Welcome to our comprehensive guide for individuals on cryptocurrency tax in the US, providing you with all the essential information based on IRS crypto tax guidance. From understanding when tax applies to filing your tax return, we’ve got you covered.

As a responsible US crypto investor it’s crucial to report any taxable gains or income from your crypto assets to the IRS. Our guide explores the intricacies of crypto tax, breaking down how different transactions are taxed and the differences between capital gains and income tax.

Crypto tax is complex!

Given the complex nature of crypto tax this is an in depth guide with a lot of information! Navigate through topics quickly by using the menu on the left hand side.

Disclaimer

This guide is intended as a generic informative piece. This is not accounting or tax advice that can be relied upon for any UK individual’s specific circumstances. Please speak to a qualified tax advisor about your specific circumstances before acting upon any of the information in this article.

Virtual currency and cryptocurrency

What is virtual currency?

Virtual currency is a digital representation of value, other than a representation of the U.S. dollar or a foreign currency (“real currency”), that functions as a unit of account, a store of value, and a medium of exchange. Some virtual currencies are convertible, as the IRS describes in Question 1 of the FAQs, this means that they have an equivalent value in real currency or act as a substitute for real currency. The IRS uses the term “virtual currency” to describe cryptocurrency and other types of currency used as a medium of exchange, such as digital currency.

What is cryptocurrency?

The IRS confirm in their FAQs that cryptocurrency is a type of virtual currency that uses cryptography to secure transactions that are digitally recorded on a distributed ledger, such as a blockchain. They also describe on-chain and off-chain transactions. A transaction involving cryptocurrency that is recorded on a distributed ledger is referred to as an “on-chain” transaction; a transaction that is not recorded on the distributed ledger is referred to as an “off-chain” transaction.

Do you have to pay taxes on cryptocurrency in the US?

Yes, you have to pay tax on cryptocurrency in the US. The IRS is clear that cryptocurrency gains and income earned by US taxpayers are subject to either income tax or capital gains tax, determined by the specific nature of your transactions.

When you dispose of a cryptocurrency (by selling, trading, or paying for a service or item) you are subject to capital gains or losses. Cryptocurrency that you receive but have not “bought” for example airdrops and mining activity, should generally be reported as ordinary income.

Compliance with tax regulations is mandatory, and declaring your crypto taxes is a legal responsibility. However, there are legal strategies to potentially reduce your crypto tax liability. For insights on optimizing your crypto tax situation and minimizing tax payments, refer to our article "Can you avoid paying tax on crypto in the US?"

How much is cryptocurrency taxed?

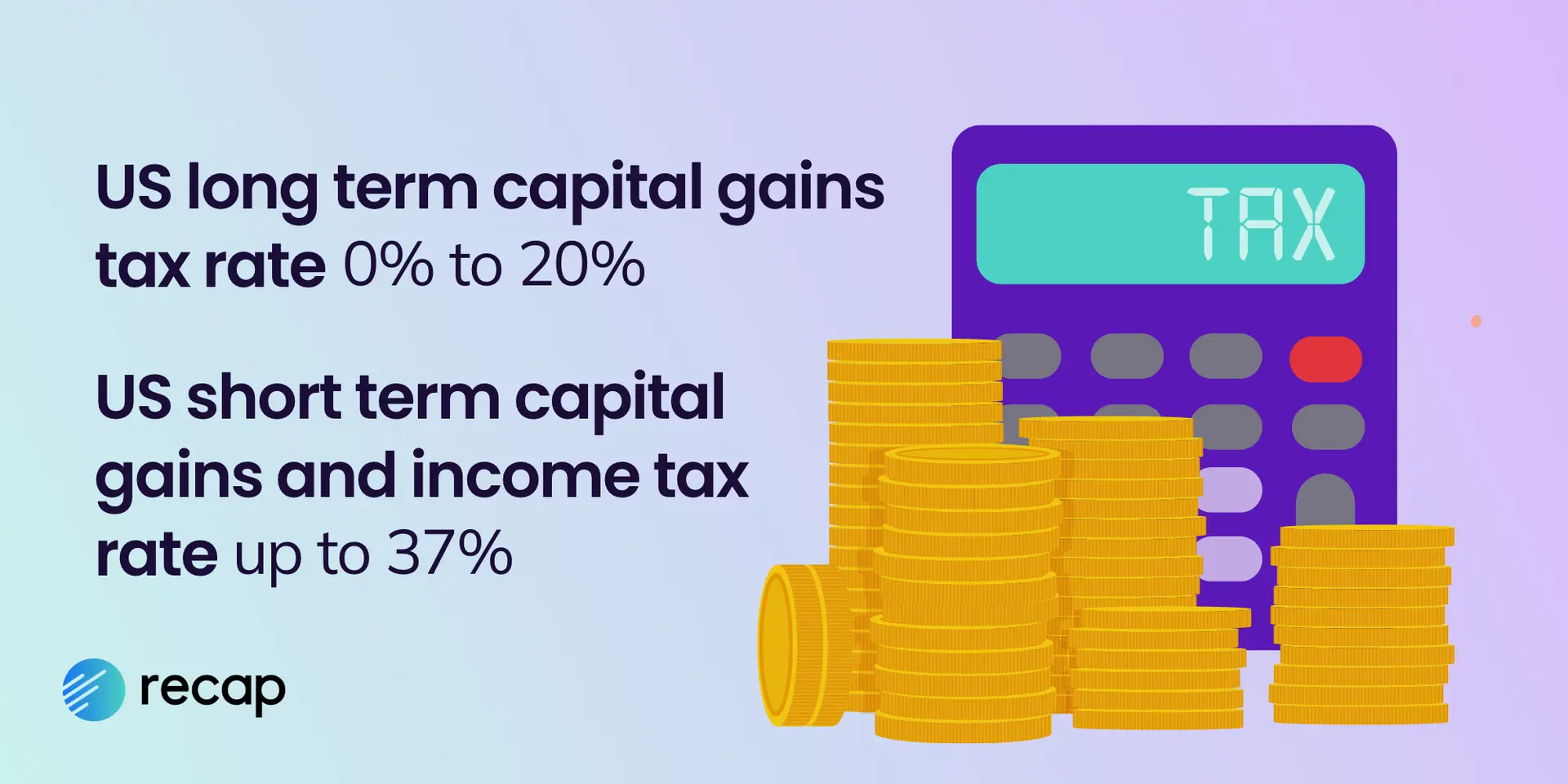

In the US, short-term capital gains and income from crypto may attract taxes of up to 37%, whereas long-term capital gains are taxed between 0% to 20%. The exact amount of tax you owe on your crypto depends on several factors including your earnings and income tax bracket, the transaction, and holding period of the asset. We’ll look into all of these in detail in this tax guide.

How is crypto taxed in the US?

In the US, most cryptocurrency taxes fall into two categories: capital gains and ordinary income.

Crypto capital gains tax

The IRS treats cryptocurrency as property for federal tax purposes. Therefore general tax principles that are applicable to property transactions must be applied to crypto transactions. When you dispose of a crypto asset (by selling, trading, or spending it) you are subject to capital gains or losses.

Some of these dispositions include:

- Selling cryptocurrency for a fiat currency (USD, GBP, EUR, etc.)

- Purchasing goods or services with cryptocurrency

- Exchanging one cryptocurrency for another (BTC to ETH, ETH to DOGE, DOGE to SHIB, USDT to USDC etc).

A good rule of thumb is that if cryptocurrency is leaving your possession and you are receiving something of value for it, it likely is a capital event and you will experience a capital gain or loss.

Crypto income tax

In general, any cryptocurrency that you receive but have not “bought” can be classified as ordinary income and should be reported under either the “other income” section Schedule 1, line 8z.

