In the dynamic world of digital assets, the UK is experiencing a surge in the popularity of NFTs (Non-Fungible Tokens) and digital collectibles. As these unique and often sought-after digital assets continue to captivate a new challenge arises: NFT taxation.

With limited guidance from HMRC, whether you're an artist, collector, or trader, understanding NFT taxation can be confusing. In this NFT guide we offer insights and guidance to help you navigate the tax landscape for your NFT activity.

Disclaimer

This guide is intended as a generic informative piece. This is not accounting or tax advice that can be relied upon for any UK individual’s specific circumstances. Please speak to a qualified tax advisor about your specific circumstances before acting upon any of the information in this article.

What is an NFT?

An NFT, or non-fungible token, is a distinctive form of digital asset that stands out in the cryptocurrency realm. Unlike the uniformity of popular cryptocurrencies like Bitcoin and Ethereum, each NFT is one of a kind, making it irreplaceable and unique.

The allure of NFTs lies in their application across various domains, including art, music, virtual real estate, and gaming, often taking the form of digital images or music files. Operating on blockchain technology, NFTs are traded on platforms like OpenSea and KnownOrigin, where users typically acquire them using the native tokens of the respective blockchains. NFTs offer a novel and exciting dimension to the world of digital assets.

Do you have to pay tax on NFTs in the UK?

Yes, despite only a small mention in HMRCs tax guidance, NFTs are subject to capital gains tax and income tax in the UK. Just like other cryptoassets, the tax of your NFTs depends on your activity. Generally any profits from disposing of NFTs are subject to capital gains tax and any earnings are taxed as miscellaneous income, unless it is a business activity.

To learn more about how different types of cryptocurrency are taxed, check out our detailed UK CryptoCurrency Tax Guide or to start calculating your NFT taxes get started with our crypto tax calculator.

How do NFT taxes work in the UK?

Whilst there is no specific guidance for NFTs from HMRC, it seems clear that NFT taxes in the UK follow the same rules as other cryptoassets. This means that investors in NFTs are subject to capital gains tax regulations, where they may incur tax liabilities upon selling or trading NFTs, with the amount dependent on the profit gained from the transaction.

For NFT creators and earners, the tax implications typically revolve around income tax. Creators may be subject to income tax and national insurance on the proceeds from selling or licensing their NFTs, while individuals earning NFTs as income might face taxation based on the market value of the acquired NFTs. We dive into some of the specifics below, but if you are unsure it's advisable to seek guidance from a tax professional.

NFT capital gains taxes

It is widely accepted that unless there is an NFT creation business, each time an investor disposes of an NFT they are subject to capital gains tax. This means that when you trade or sell an NFT you need to calculate your gain (or loss) on the transaction and incorporate it into your overall capital gains for the tax year. If your net capital gain exceeds the annual capital gains allowance, capital gains tax is payable at 18% or 24% (post-Budget rates from 30 October 2024), depending on whether the gain falls in your basic-rate or higher-rate income band.

How NFT gains and losses are calculated

In their guidance, HMRC recognise that “non-fungible tokens (NFTs) are separately identifiable and so are not pooled”. Therefore the normal share matching and pooling rules used to calculate the capital gains on (fungible) cryptoassets like BTC and ETH are not relevant.

To calculate the capital gain or loss on the disposal of an NFT, simply deduct the actual acquisition cost of the NFT from the disposal proceeds.

