Filing your tax return might feel daunting, but don’t worry! Follow these steps to report your crypto transactions for the 2024 tax year to the IRS.

Disclaimer

This guide is intended as a generic informative piece. This is not accounting or tax advice that can be relied upon for any individual’s specific circumstances. Please speak to a qualified tax advisor about your specific circumstances before acting upon any of the information in this article.

Understanding Your Crypto Tax Obligations

The IRS treats cryptocurrency as property, meaning that crypto transactions are subject to capital gains and income taxes. It's crucial to report all taxable events to remain compliant and avoid potential penalties.

Taxable Events Include:

- Selling cryptocurrency for USD or other fiat currencies: Anytime you convert crypto to traditional currency, it's considered a taxable event.

- Trading one cryptocurrency for another: Exchanging Bitcoin for Ethereum, for example, is taxable.

- Using cryptocurrency to purchase goods or services: Spending crypto is treated as a sale of property, triggering a taxable event.

- Earning cryptocurrency through mining, staking, or airdrops: Such earnings are considered income and must be reported.

Non-Taxable Events Include:

- Purchasing cryptocurrency with USD: Simply buying and holding crypto isn't taxable.

- Transferring cryptocurrency between wallets you own: Moving crypto between your wallets isn't a taxable event.

Find out how tax applies to crypto in more detail in our US Crypto Tax Guide.

Step-by-Step Guide to Filing Your Crypto Taxes

Step 1: Gather Your Crypto Transaction Records

Accurate record-keeping is the foundation of proper tax reporting. Ensure you have detailed information on each transaction, including:

- Dates of acquisition and disposal

- Amounts and types of cryptocurrency involved

- Fair market value in USD at the time of each transaction

- Purpose of the transaction (e.g., investment, payment for services)

Step 2: Calculate Your Capital Gains and Losses

For each taxable event, determine your capital gain or loss:

- Short-Term vs. Long-Term: Assets held for less than a year are subject to short-term capital gains tax, typically at higher rates than long-term gains for assets held over a year.

- Calculation: Subtract the cost basis (purchase price plus any associated fees) from the proceeds of the sale or fair market value at the time of the transaction.

Step 3: Calculate Your Crypto Income

If you've received cryptocurrency as payment for goods or services, through mining, staking, or airdrops, this constitutes ordinary income. You’ll need to report the Fair Market Value of the asset in USD at the time of receipt.

