Understanding your crypto tax liability can be a daunting task. But did you know that transferring cryptocurrency to your spouse or civil partner could help you save on capital gains tax?

In recent times gifting crypto to your spouse has become a savvy tax-saving move for UK investors, with the no gain/ no loss disposal letting you transfer cryptoassets tax-free, tapping into your partner’s annual capital gains allowance.

With growing regulation it's important to understand the broader spectrum of crypto tax, especially before considering tax optimisation. For help navigating the intricacies of taxation in the UK, take a look at our UK tax guide. In this article, let’s break down the rules around spouse gifts…

Disclaimer

This guide is intended as a generic informative piece. This is not accounting or tax advice that can be relied upon for any UK individual’s specific circumstances. Please speak to a qualified tax advisor about your specific circumstances before acting upon any of the information in this article.

Understanding capital gains tax on crypto

When you sell or dispose of crypto in the UK, you may need to pay CGT on the profit (or gain) you’ve made. But, what happens to capital gains tax when you transfer crypto to your spouse? The good news is, HMRC treats the transfer of cryptoassets between spouses or civil partners differently to taxable crypto disposals. Instead of being taxed on the gain at the point of disposal, the transfer or gift is considered a “no gain/ no loss” disposal.

What is a “no gain/ no loss” disposal?

HMRC describes no gain/ no loss disposals as “disposals where the asset is treated as passing from the transferor to the transferee at a value which results in neither a gain nor a loss accruing to the transferor”.

In simple terms, the transfer is treated as taking place for an amount that gives the transferring spouse neither a gain nor a loss. The receiving spouse or civil partner takes over that deemed acquisition cost, rather than using the market value at the date of the gift. Any amount actually paid is ignored.

How is a crypto spouse transfer or gift taxed?

When a crypto asset is transferred (or gifted) between two spouses or civil partners, there is a disposal by the gifter and an acquisition by the receiver for capital gains tax purposes. The disposal is deemed to take place at ‘no-gain and no-loss’ meaning there is no tax due for the gifter. Their spouse or civil partner, the receiver, is not taxed on the receipt of the asset but will be subject to capital gains tax when they later dispose of it.

- The gifter: The disposal proceeds used in the capital gains calculation is a balancing figure and it is equal to the assets costs of acquisition, plus enhancement expenditure, plus incidental costs of sale.

- The receiver: the gifter’s disposal proceeds figure is the deemed cost of acquisition for the transferee spouse.

What happens when your spouse disposes of the crypto?

After the transfer, your spouse will now own the crypto, and when they decide to sell or dispose of it, they will be responsible for any CGT that applies. The cost basis (acquisition cost) for them will be the same as it was for you: your original acquisition cost, plus any allowable costs. This means that any gain or loss they report will be based on this original value, not the value at the time of the transfer.

What are the requirements for ‘no gain/ no loss’ spouse disposals?

The disposal is deemed to take place at ‘no-gain and no-loss’ provided the couple is:

- married or in civil partnership, and

- living together during the tax year

The rules are quite flexible. You don’t need to be physically living in the same house to qualify. Even if you live separately or have separate homes, as long as your marriage or civil partnership hasn’t broken down, the no gain, no loss rule still applies.

How do spouse gifts work with separation and divorce?

If you separate or divorce, the no gain/ no loss treatment does not last forever. Individuals who are married or in civil partnership are treated as living together unless they separate:

- under an order of a court

- by a deed of separation, or

- in circumstances where the separation is likely to be permanent

The rules became much more generous from 6 April 2023. Separating spouses and civil partners can now make no gain/ no loss transfers up to the earlier of the end of the third tax year after the tax year in which they stop living together, or the date the court grants their divorce, annulment or dissolution. Transfers made under a formal divorce or separation agreement, or a court order, can qualify without that three year limit.

Once the window closes, any transfers take place at market value because the couple are treated as ‘connected persons’, even if they are still legally married and regardless of any amount actually paid. For example: if a couple permanently separates during the 2026/27 tax year, transfers between them up to 5 April 2030 take place at no gain/ no loss, unless the court grants a divorce or dissolution order first. Transfers made under a formal divorce agreement or court order can still qualify after that, with no time limit.