Schedule C should be used to report crypto income for a trade or business - for example if you are a mining business sole proprietor. If you are a trade or business, earnings are subject to self-employment taxes as well.

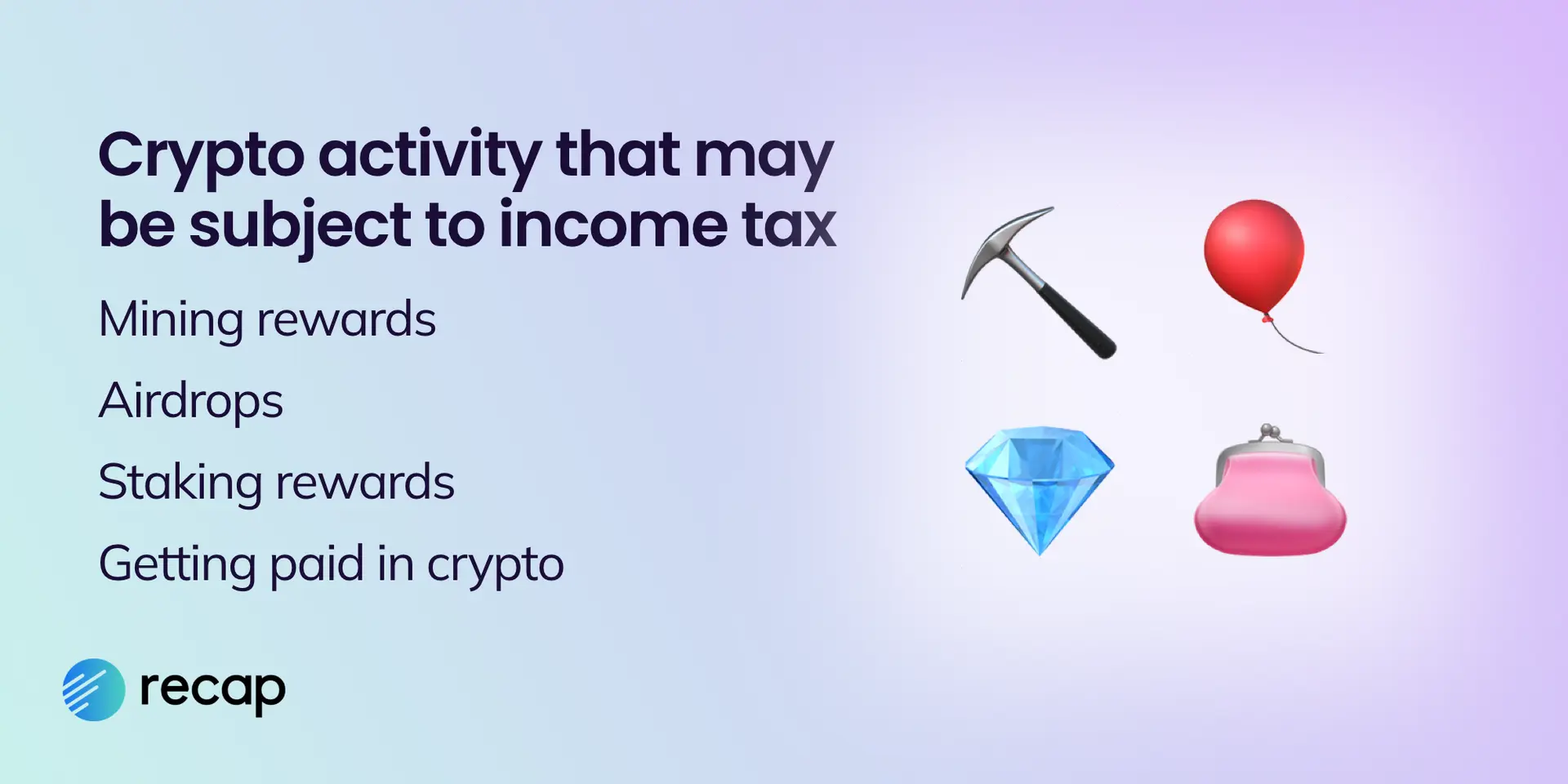

These transactions generate ordinary income:

- Airdrops

- Getting paid in cryptocurrencies for goods and services you provide

- Staking Rewards

- Mining Rewards

DeFi rewards

Note: Certain DeFi (or decentralized finance) rewards are considered ordinary income. There is not much guidance and there are different positions but a good rule of thumb is that any “free” coins that are not received by trading / buying (hard fork, airdrop), are always income in the IRS eyes. Please consult your accountant or tax attorney for questions regarding your DeFi activity and its tax implications.

For individuals, think of ordinary income as your paycheck from your employer, any payments made to you for freelance work, receiving a gift containing fiat currency, etc.

For businesses, cryptocurrency could also be business income, which could allow you to deduct business expenses. Please consult your accountant or tax attorney for which items could be deducted from your tax liability.

Tax free crypto transactions

Not every transaction is taxable or reportable under the tax code.

Non-taxable transactions include:

- Purchasing cryptocurrency with fiat currency (USD, GBP, EUR, etc.)

- Transferring cryptocurrencies between wallets and exchanges you own

- Sending or receiving cryptocurrency as a gift (although there may be tax consequences for the donor)

- Making donations to qualified charities in cryptocurrency

Crypto capital gains tax

Crypto capital gains tax is triggered when you dispose of a crypto asset. Essentially, if you sell your crypto for more than its cost basis (the original purchase price), you realize a capital gain. Conversely, selling it for less than the cost basis results in a capital loss. It’s crucial to report these gains or losses on your tax form, to ensure compliance with IRS regulations.

The distinction between short-term and long-term capital gains adds further complexity as the capital gains tax rate that you pay depends on how long you have held assets for. You must determine if you have held them for a short or long term. The holding period begins on the day after you acquired the cryptocurrency and ends on the day you sell or exchange the cryptocurrency.

Short term capital gains tax

Cryptocurrency held for less than a year when disposed of is considered a short term gain and is taxed at the same rate as your ordinary income.

Short term capital gains tax rates

| Tax rate | Single | Head of household | Married filing jointly | Married Filing separately |

|---|---|---|---|---|

| 10% | $0 - $11,000 | $0 - $15,700 | $0 - $22,000 | $0 - $11,000 |

| 12% | $11,001 - $44,725 | $15,701 - $59,850 | $22,001 - $89,450 | $11,001 - $44,725 |

| 22% | $44,726 - $95,375 | $59,851 - $95,350 | $89,451 - $190,750 | $44,726 - $95,375 |

| 24% | $95,376 - $182,100 | $95,351 - $182,100 | $190,751 - $364,200 | $95,376 - $182,100 |

| 32% | $182,101 - $231,250 | $182,101 - $231,250 | $364,201 - $462,500 | $182,101 - $231,250 |

| 35% | $231,251 - $578,125 | $231,251 - $578,100 | $462,501 - $693,750 | $231,251 - $346,875 |

| 37% | $578,126+ | $578,101+ | $693,751+ | $346,876+ |

Long term capital gains tax

Cryptocurrency held for over a year when it is disposed of is considered a long-term capital gain or loss, and is typically taxed at a lower rate than ordinary income.

Long term capital gains tax rates

| Tax rate | Single | Head of household | Married filing jointly | Married filing separately |

|---|---|---|---|---|

| 0% | Up to $44,625 | Up to $59,750 | Up to $89,250 | Up to $44,625 |

| 15% | $44,626 to $492,300 | $59,751 to $523,050 | $89,251 to $553,850 | $44,626 to $276,900 |

| 20% | Over $492,300 | Over $523,050 | Over $553,850 | Over $276,900 |

How to calculate capital gain for crypto

Capital gain or loss is the difference between the cost basis of your cryptocurrency and the value you received in exchange for your cryptocurrency when sold. This is reported on your federal income tax return in U.S. dollars.

