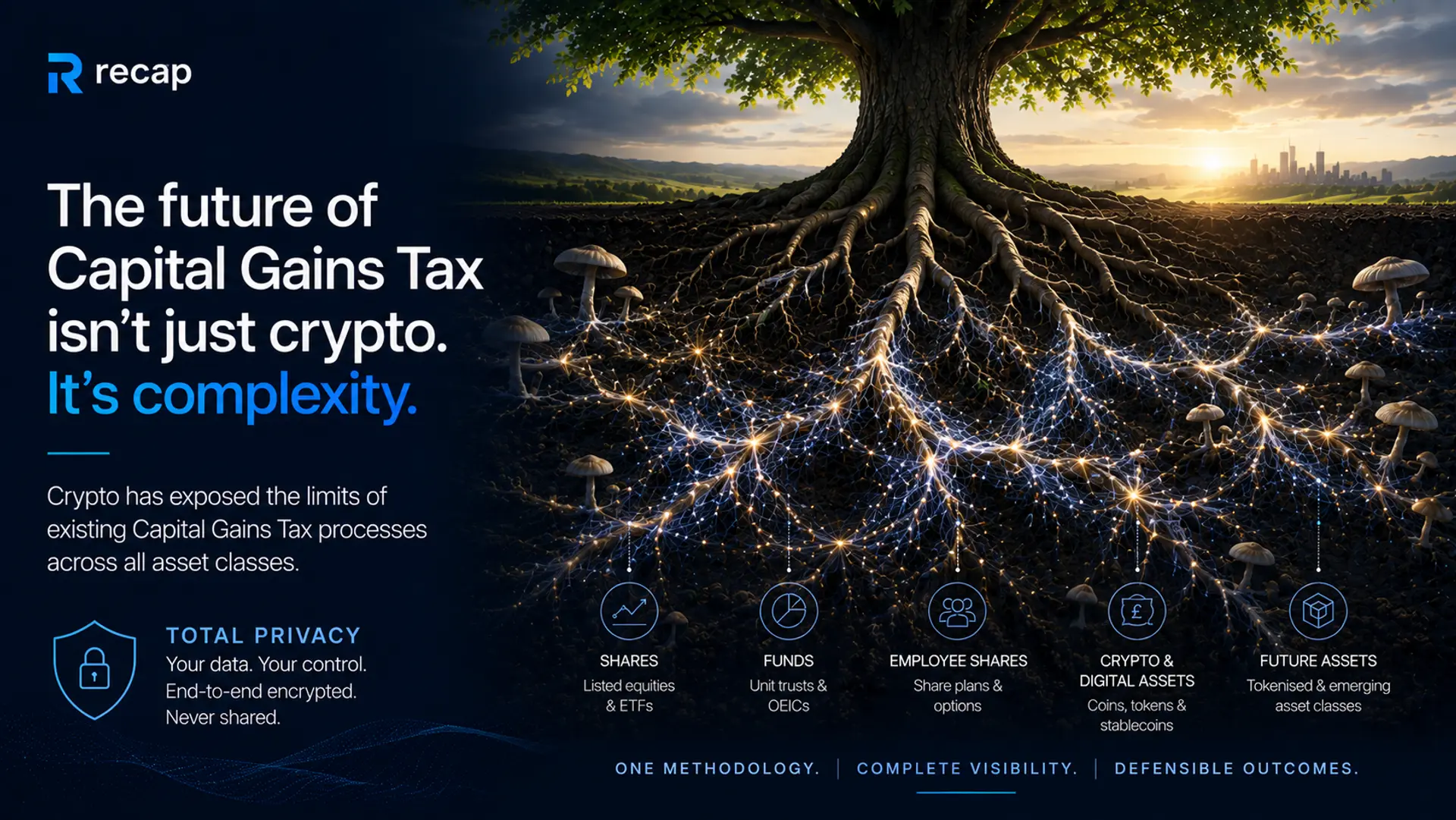

Crypto has exposed the limits of existing CGT processes across all asset classes.

For some years, digital assets have been treated as a specialist corner of Capital Gains Tax. As more and more firms encounter this new asset class, it is exposing a problem that was already there across the wider investment landscape: Complexity.

As portfolios trend towards more diversification and such diversification becomes more accessible, investors increasingly spread assets across multiple platforms, brokerages and custodians. A single client may well now hold listed securities with multiple investment platforms, have legacy holdings, employee share schemes, ISAs, overseas investments, have exposure to property directly or via REITs as well as holding and trading digital assets—all spanning multiple tax years.

Theoretically, none of these is especially difficult to address given enough time. Collectively, they become surprisingly complex.

The UK's changing CGT landscape

Recent reductions in the UK's Capital Gains Tax annual exemptions bring more and more individuals into the scope of CGT. The extra number of individuals to support can further stress an already stretched firm. Compounding this, advisers are seeing increasing transaction volumes across portfolios, more fragmented records and greater expectations around governance and evidence.

Such complexity and volumetric datasets are no longer reserved for ultra-high-net-worth clients. This has become mainstream.

The arduous process all firms recognise

When we speak with accountancy firms across the UK, a common theme emerges. Complex capital gains work often passes through two or three levels of review before reaching partner sign-off. Not because firms lack technical expertise. Because they recognise the underlying process can be time-consuming, difficult to evidence and heavily reliant on manual reconciliation and prone to error. Spreadsheets remain commonplace. Supporting documentation is often fragmented. Reviewers spend valuable time checking calculations rather than delivering advice.

Whilst many firms tell us they have confidence in their people. Fewer have complete confidence in the process.

The standard has shifted

HMRC's Guidelines for Compliance 13 reinforces an increasingly important principle: tax submissions should be correct, complete and supported by appropriate evidence. This represents a broader shift in professional expectations. The standard has shifted from plausible to defensible.

The question is no longer simply whether a calculation appears reasonable. It is whether the methodology can be explained, evidenced and defended if challenged.

Beyond crypto

This is precisely why Recap's evolution into being able to address listed securities really matters.

Capital gains calculations become exponentially more difficult as portfolios span multiple asset classes, multiple platforms and multiple ownership histories.

Whether reconstructing digital assets or calculating gains on listed securities, the underlying professional requirement is the same:

1, accurate data,

2, consistent methodology,

3, transparent calculations,

4, evidence that stands up to scrutiny and can be forensically defended and reconstructed.

One methodology. Multiple asset classes.

The next step is even more significant.

Professional advisers increasingly need to consider capital gains across traditional investments and digital assets together.

Applying share pooling principles consistently across both asset classes creates a single, coherent approach to CGT reporting, reducing manual effort while improving confidence in the final result. For firms, this is about much more than automation. It is about delivering work that partners can confidently sign.

Looking ahead

As digital assets become another recognised investment class rather than a specialist niche, the distinction between "crypto tax software" and "capital gains software" begins to disappear.

The future belongs to platforms that help firms manage complexity across every asset class, giving advisers confidence that their work is not simply plausible—but defensible.