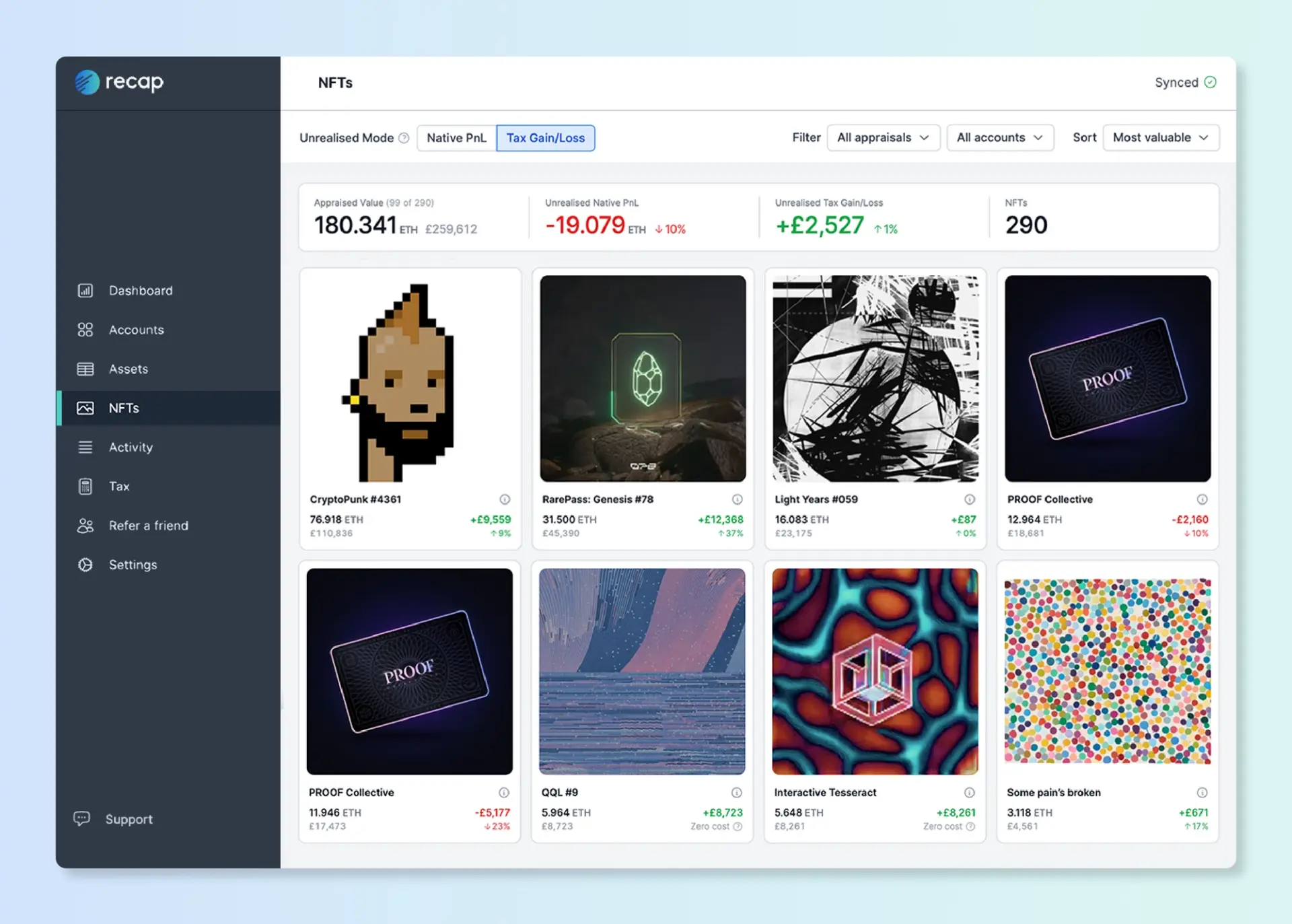

It’s important to keep accurate records of your NFT activity including dates, amounts and valuations in case they are requested by HMRC or are needed for your tax return. Maintaining precise records for your NFT transactions isn't just a formality; it also streamlines the process of calculating your capital gains and losses. Crypto tax calculators like Recap which automatically track your NFTs are an invaluable tool for record-keeping, providing you with time savings and peace of mind for accuracy.

NFT income taxes

Income tax may apply to NFTs that are earnt or if your NFT activity is a business activity or is classified “finanical trading” by HMRC.