Exceptions to the spouse gift rule

The rule of no gain or loss doesn't always apply:

- If the transfer happens on death, including a ‘deathbed gift’ made in contemplation of death. The receiving spouse is treated as a legatee and acquires the asset at its market value at the date of death, with no chargeable gain or loss arising

- If the transferred asset formed part of the gifting spouse's trading stock

- If the transferred asset becomes part of the receiving spouse's trading stock.

If an individual is engaging in financial trading in cryptoassets and transfers assets into or from the trading stock of this business then the transfers are deemed to take place at market value. This is a complex area and we strongly advise seeking assistance from a qualified tax professional if this applies to your situation.

How to reduce your crypto taxes with spouse gifts

So, you can transfer or gift crypto to a spouse or civil partner as a no gain/ no loss disposal but where are the actual tax savings?! The potential tax saving relies on the receiving spouse either not using their entire capital gains allowance, being taxed at a lower rate, or both.

Access your spouse's unused annual exempt amounts

The UK tax year runs from 6th April to 5th April the following year and all UK taxpayers have an annual capital gains allowance, which determines the amount of capital gains you can earn before becoming liable for tax. By strategically transferring crypto to your spouse or civil partner and carefully timing disposals, each partner can utilise their capital gains allowance to minimise taxable gains.

The annual exempt amount 2026/27

The annual exempt amount for the 2026/27 tax year is £3,000, so you can realise £6,000 in capital gains between you before paying capital gains tax.

Leveraging a spouse’s lower tax rate

Capital gains tax is not a one-size-fits-all scenario; the rate of tax varies based on individual income levels. When one partner finds themselves in a lower tax bracket than the other, strategically transferring assets to the partner in the lower bracket before making disposals can result in substantial savings on the taxable gain. For the 2026/27 tax year, basic rate taxpayers pay 18% capital gains tax on crypto gains, while higher and additional rate taxpayers pay 24%.

Spouse gifting is a great tax optimisation strategy and can be used alongside other techniques for a massive impact on your tax bill. Take a look at other tax saving opportunities for crypto in our article "Can you avoid paying tax on crypto".

Get professional tax advice

Every investor's situation is unique, and it's crucial to tailor these strategies to individual circumstances so we strongly encourage you to consult with tax professionals to assess your unique circumstances and help you with tax planning.

How to report spouse transfers to HMRC

Do you need to tell HMRC about a spouse transfer? Not always. Even where no tax is due, you should keep records of the transfer and include the details if they are needed to support your capital gains tax computation, or if HMRC asks for them. If you are completing the SA108 capital gains pages, your adviser may recommend disclosing spouse transfers for clarity. A no gain/ no loss spouse gift with no tax due is not automatically the same as a taxable gain.

It’s also a good idea to declare the transfer on both spouse’s tax returns even if it’s not strictly required to help prevent any misunderstandings with HMRC.

Disposal proceeds

If you already file a Self Assessment tax return, don’t forget that you must report your disposals if your total disposal proceeds for the tax year exceed £50,000, even if your capital gains are below the annual exempt amount.

It’s important to keep thorough records of spouse transfers, including dates, values, and any relevant documentation. Crypto tax calculators can help to keep you on track with tax reporting liabilities - they automate much of the process, saving you time and ensuring accuracy with a consistent approach to crypto valuations.

How to account for spouse gifts in Recap

Transferring crypto to your spouse can be a smart tax-saving strategy, but keeping track of all the details can be challenging. By using a crypto tax calculator like Recap you can keep track of your whole portfolio and tax liability - simply connect your accounts or upload transaction data and the software applies the corresponding tax treatment to all of your transactions.

To account for spouse gifts in Recap both partners will need their own independent Recap account in order to correctly represent their portfolio and beneficial ownership of funds.