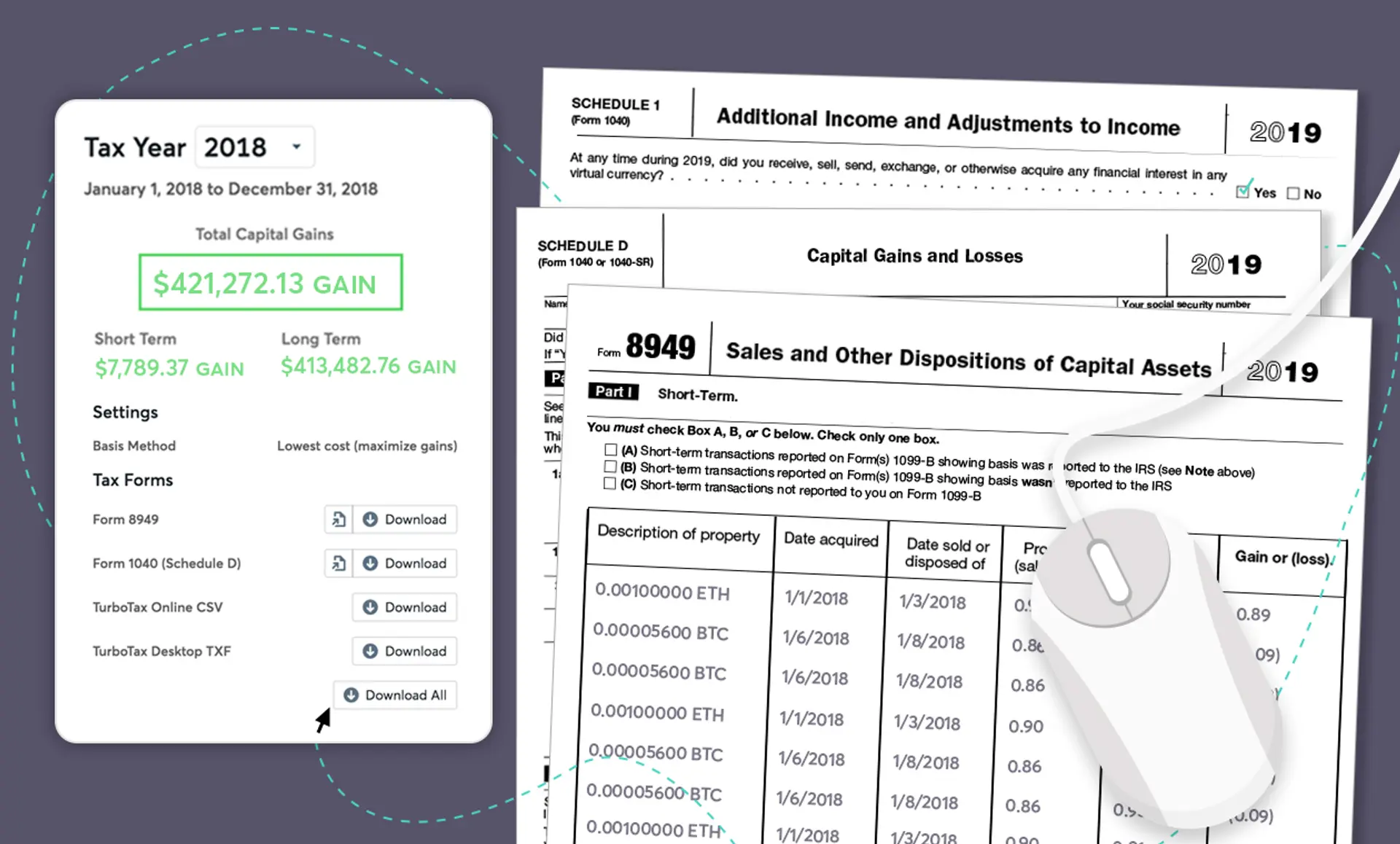

Recap can streamline this process by importing and organizing your transaction data. Tax calculations are automated and Recap provides IRS-compliant tax reports for all your capital gains and income from crypto.

Step 4: Complete IRS Forms

- Form 8949: List all capital asset transactions, including cryptocurrency trades.

- Schedule D: Summarize total capital gains and losses from Form 8949.

- Schedule 1 or Schedule C: Report any additional income from crypto activities.

In our blog “Which crypto tax form?” you’ll find more detailed information on the tax forms you’ll encounter as a crypto investor and where to declare your crypto activity.

Step 5: File and Pay Your Tax Return to the IRS

Once you have completed all necessary information, you can file through the IRS e-file system or by mail. The US filing deadline is April 15, 2025, unless you've obtained an extension. If you owe taxes, timely payment will help you avoid penalties and interest.

Common crypto tax filing mistakes to avoid

- Not reporting all crypto activity: Many investors are uncertain about which cryptocurrency activities are taxable, leading to potential misreporting. Overlooked taxable events include trading one cryptocurrency for another, using crypto to purchase goods or services, and earning crypto. Failure to report these can result in penalties. For comprehensive information, consult our [Crypto Tax Guide] or seek personalized advice from a tax professional.

- Incorrect Cost Basis Calculation: Determining the correct cost basis - the original value of an asset for tax purposes - is crucial. Misunderstanding different cost basis methods, such as First-In-First-Out (FIFO) or Last-In-First-Out (LIFO), can lead to inaccurate tax reporting. With new approaches introduced for the 2025 tax year, confusion is understandable. Recap defaults to the correct cost basis method and allows you to switch methods when applicable, ensuring accuracy.

- Poor Record-Keeping: Incomplete or disorganized records of cryptocurrency transactions can trigger IRS audits and complicate tax filings. It's essential to maintain detailed records of all transactions, including dates, amounts, transaction types, and the value in USD at the time of each transaction.

- Missing Tax Deadlines: Failing to file your tax returns on time can lead to late filing penalties and interest charges. The IRS imposes penalties for late filings, which can accumulate over time. If you're unable to meet a deadline, filing for an extension can provide additional time to prepare your return without incurring late filing penalties.

- Ignoring Transactions on Foreign Exchanges: Some investors mistakenly believe that transactions on foreign exchanges are exempt from U.S. tax reporting. However, the IRS requires you to report all cryptocurrency transactions, regardless of where they occur. Neglecting to include foreign transactions can result in underreporting income and potential penalties. Ensure you track and report all global crypto activities accurately.

- Not Staying Updated with Tax Laws: Tax regulations are continually evolving. Failing to stay informed about the latest tax laws can lead to compliance issues. Regularly consult reliable sources or work with a tax professional to ensure you're up-to-date with current regulations.

How Recap Can Help US Taxpayers

Filing your crypto taxes doesn't need to be overwhelming. By following the steps above, you can ensure your tax return is accurate and submitted on time or within the extension deadline.

Recap can simplify your crypto tax reporting by aggregating your crypto transactions and automatically calculating capital gains, losses, and income, generating IRS-compliant tax reports you can easily include with your return.