As a basic calculation, CAPITAL GAIN/LOSS = PROCEEDS (the amount of money you received from disposing the cryptocurrency) - COST BASIS (usually the cost to originally acquire the cryptocurrency)

If the proceeds exceed the cost basis, you experienced a capital gain on the cryptocurrency. If the cost basis exceeds the proceeds, you experienced a capital loss on the cryptocurrency.

Disposal proceeds

The disposal proceeds, the amount received from selling or exchanging crypto, are vital for calculating taxable capital gains or losses. Whether you sell the crypto asset for cash, trade for another cryptocurrency, or make a purchase, you’ll need to accurately determine its fair market valuation in USD for the transaction date.

Cost basis

For those who have purchased cryptocurrency at different times and prices, determining the correct cost basis can be difficult. For example, if you bought 3 BTC but on different dates at different prices and have sold 1 BTC, how do you decide which Bitcoin you sold?

To determine the order in which your tokens are sold, you need to decide on a cost basis method. Different methods can significantly impact your capital gain or loss therefore some of these cost basis methods are controversial. The IRS prefers simplicity and consistency and so Specific ID followed by FIFO are our recommended methods.

Cost basis methods

- Specific Identification (SpecID) - If you can specifically identify the unit or units involved in the trade, then you can select which units are deemed to be sold.

- First-in, first-out (FIFO): units are sold or disposed of in a chronological order beginning with the earlier or first unit acquired

- Last-in, first-out (LIFO): the last assets you bought are the first assets you sold or exchanged.

- Highest-in, first-out (HIFO): assumes the most expensive asset you bought is the first asset you sold or exchanged

- Lowest-in, first-out (LOFO): assumes the least expensive asset you bought is the first asset you sold or exchanged

Below we explore the effect of different cost basis methods using the following example:

- On 09/22/2017 Dave bought 1 BTC for 2,000 USD.

- He buys 2 BTC for 5,000 USD on 01/06/2018 and then buys 1 BTC for 8,000 USD on 04/19/2018.

- On 05/03/2018 Dave sold 1 BTC for 4,000 USD.

| Type | Date | Amount | Price | Cost Basis |

|---|---|---|---|---|

| Buy | 09/22/2017 | 1 BTC | 2,000 USD | 2000 USD |

| Buy | 01/06/2018 | 2 BTC | 5,000 USD | 5,000 USD |

| Buy | 04/19/2018 | 1 BTC | 8,000 USD | 8,000 USD |

| Sell | 05/03/2018 | 1 BTC | 4,000 USD | ? |

FIFO: First-in, first-out

(Default method by the IRS) Assumes that the first assets you purchased are the first assets you sold or exchanged. So, using this method your gains are calculated using the price paid for the oldest assets in your portfolio, and the asset price at the time of disposal.

- The first coin was bought on 09/22/2017 for 2,000 USD, so his cost basis is 2,000 USD.

- 4,000 - 2,000 = +2,000 USD (profit)

LIFO: Last-in, first-out

Assumes the last assets you bought are the first assets you sold or exchanged. Using this method your gains are calculated by using the price you paid for the most recently purchased assets and the asset price at time of disposal.

- The last coin was bought on 04/19/2018 for 8,000 USD, so Dave's cost-basis is 8,000 USD

- 4,000 - 8,000 = -4,000 USD (loss)

HIFO: Highest-in, first-out

Calculated using the highest purchase price first, generating the lowest total gain.

- The highest purchase price was on 04/19/2018 for 8,000 USD, so his cost basis will be 8,000 USD.

- 4,000 - 8,000 = -4,000 USD (loss)

LOFO: Lowest-in, first-out

Calculates the highest total gain by using the lowest purchase price first.

- The lowest purchase price was on 09/22/2017 for 2,000 USD, so his cost basis will be 2,000 USD

- 4,000 - 2,000 = +2,000 USD (profit)

Seek professional advice

Consult a tax professional to see if your transactions meet the requirements for specifical identification.

Find out more about crypto cost basis in our <cost basis article name> including tips and best practice for record keeping.

Crypto losses tax

Crypto losses can offset capital gains from crypto within the same tax year helping to reduce your tax liability. If losses surpass gains, you can deduct up to $3,000 against ordinary income, with any remaining losses carried over to future tax years. To maximize these deductions make sure your record keeping is accurate.

How is lost and stolen cryptocurrency taxed?

The IRS is clear that you cannot claim a capital loss for lost or stolen crypto whether it’s due to lost keys or a hack or scam.

Under the Tax Cuts and Jobs Act (TCJA) passed in 2017, losses as a result of stolen cryptocurrency are generally not deductible unless attributable to a federally declared disaster. While there are other types of losses that were not suspended by the TCJA, the IRS has not provided guidance on when it is appropriate to use such methods, as such, individual tax preparers may take certain tax positions based on facts and circumstances. If your loss is of a substantial size, we recommend you seek help from a <crypto CPA>.

Some taxpayers might also argue that the hacked/stolen crypto is now “worthless” and therefore sold as $0. As a result, you would record a capital loss in the amount of the original cost basis.

Crypto income tax

In the US, various crypto transactions can be categorized as ordinary income, making them taxable as ordinary income rather than capital gains. Think of it this way: anytime you're 'earning' crypto, it's probably liable to income tax, for example receiving airdrop rewards, staking rewards, or mining rewards. Let’s dive into income tax rates and find out how to calculate income tax on crypto.

Federal income tax rates

Your rate of income tax (tax bracket) depends on your taxable income and your filing status. The United States has a progressive tax system, meaning people with higher taxable incomes pay higher federal income tax rates. You won't pay the same tax rate on your entire income, you will be taxed at the corresponding tax rate for your earnings within each bracket.