The gifting spouse

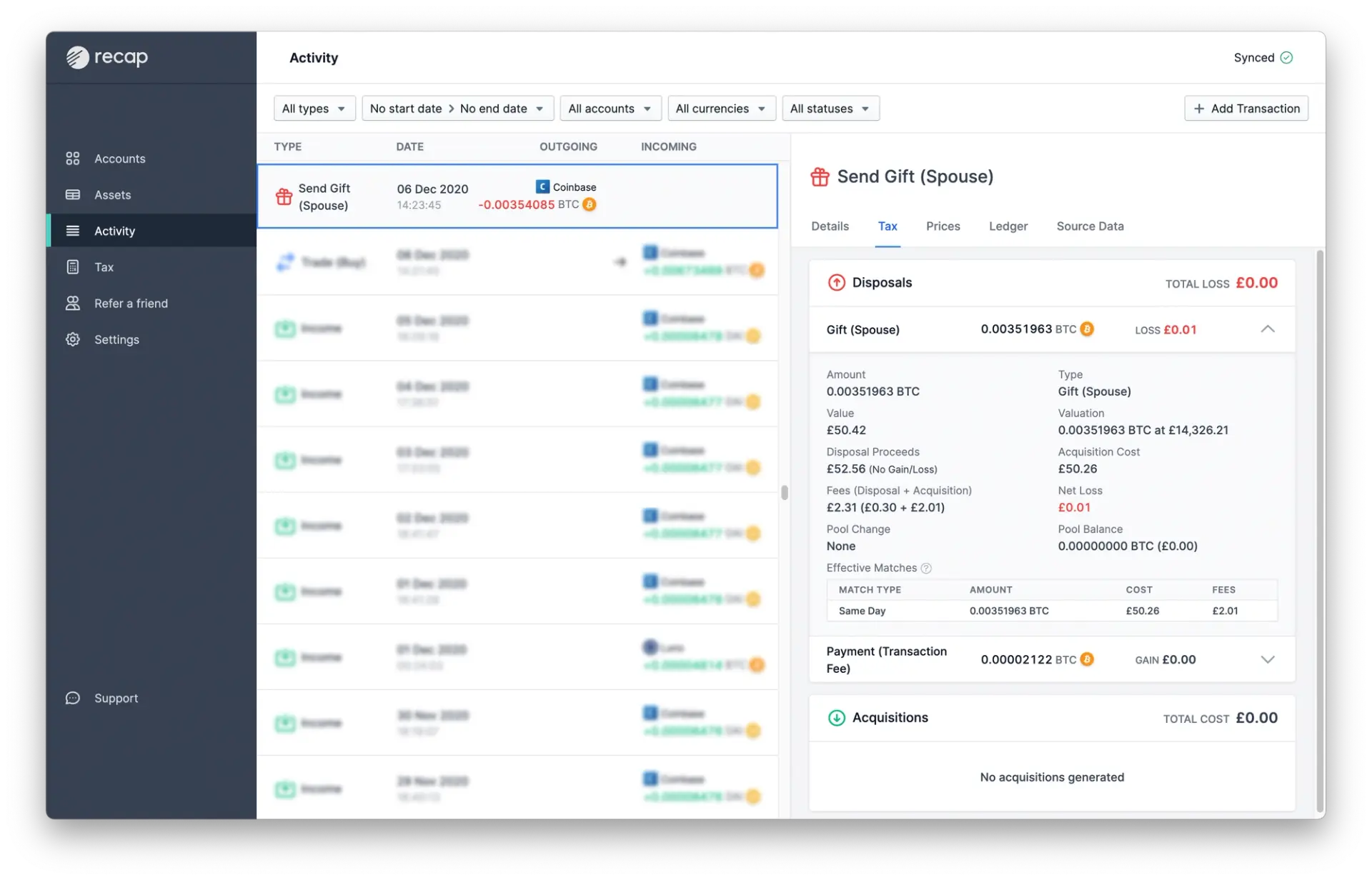

Sending a gift or transferring crypto is likely to be tracked as a withdrawal by your exchange or wallet. To correctly account for the transaction in Recap, reclassify the withdrawal to Send Gift (Spouse). Recap treats spouse gifts as a disposal at no gain/ no loss, and the gift appears in the Gift Disposals section of your capital gains tax report along with its associated cost.