Income tax from earning NFTs

Earning money with NFTs can be a real adventure with activities like staking, airdrops, and Play-to-Earn (P2E) gaming. Despite the absence of specific HMRC guidance on NFT income, it is anticipated that taxation for such earnings will align with established principles for other cryptoassets. Consequently, income derived from NFT activities, may be subject to miscellaneous income tax based on the sterling value at the date the tokens are receivable.

Income tax for financial trading in NFTs

In some circumstances UK taxpayers may be treated as a ‘financial trader’ for their NFT activity. In which case profit from their disposals are treated as business trading income, subject to income tax and national insurance instead of capital gains. You can work through HMRC‘s Badges of Trade to understand your position, but this can be hard to determine and is mostly decided on a case-by-case basis. Because NFTs are a new and evolving asset class we recommend speaking to a tax professional to fully understand the appropriate tax treatment for your circumstances.

NFT creators

NFT creators are most likely to be taxed as a trading business for creating and selling their own collection. The self-employed business profits will be subject to income tax and national insurance.

Other investment activity that is not connected to their own NFT collections will be subject to capital gains tax as outlined above unless the activity is more akin to a business and then income tax applies. Similarly, cryptoassets received by the creator as business income are subject to capital gains tax when disposed of.

Is minting an NFT taxable?

When an individual creates an NFT, the process, known as minting, involves generating a unique non-fungible token on a blockchain, assigning specific identifiers and metadata to distinguish their digital creation. Importantly, it is likely that minting itself is not subject to taxation, as there is no immediate disposal or realised gain. Costs incurred in the minting process are likely to be eligible as an allowable expense to be deducted from any income or capital gains when the NFT is sold, lowering the overall tax liability.

Does VAT apply to NFTs?

Possibly yes, but it is not clear and there is no HMRC guidance. UK creators need to consider VAT when selling their NFTs and should take advice from a crypto VAT specialist. If VAT is payable, the location of the customer may be relevant, but not always. Proving to HMRC that customers are overseas can be challenging, if not impossible. Even if UK VAT does not apply on sales to overseas customers, you may be liable for VAT (or equivalent) in the customers’ country.

Some crypto VAT specialists think that there may be no VAT on NFT sales by the creator, even when made to UK customers. However it is strongly recommended by VAT professionals that clearance is obtained from HMRC for your specific circumstances if you are not declaring VAT on the sale of your own NFT collection.

How to reduce your NFT taxes

While tax evasion is illegal, there are a few ways you can legally navigate taxes to reduce your tax liability on your NFTs.

- Take advantage of your allowances. UK taxpayers are entitled to an annual capital gains tax allowance, £3,000 for the 2025/26 tax year, and an annual trading allowance, which entitles each individual to £1,000 tax free miscellaneous or trading income (you are probably not eligible for the trading allowance if you have other self employment).

- Tax loss harvesting. If you are holding any NFTs at a loss then you could consider selling them to realise a capital loss and offset your capital gains in the same tax year, or if not used, to carry forward to set against future gains.

- Negligible value claims. If NFTs you still own are now worthless, you can make a capital loss negligible value claim in the tax year in which they became worthless. HMRC require a claim to be made and certain information about the loss to be provided.

- Gift NFTs to your spouse. In the UK, gifting to a spouse is viewed as a no-gain no-loss disposal so is tax free, meaning you can transfer NFTs to your spouse before they are sold, to take advantage of both individuals' capital gains allowances.

- Hire a tax professional. Sounds expensive, but the potential tax savings a good accountant can uncover often surpasses their fees significantly.

- Track your NFTs with Recap. Our purpose built NFT gallery with current price appraisals makes tracking your NFT gains and losses simple, identifying opportunities for disposals that will reduce your tax liability.

For more approaches to tax optimisation for your cryptoassets take a look at our article "Can you avoid paying tax on crypto in the UK" or keep reading for more specific detail on offsetting your NFT losses.

NFT tax loss harvesting

If you are holding any NFTs at a loss in your portfolio then you could consider disposing of them to realise a loss which can offset any gains in the same tax year, therefore lowering your tax position.