Single filers

| Tax rate | Taxable income bracket | Tax owed |

|---|---|---|

| 10% | $0 to $11,000 | 10% of taxable income |

| 12% | $11,001 to $44,725 | $1,100 plus 12% of the amount over $11,000 |

| 22% | $44,726 to $95,375 | $5,147 plus 22% of the amount over $44,725 |

| 24% | $95,376 to $182,100 | $16,290 plus 24% of the amount over $95,375 |

| 32% | $182,101 to $231,250 | $37,104 plus 32% of the amount over $182,100 |

| 35% | $231,251 to $578,125 | $52,832 plus 35% of the amount over $231,250 |

| 37% | $578,126 or more | $174,238.25 plus 37% of the amount over $578,125 |

Head of household

| Tax rate | Taxable income bracket | Tax owed |

|---|---|---|

| 10% | $0 to $15,700 | 10% of taxable income |

| 12% | $15,701 to $59,850 | $1,570 plus 12% of the amount over $15,700 |

| 22% | $59,851 to $95,350 | $6,868 plus 22% of the amount over $59,850 |

| 24% | $95,351 to $182,100 | $14,678 plus 24% of the amount over $95,350 |

| 32% | $182,101 to $231,250 | $35,498 plus 32% of the amount over $182,100 |

| 35% | $231,251 to $578,100 | $51,226 plus 35% of the amount over $231,250 |

| 37% | $578,101 or more | $172,623.50 plus 37% of the amount over $578,100 |

Married, filing jointly

| Tax rate | Taxable income bracket | Taxes owed |

|---|---|---|

| 10% | $0 to $22,000 | 10% of taxable income |

| 12% | $22,001 to $89,450 | $2,200 plus 12% of the amount over $22,000 |

| 22% | $89,451 to $190,750 | $10,294 plus 22% of the amount over $89,450 |

| 24% | $190,751 to $364,200 | $32,580 plus 24% of the amount over $190,750 |

| 32% | $364,201 to $462,500 | $74,208 plus 32% of the amount over $364,200 |

| 35% | $462,501 to $693,750 | $105,664 plus 35% of the amount over $462,500 |

| 37% | $693,751 or more | $186,601.50 + 37% of the amount over $693,750 |

Married, filing separately

| Tax rate | Taxable income bracket | Taxes owed |

|---|---|---|

| 10% | $0 to $11,000 | 10% of taxable income |

| 12% | $11,001 to $44,725 | $1,100 plus 12% of the amount over $11,000 |

| 22% | $44,726 to $95,375 | $5,147 plus 22% of the amount over $44,725 |

| 24% | $95,376 to $182,100 | $16,290 plus 24% of the amount over $95,375 |

| 32% | $182,101 to $231,250 | $37,104 plus 32% of the amount over $182,100 |

| 35% | $231,251 to $346,875 | $52,832 plus 35% of the amount over $231,250 |

| 37% | $346,876 or more | $93,300.75 plus 37% of the amount over $346,875 |

How to calculate crypto income

Calculating your crypto income tax is fairly straightforward, simply determine the fair market value of the received crypto in USD on the day of acquisition. This figure represents your earnings and serves as the taxable amount, subject to your Federal Income Tax rate and potentially your State Income Tax rate when fulfilling your tax obligations.

Employment income

Today, a growing number of employees and contractors are being paid in cryptocurrency for work that they perform . Cryptocurrency received as compensation from employment or other work you perform would be considered ordinary income under US tax law.

It is taxed at the fair market value at the time you have dominion and control (generally when it is received). It is then reported on your tax return as ordinary income, like a regular paycheck or freelance income (depending on the nature of the income). The amount of tax you pay will be based on the marginal tax rate.

If you get paid in crypto as an employee, you do not have to worry about making the crypto to USD conversion as this amount will be added by your employer on your Form W-2. If you get paid as a contractor, however, the company paying you might issue you a Form 1099-NEC reporting this amount; if they do not, you are still responsible for this tax.

Example:

- Louise gets paid 1 BTC on 01-31-2022 for working at Crypto-corp.

- When this BTC arrives in her wallet, she checks the current market value of that asset ($50k).

- When she receives her W-2 for the year, she sees this amount added to her Box 1 wages.

Do you pay tax when buying crypto in the US?

When buying crypto in the US, whether or not you pay tax depends on the method and currency you use to purchase the asset. Here’s a breakdown of the tax implications for different scenarios.

Buying crypto with USD

If you purchase cryptocurrency with fiat currency like USD, you won’t be taxed at the time of purchase. However it is crucial to maintain a record of these transactions so you can calculate your capital gain/loss when eventually disposing of the asset.

Buying and HODLing crypto

When you buy cryptocurrency and hold on to it - known as HODLing, this action is not taxable as you continue to retain the crypto. Nevertheless, you should keep a record of your acquisition cost for calculating the gains or losses for future taxable disposals. It’s also helpful to note when you move crypto between your own wallets and accounts in case this is ever incorrectly tracked as a disposal.

Buying crypto with crypto

Trading or swapping one crypto asset for another is subject to capital gains tax. Many crypto investors overlook this when filing their taxes because they are not “cashing out”. However you are disposing of one crypto asset and acquiring another. The disposal realizes a capital gain or loss and therefore is subject to capital gains tax. The sterling market value of the crypto asset disposed of is used as the disposal proceeds in the calculation of the capital gain or loss and is also recognized as the acquisition cost of the crypto asset acquired in the exchange.

Buying crypto with stablecoins

Buying crypto with stablecoins is treated similarly to buying crypto with crypto and is subject to capital gains tax. Stablecoins are designed to maintain a relatively stable value, because they are typically pegged to a currency or commodity. While it’s unlikely you will recognize a gain or loss substantial enough to impact the tax payable, it is still essential to record these transactions for tax purposes. Investors are often surprised that they realize gains or losses on trading in and out of stablecoins; but this is inevitable due to fluctuation of the price of the pegged currency to sterling between acquisition and disposal of the stablecoin.

Buying and HODLing stablecoins

There is a lot of misconception around taxation of stablecoins because of their nature.However, the reality is that they are subject to the same tax treatment as other cryptocurrencies. Hence, any earnings accrued from holding stablecoins, such as yield, interest, or staking rewards, are taxable.

Do you pay tax when selling crypto in the US?

Yes, you have to pay tax when selling crypto in the US, short-term capital gains are taxed at a rate of 10% to 37% and long-term capital gains from 0% to 20%.

Selling crypto for fiat currency (USD)

Crypto sold for fiat money like USD is treated as a taxable disposal, subject to capital gains tax. To calculate the capital gain or loss, subtract the cost basis of the asset from the fair market value of the asset (sale proceeds) on the day you dispose of it.

Selling crypto for another crypto

Selling (or trading) one crypto asset for another is subject to capital gains tax.This process is recognized as a disposal of one crypto asset and the acquisition of another. The disposal realizes a gain or loss and therefore must be subjected to capital gains tax. The fair market value of the crypto asset disposed of is used as the disposal proceeds in the calculation of the capital gain or loss and is also recognized as the acquisition cost of the crypto asset acquired in the exchange.

Do you pay tax when spending crypto?

Yes, spending crypto is classed as a taxable disposal by the IRS. When you make a purchase using cryptocurrency, it is treated as if you sold the crypto for fair market value, as such events like the below may realize a capital gain or loss.

- Paying fees on trades, withdrawals and deposits of crypto

- Buying a pizza

- Paying for accountancy services

When you pay for goods and services using cryptocurrency, the IRS views that you are effectively exchanging that capital asset for property or service.This could be for a crypto related service or for a “real world” transaction like using crypto to pay for a coffee.

As a rule of thumb, the cost of the services you receive is your proceeds, and you subtract that from the original cost basis of the cryptocurrency you spent. The difference between these amounts is your capital gain or loss.

If you use virtual currency to purchase property, the cost of the purchased property is used as the proceeds of the transaction. The gain or loss is the difference between the cost of the property and your adjusted basis in the cryptocurrency exchanged. When using crypto to purchase goods or services, the transaction should be considered at ‘arm’s length,’ meaning it reflects the fair market value. Typically, this is the price you actually paid for the goods or services unless they were acquired below the market value.

How are crypto-to-crypto trades taxed?

When swapping one cryptocurrency for another, including stablecoins, it triggers a capital gain or loss based on the fair market value at the time of the exchange. The IRS views the exchange as a disposal of one cryptocurrency and an acquisition of another; it is treated the same as if you sold the first for cash and then used the cash to buy the second.

The capital gain or loss is the difference between the fair market value of the cryptocurrency you received and the original cost basis of the cryptocurrency you exchanged.

Crypto to crypto trades are not like-kind exchanges

Like-kind exchanges allow for exchange of property of like-kind or similar nature without tax being applied (26 U.S.C. § 1031). Many traders wrongly assume that crypto to crypto transactions like exchanging Bitcoin for Ethereum meet this description. However, since 2018, like-kind exchanges are limited to real estate. Furthermore,the IRS has clarified that even exchanges prior to 2018 do not qualify as for like-kind exchange treatment.

Is transferring crypto a taxable event?

No, in the US, transferring cryptocurrency tokens between wallets or exchange accounts you own is not subject to tax, as they are not taxable disposals. It is important however, to keep records of all transfers in case they are ever incorrectly assumed to be disposals.

Are transfer fees taxable?

Transfer fees from your exchange or wallet when moving crypto between accounts, may be taxable. When the transfer fee is paid in crypto, it is considered that you are spending crypto, which is regarded as a disposal subject to capital gains tax and you will need to calculate the gain or loss.