The receiving spouse

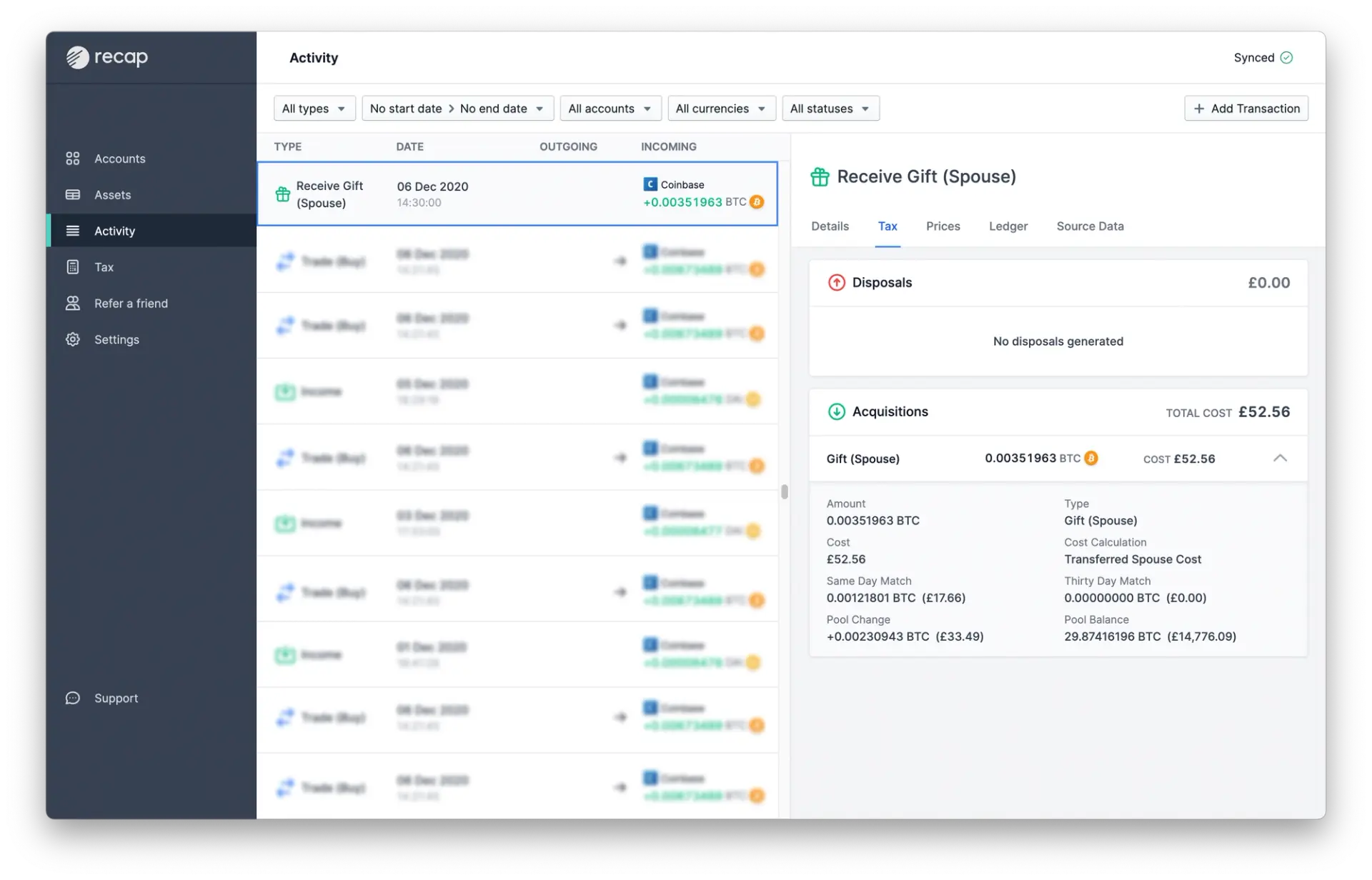

Receiving a crypto gift or transfer of crypto is likely to be tracked as a deposit by your exchange or wallet. In your own Recap account, reclassify the deposit to Receive Gift (Spouse). Recap will then ask for the Gift Value, which becomes your acquisition cost: enter the figure shown in the Gift Disposals section of your spouse’s Recap report. This value will be used to calculate your capital gain when you eventually dispose of the asset. For step by step instructions, see our help guide How to account for spouse transfers in Recap.

Spouse gifts: key takeaways

- In the UK, gifting crypto to your spouse or civil partner is not taxable

- Spouse transfers can help you to significantly lower your tax bill by utilising both partner’s annual capital gains allowance

- There is opportunity to reduce the tax bill further if a spouse is in a lower tax bracket