UK tax year

It’s important to remember that the UK tax year runs from 6th April to the 5th April the following year, and that you can only realise a loss to offset gains in the same tax year. Capital losses can be rolled forward to future tax years but cannot be used to offset gains from previous tax years.

How to offset capital gains with NFT losses

- Discover which of your NFTs are underperforming - you can use Recap’s NFT gallery and tax dashboard to find out the realistic value of your NFTs and their unrealised capital gain or loss.

- Carefully consider your current tax position for the current tax year and whether realising a loss will benefit your circumstances. If so, decide which underperforming NFTs you are prepared to dispose of in order to realise the loss.

- Dispose of the chosen NFT(s) to realise the capital loss, for example by selling, trading or burning your NFT.

Burning an NFT to realise a tax loss

Burning an NFT refers to the intentional and irreversible action of destroying a non-fungible token by sending it to a burn address. Burn addresses have unobtainable keys and therefore any assets sent to the address are permanently unrecoverable. Typically burn addresses have been used to eliminate unwanted or worthless tokens and also to reduce supply of a token to increase scarcity. From a tax perspective, burning an NFT can be used to realise a tax loss, where the taxpayer disposes of the asset with £Nil proceeds and the purchase cost is the capital loss.

Burning an NFT warning

The concept of burning an NFT is extreme and complex.Tax implications may vary by tax jurisdiction and individual circumstance, therefore you should consult an advisor.

How to report NFT transactions to HMRC

Taxable NFT transactions should be reported and paid as part of HMRC’s Self Assessment Tax Return (form SA100). They need to be included as capital gains or miscellaneous income depending on the appropriate tax treatment. It is also essential to report all capital losses so that they can be ‘claimed’ against gains in future tax years. Losses can be reported to HMRC on the tax return or by letter (if a tax return is not required). Creators and any individuals who need to report their NFT activity as a business activity or Financial Trading should do so on the Self Employment pages of the tax return.

One of the most important messages to come from HMRC guidance is the necessity of keeping records of all cryptoasset activity. Good records are the easiest way to prove your acquisition costs and history to HMRC.

HMRC guidance states records should detail:

- the type of cryptoasset

- date of the transaction

- if the asset was bought or sold

- number of units involved

- value of the transaction in pound sterling (as at the date of the transaction)

- cumulative total of the investment units held

- bank statements and wallet addresses, in case these are needed for an enquiry or review.

Accurate reporting for NFTs and other cryptoassets is essential, especially given HMRC’s increasing attention to cryptocurrency transactions.

Using Recap’s Software for NFT Tax Tracking

Calculating taxes for your NFT transactions is a breeze with crypto tax software like Recap. Simply connect your wallets and Recap identifies all your taxable transactions and calculates capital gains (or losses) and income tax obligations, based on HMRC guidance.

You can use Recap to calculate and keep track of your NFT income and capital gains by following these steps:

- Sign up for free.

Head to recap.io and sign up using your email address or google account. Make sure to backup your recovery key and select your country and tax jurisdiction settings. - Connect your NFT wallets and any other cryptoasset data sources.

Automatically sync your transaction data by connecting your wallets and exchanges. Upload additional data via CSV (for example extinct exchanges, old accounts). - Check your data is correct.

Ensure all of your historical data is uploaded and that all transactions are accurately classified and accounted for. - Recap automatically calculates your crypto capital gains, capital losses and income tax.

We source valuations for all of your NFTs and cryptoassets and apply the appropriate tax treatment to each transaction to calculate your total capital gains and income. - Generate and download your crypto tax reports.

Subscribe to Recap and head to the tax page to download your crypto tax reports.

Crypto tax calculators are really effective for crypto investors navigating lots of transactions and complex activity. They are the fastest and most reliable way to calculate your crypto taxes. Recap’s NFT gallery and UK tax dashboard also provide detailed insight on the true value of your NFTs, identifying opportunities to optimise your portfolio and tax liability.

Get started for free.