Find out more in our article <Do you pay tax when transferring crypto?> where we go into detail about where tax needs to be considered for more complex transfers like adding/removing liquidity and transfers between different blockchains.

Taxes on crypto gifts and donations

When it comes to gifting and donating cryptocurrency in the US, it’s important to understand the tax implications. In most cases, gifting cryptocurrency is considered non-taxable and donations to registered charities do not realize a capital gain or loss and can be claimed as a tax deduction. However, there are some exceptions and specific rules for gifts and donations that should be followed to ensure compliant tax reporting.

How are crypto gifts taxed?

In most instances crypto gifts are tax free, but let’s explore the tax consequences for the gifter and receiver in more detail.

Tax on gifting crypto

Individuals can gift up to $17,000 per recipient in the 2023 tax year ($18,000 in 2024) before incurring any gift tax liability. Assets can be gifted all at once or in more than one transaction but must not exceed the annual threshold. If you pass the annual gift tax exclusion amount, then you’ll have to file a gift tax return using form 709, but you will only pay gift tax on the amount over $17,000 if you exceed the lifetime gift tax exemption of $12.92 million (2023).

Receiving a crypto gift

When you receive a crypto gift, you do not generate a taxable event until you dispose of the asset. The IRS have confirmed that virtual currency received as a bona fida gift is not income.

Selling a crypto gift

When you eventually sell or dispose of a crypto gift it should be treated for capital gains tax. Your cost basis for the gift depends on whether you will have a gain or loss when you sell it.

Providing the fair market value of the gift at the time you received it was equal to or more than the gifter's cost basis, you will inherit their cost basis of the asset. If the fair market value of the gift at the time you received it was less than the donor's cost basis, then the cost basis for your disposal is:

For a gain – the donor’s cost basis

For a loss – the fair market value at the time you received the gift.

This ensures there is no sharing of losses in order to deduct against capital gains.

You must be able to prove the gifter's cost basis

It’s crucial to get documentation from the gifter’s original acquisition information for the crypto asset to substantiate their cost basis. Without this the IRS may deem the receiver’s cost basis to be zero which can dramatically increase the capital gain and tax liability.

How are crypto donations taxed?

If you donate cryptocurrency directly to a qualified charitable organization (described under Section 170(c) of the IRS’ tax code), then you can potentially avoid capital gains tax liability and claim a charitable deduction on your tax return for the fair market value (FMV) of your cryptocurrency at the date of donation.

Non-cash donations over $500 need to be reported on Form 8283 of your tax return. Although you are not required to provide receipts or other records of your donations here, it’s important to maintain records in case the IRS requests evidence. If you donate more than $5,000 you’ll need a qualified appraisal and the charity is also normally required to sign Form 8283 acknowledging receipt of the asset.

The amount that can be deducted on your tax return depends on how long you held the donated crypto for:

If you owned cryptocurrency for more than 1 year at the time of donating it, your charitable deduction is equal to the FMV of the virtual currency at the time of the donation.

If you owned cryptocurrency for 1 year or less at the time of donating it, your charitable deduction is equal to the lesser of your cost basis or the virtual currency’s FMV at the time of the contribution.

How are airdrops and forks taxed?

In 2019, the IRS issued guidance that crypto received as a result of an airdrop or a hard fork, is treated as ordinary income. They also confirmed that because this was clarification of already existing code any forks or airdrops that occurred before 2019 should also be treated this way. Below we explore the taxation of airdrops and forks in more detail.

How are airdrops taxed?

Crypto assets received as airdrops are taxable as ordinary income when received and subject to capital gains tax when later disposed of. The amount reported as ordinary income becomes your cost basis in the tokens.

Income tax on airdrops

To calculate the income tax on an airdrop you need to determine the fair market value (FMV) of the received tokens at the time of the airdrop. The FMV represents your taxable income, and you're required to report it on your tax return and will be taxed at your income tax rate.

Capital gains tax on airdropped assets

If the airdropped tokens are later sold, the sale would incur capital gains tax. The fair market value of the crypto asset is treated as the acquisition cost for capital gains tax purposes.

How are forks taxed?

In the United States, forks might be reported as ordinary income and capital gain income depending on the transaction. Whereas capital gains tax always applies when the asset is eventually disposed of, whether a fork is considered ordinary income at the time of receipt depends on if a soft fork or hard fork occurs.

What is a crypto fork?

Some crypto assets operate by consensus amongst their community; when a significant part of the community wants to do something different they may create a ‘fork’ in the blockchain. There are two types of forks, a soft fork and a hard fork, below we explore the different outcomes of each and how this affects the tax consequences.

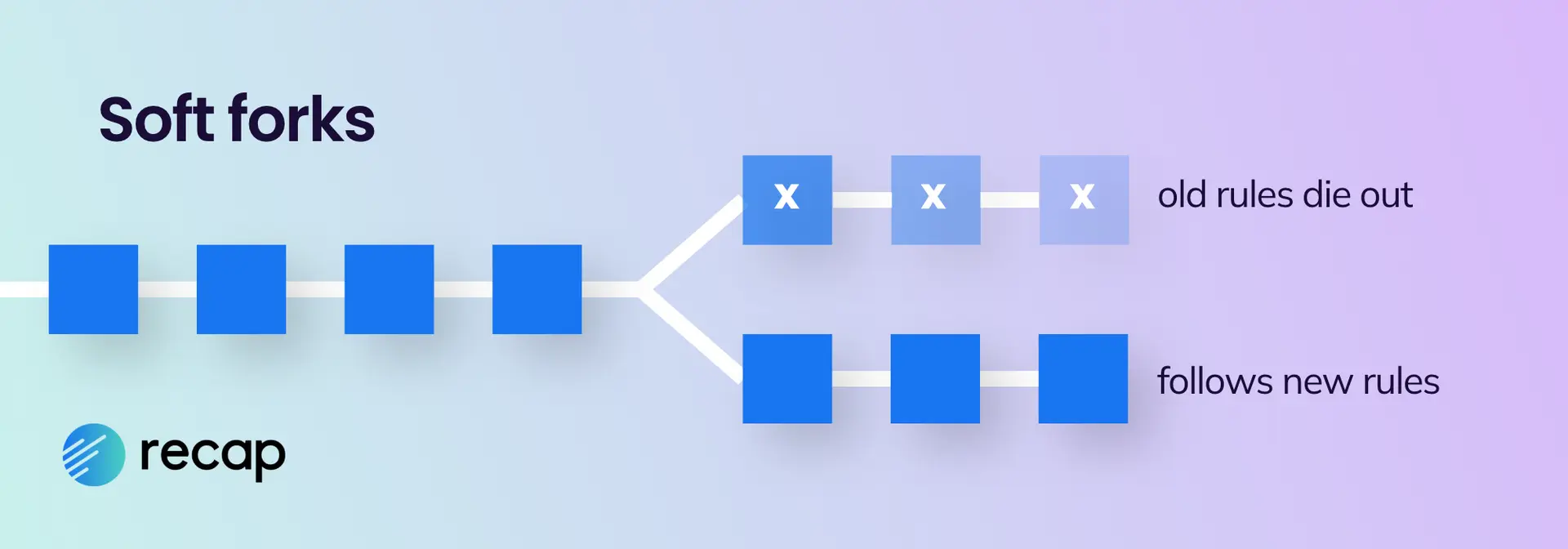

Soft forks

A soft fork updates the protocol and is intended to be adopted by all. As no new tokens or distributed ledger are expected to be created there is no taxable event. When the asset is later sold then the disposal should be treated for capital gains tax as normal.

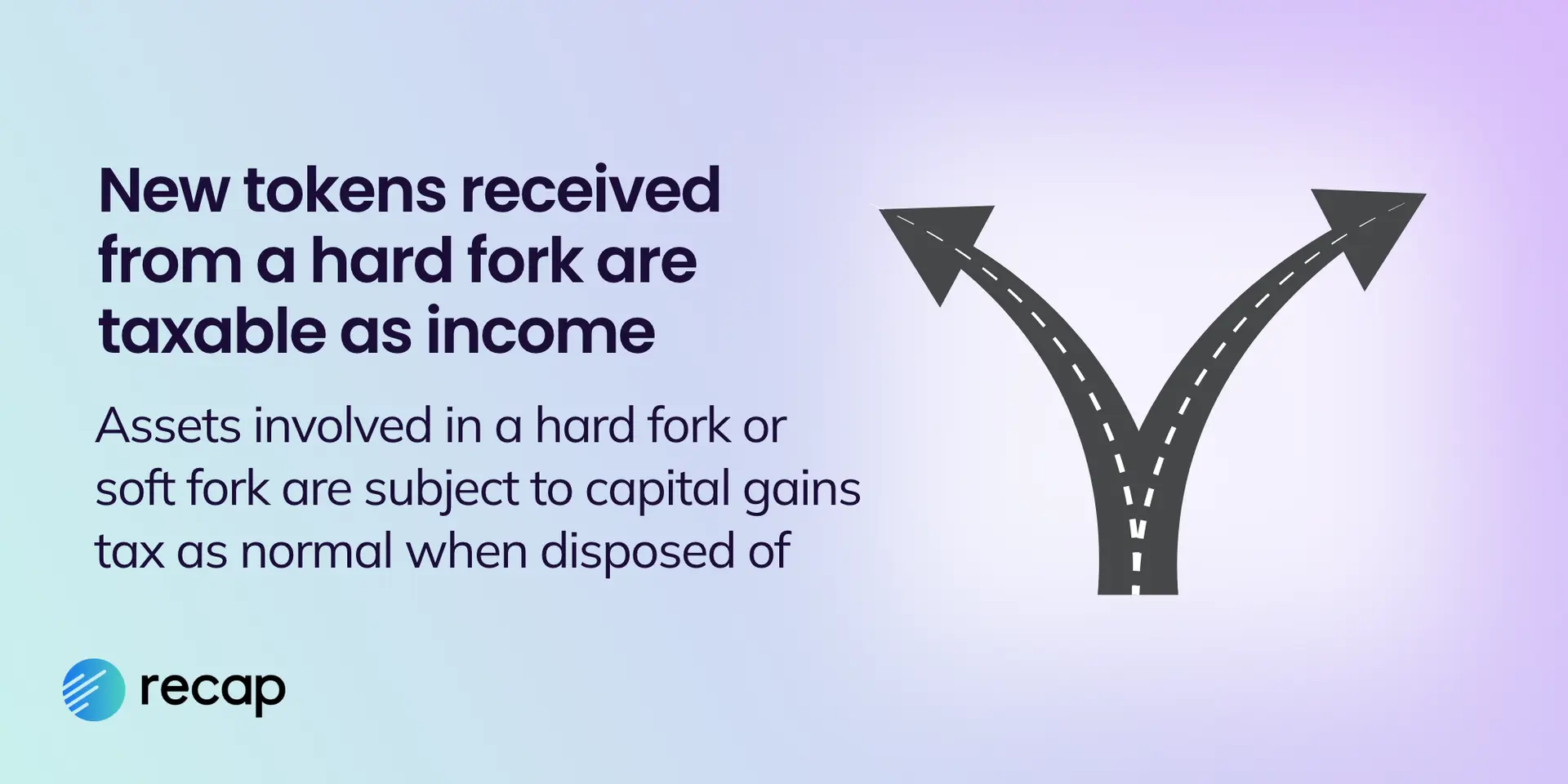

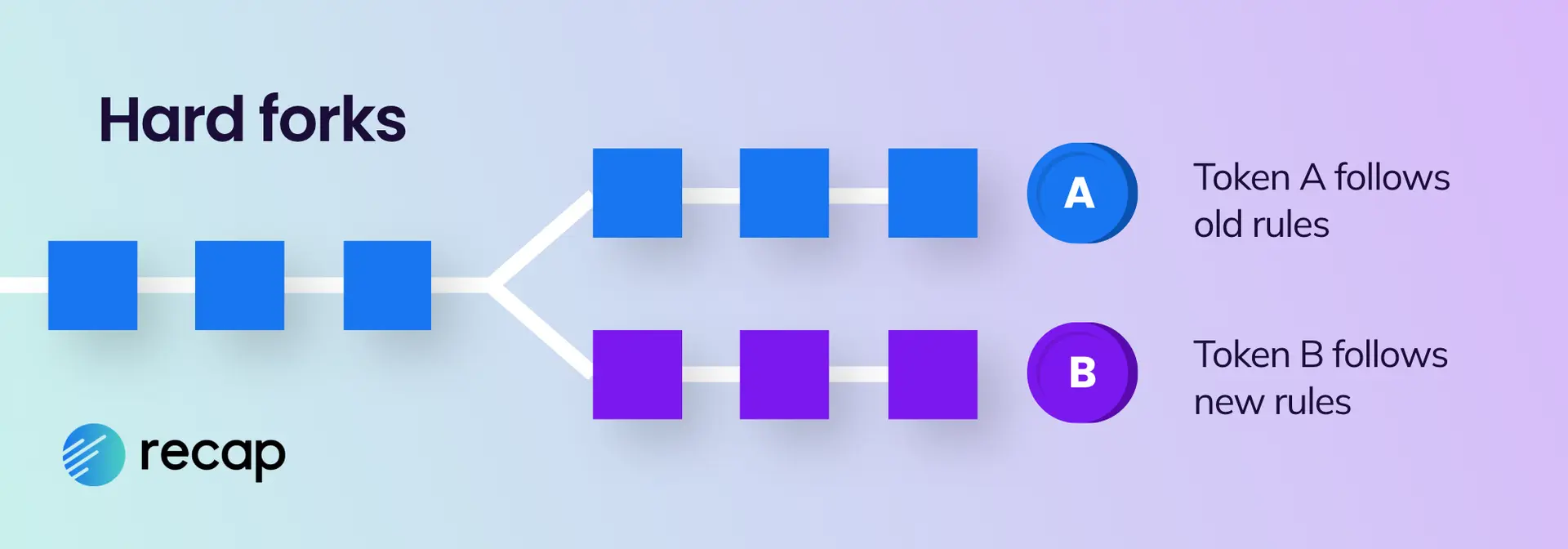

Hard forks

A hard fork can result in new tokens coming into existence. Before the fork occurs there is a single distributed ledger. Usually, at the point of the hard fork, a second branch (and therefore a new crypto asset) is created and individuals typically receive new tokens. The IRS has confirmed this is taxable as ordinary income.

The distributed ledger for the original and the new crypto assets have a shared history up to the fork. If an individual held tokens of the crypto asset on the original distributed ledger they will, usually, hold an equal number of tokens on both distributed ledgers after the fork. The value of the new tokens is derived from the original tokens already held by the individual.

To calculate the amount of taxable income, you'll need to identify the FMV of the tokens on the date of receipt. When you later sell (dispose of) the tokens you’ll also be liable for capital gains tax and this value is treated as the cost basis for the capital gains calculation.

How is mining cryptocurrency taxed?

Whether you mine as a hobby or as part of a business, crypto received as a result of mining activities is treated as income. Income from mining will be taxed based on the fair market value of your mining rewards at the time of receipt. You will also be liable for capital gains tax when you eventually dispose of mined tokens depending on their change in value.

Mining as a hobby

If you are mining as a hobby, you need to declare the proceeds as “other income” on Schedule 1 of your tax return. Prior to the changes introduced by the Tax Cuts and Jobs Act (TCJA), hobby losses could be deducted but only up to hobby income. However, due to the suspension of miscellaneous itemized deductions by the TCJA, hobby expense deductions are not allowed between tax years 2018 - 2025.

Mining as a business

If you've organized a business as a sole proprietorship or a single member LLC, you should report your mining income on form 1040, Schedule C. Businesses can claim further deductions related to their mining operations including:

- Equipment and repair expenses

- Office/ rented space

- Electricity

- Any losses

For further information and more clarification between hobby and business mining refer to our article <How crypto mining is taxed>.

Not all mining is a business

Please consult a tax professional to help assess if your mining activity would be considered a business.

How is staking cryptocurrency taxed?

There are two types of staking to be aware of within crypto - staking as part of a proof of consensus mechanism (PoS) and DeFi staking. In most instances staking rewards should be reported as ordinary income and as capital gains when later disposed of.

Staking as part of a PoS consensus mechanism

When you stake some of your crypto to contribute to the Proof of Stake (PoS) network of that asset, you earn more assets from the network at a percentage rate over time as a reward. This reward is subject to ordinary income at the fair market value at the time received.

DeFi staking

In contrast, DeFi staking involves lending your cryptocurrency through specific DeFi protocols, receiving crypto income from the borrowers. The tax implications depend on the terms and mechanics of the protocol. If you earn new tokens, income tax is likely applicable however if you deposit capital and receive LP tokens which increase in value then this may be treated as a crypto to crypto trade subject to capital gains tax.

IRS 2023 staking guidance

The IRS released guidance in 2023 confirming that staking rewards are taxable income when received, although they didn’t distinguish between PoS and DeFi staking. They clarified that staking rewards are received when “the taxpayer gains dominion and control over the validation rewards”.

Is crypto cashback taxable?

Some large providers (such as crypto.com) offer users a cashback card, which is like a debit card, and can be used to make purchases of goods and services in fiat from most retailers (ie for your groceries, buying a car or a TV). Cashback rewards are received in cryptoassets (ie in CRO/MCO on crypto.com) for using the cashback card, based on the amount of purchases made with the card.

Although the IRS have not officially released guidance on crypto cashback, based on existing guidance, it’s likely “cash-back” rewards should be considered as non-taxable “rebates.” The IRS has previously used this treatment for traditional cash-back rewards, points, and airline miles earned through credit cards.The rationale for this tax treatment is that the rewards are an after the fact discount to the underlying purchase price.

They will, however, be liable for income tax on any capital gains when later disposed of, so it's important to note the cost basis of any assets that you receive as a reward so you can calculate the gain or loss.

How is margin, futures and CFDs trading taxed?

Individual traders will pay capital gains tax on any margin trades or other CFDs. When you open a new position, you pay no tax, however, when this position closes a taxable event occurs and you realize a capital gain or loss. The normal short-term and long-term capital gains tax rates apply to these transactions.

If you're trading regulated crypto futures, you can apply the IRS’ 60/40 rule to get a more favorable tax treatment. This rule allows investors to treat 60% of their gains as long-term gains and 40% as short term gains regardless of how long a position is kept open. However, the vast majority of crypto futures are unregulated and as such these rules cannot be applied.

How do DeFi taxes work?

The decentralized finance (DeFi) landscape has experienced exponential growth in recent years, however the IRS is yet to introduce formal guidance specifically tailored to DeFi transactions. While we wait for clarity it’s important to stay compliant and recognize that the usual tax principles and tax rules for crypto apply to DeFi as well. Think of it this way: if you make profits from crypto disposals, it's treated as capital gains. And if you're raking in those DeFi rewards, that's likely counted as regular income. We explore some of the popular activities below.

Selling tokens on DeFi protocols

Selling or trading tokens on DeFi protocols is likely to be viewed as a disposal and any profits subject to capital gains tax just like sales made on centralized crypto platforms.

Receiving rewards and interest

When you earn rewards in the form of new tokens you will be subject to income tax based on the fair market value of the reward when received. When your rewards are “locked up”, the income is not recognised until you have control of the asset.

If you earn a reward in the form of your token accruing in value then you will be subject to capital gains tax on its disposal.

How is liquidity mining taxed?

When you deposit a pool with liquidity, you are often rewarded with Liquidity Provider (LP) tokens in proportion to the amount of liquidity.This may be considered a crypto to crypto trade liable for capital gains tax. When you withdraw from the pool, you’ll often trade your LP tokens to access your crypto. This is also likely considered a crypto to crypto trade that is subject to capital gains tax.

How are loans taxed?

Loans have long been considered non-taxable by the IRS. It’s reasonable to assume that cryptocurrency loans will be treated the same way.

That said, some decentralized protocols use crypto-to-crypto swaps to facilitate loans. For example, if you use BTC as collateral on a platform, you might be given pBTC in return. Swaps typically generate a taxable event and given the lack of explicit guidance from the IRS, this may be considered a swap rather than a loan.

How you choose to report this type of loan will depend on if you want to take an aggressive stance or a more conservative approach to your tax position. A conservative view would treat the loan as a swap for a new token and as such treat this as a disposal subject to capital gains tax depending on how the value of the asset has changed. An aggressive approach would treat this entirely as a loan, treating the new token as a 'claim ticket' and avoid declaring anything to the IRS.

For more detailed information and guidance on DeFi taxation in the US, you can refer to our <comprehensive DeFi tax guide>.

How do NFT taxes work?

Are non-fungible tokens taxed?

Like other crypto, NFTs are treated as property so tend to follow the same tax treatment as crypto assets where capital gains or income tax may apply. Below we summarise the tax considerations for NFT creators and investors.

IRS NFT guidance 2023

The IRS announced that some NFTs may be deemed as collectible and under the tax law will be treated for capital gains tax under the higher long-term CGT rate of 28%. Until additional guidance is issued, the IRS intends to determine when an NFT is treated as a collectible by using a "look-through analysis."

Tax for NFT creators

For NFT creators, taxes are relatively simple. Creating an NFT is not a taxable event, but when this asset is disposed of it becomes taxable. Although there is no explicit guidance from the IRS we can assume that primary and secondary sales of an NFT which you created would be subject to income tax. You should declare and use your normal income tax rates when selling an NFT that you created and you may be subject to self-employment income.

Example: Dave creates a piece of art on a canvas. When he creates this art, there is no known value for this piece and there has not yet been a sale and therefore no taxable event. When Dave sells this art for $10,000 he receives this as income for the work that he has done to create the piece. The same logic applies for an NFT created by an artist.

If you are an NFT creator organized as a trade or business these sales are top line revenue, and you could deduct cost / expenses. Find a CPA who can assist you with all required business tax reporting.

Tax considerations for NFT investors

NFT investors are subject to capital gains at the various stages of buying and selling NFTs. Normal short and long term capital gains rules apply but you may also need to consider if your NFT is a collectible and taxed at the higher long-term tax rate of 28%.

Purchasing an NFT

Purchasing an NFT with fiat currency is considered non-taxable, but most NFTs will be bought with cryptocurrency. This is viewed as a taxable event as you are disposing of your crypto asset. You will be subject to capital gains tax depending on how the value of your crypto has changed since you acquired it.

For example, if you purchase an NFT with 1ETH, you are disposing of this ETH and will be subject to capital gains tax on any gains or losses. Depending on how long you held that ETH you would be subject to either the long or short term capital gains tax rate.

You also take ownership of an NFT which has an acquisition value of 1ETH ($10k), when this asset is later sold you are subject to capital gains tax on any gains or losses (see below). You would use the fair market value (FMV) of the ETH at the time you acquired and then sold the asset to calculate its value.

Swapping one NFT for another NFT

Trading one NFT for another NFT triggers a taxable event and is subject to capital gains tax. The rate of capital gains tax depends on how long you held the asset for and whether it is deemed a collectible.

For example, if you bought an NFT for 1 ETH ($1,000) and traded it for another NFT three months later for another NFT which has a FMV of 3 ETH ($3,500) you would incur a taxable capital gain of $2,500, taxed at the short term capital gains rate.

Selling an NFT for cryptocurrency

Whenever you sell an NFT you incur a capital gain or loss in the same way that you would for any other type of crypto asset. The tax you pay depends on if you held the asset short term or long term and if it was classed as a collectible.

For example, if I bought an NTF for 1 ETH ($1,000) and then sold this for 3 ETH ($4,000) I owe capital gains on $3,000.

Determining fair market value of an NFT

Determining the value of an NFT can be challenging and there is some debate about the best way to calculate a fair market value (FMV) for an NFT.

IRS definition of FMV

"Fair market value (FMV) is the price that property would sell for on the open market. It is the price that would be agreed on between a willing buyer and a willing seller, with neither being required to act, and both having reasonable knowledge of the relevant facts.”

You will need to choose a methodology that you feel fairly values your asset and which would be reasonably considered fair to both parties. If you are buying the NFT from an exchange, the assumption is that what you bought it for is its FMV. In this case, the NFT switched hands between a willing buyer and seller at that price, so you can rely on the purchased / sold value for FMV.

Take a look at our <NFT tax guide> for more detail on the taxation of NFTs.

How do you lower your crypto taxes?

Tax compliance is law and declaring your crypto taxes is your legal responsibility, however there are some deductions, allowance and strategies to legally reduce your crypto taxes. Here we summarize some of the more common strategies; we also recommend you speak with a tax attorney or accountant to develop whatever strategies are best for your personal investment and tax situation.

HODL your cryptocurrency for long term gains

Because long-term capital gains are taxed (typically) at a lower rate than short-term capital gains, there’s an incentive for being a “hodlr.” If you hold your cryptocurrency for more than a year before disposing of it, you may realize a lower tax bill.

Understand the taxable income threshold

Capital gains form part of your taxable income (along with wages, business income, interest, etc) and capital gains are taxed at different rates. If your total taxable income falls under the threshold then you have 0 tax and technically don’t have to file (although recommended for other reasons).

A capital gains rate of 0% applies if your taxable income is less than or equal to:

- $44,625 for single and married filing separately;

- $89,250 for married filing jointly and qualifying surviving spouse

- $59,750 for head of household.

A capital gains rate of 15% applies if your taxable income is:

- more than $44,625 but less than or equal to $492,300 for single;

- more than $44,625 but less than or equal to $276,900 for married filing separately;

- more than $89,250 but less than or equal to $553,850 for married filing jointly and qualifying surviving spouse;

- more than $59,750 but less than or equal to $523,050 for head of household.

Select optimal cost basis method

Most crypto investors choose first-in, first-out when calculating their capital gains because it’s the most preferred by the IRS, however selecting a different cost basis method could create big tax savings. It’s best to seek help from a tax professional, but providing you are consistent and can demonstrate how you arrived at the valuation with adequate records and calculations then the IRS should be satisfied.

Offset capital losses against gains

Crypto capital losses can be used to offset capital gains within the same tax year. If your losses outweigh your gains, you can deduct up to $3,000 against ordinary income, with any remaining losses carried over to future tax years.

Tax-loss harvesting

If you’ve found yourself sitting on unrealized losses, assets worth less than their initial value when you first purchased or received them, then you could consider disposing of them to counterbalance capital gains.

You might have heard of the wash sale rule; this rule currently doesn’t apply to crypto, so you can swiftly repurchase the same asset, crystallizing the loss without bidding farewell to your crypto! This process, called tax loss harvesting, capitalizes on a legal loophole, however the IRS has their eye on it so change is likely on the horizon!

Cryptocurrency trading fees

There are some incidental costs of purchase and disposal that can be deducted from capital gains. There is not much IRS guidance on what is acceptable, so the best practice is to assume that if the cost relates to the acquisition and disposal of cryptocurrencies, then it is allowable. Therefore, while cryptocurrency trading fees are likely deductible, transfer fees do not follow this same rule.

Mining expenses

Depending on if you’re a hobbyist or business miner, you may be able to deduct some expenses to reduce your tax liability.

- Hobbyist miners cannot deduct any expenses due to the suspension of miscellaneous itemized deductions by the TCJA between tax years 2018-2025.

- Business miners can deduct the ordinary and necessary business expenses. These should be reported on the proper business schedule or return, such as Schedule C or Form 1120, 1120-S or 1065. If the business operates at a loss, they may be able to use losses to offset other income. It’s advisable to consult a tax attorney or accountant to determine which business deductions are applicable based on personal circumstances.

Hold cryptocurrency in an IRA

Individual retirement accounts (IRAs) are a great option for investors who plan on holding long term. Capital gains or income generated within the IRA from your hodled crypto are shielded from immediate taxation, providing potential for your investment to grow more efficiently over time.

Gift and donate crypto

Gifting and donating crypto both help to reduce taxes. During the tax year, you can gift up to $17k for 2023, $18k for 2024 per recipient tax free. These gifts can be made all at once or in more than one transaction. When donating crypto to a qualified charitable organization you can avoid capital gains tax and claim a charitable deduction on your tax return.

For more tax saving strategies as well as more detail on the above ideas check out our article <link to avoid / reduce tax article>.

How to report crypto in your tax return

Crypto taxes are filed within your annual tax return, below we look at where you need to declare your crypto capital gains and income on the tax forms and the important dates in the tax diary.

How to report crypto capital gains

You should calculate your capital gains using your chosen accounting method and report the gains on Form 8949 and Form 1040 (Schedule D) of your tax return.

Crypto tax form 8949

This form is used in part to report the sale or exchange of capital assets not reported on another form. It lists all of your transactions that qualify as a capital transaction resulting in a capital gain or loss. Information reported on the form includes the date the assets were acquired, the date of disposition, your proceeds (typically the FMV at time of sale), your cost basis, and your gain or loss. At the bottom of the form you need to declare your total proceeds, cost basis, and gains/losses for the year.

Crypto tax form 1040 Schedule D

Schedule D on Form 1040 is used to summarize the overall gain or loss from the transactions reported on Form 8949. All capital losses should be reported on Schedule D of your tax return. It is important to do this as this ensures they can be “claimed” to use against future gains.

How to report crypto income tax

Crypto tax form Schedule 1

Cryptocurrency received and classified as Income should be reported under “Other income” on Line 8 of Schedule 1 of your income tax return.

When do you have to pay taxes on crypto?

The deadline for filing and paying your taxes to the IRS is normally April 15, although holidays and weekends can impact the actual date.

Tax payments are due throughout the year. Most people don't have to worry since if you have a job, your employer withholds taxes and remits throughout the year. If your income has no withholdings (business income, self-employment, crypto gains), then you should make payments throughout the year. Any balance due, is due April 15.

Requesting an extension to file your tax return

To avoid late filing penalties, you can apply for an extension of 6 months by submitting IRS Form 4868 before the April tax return deadline. The due date for extended forms is October 15.

IRS penalties for underpaying taxpayers

Some taxpayers who receive income from crypto, must make quarterly payments to the IRS throughout the tax year. If these tax payments are not sufficient then the IRS can charge penalties and interest. If you owe less than $1,000 or meet one of the criteria below then it’s unlikely you will be penalized, but you will need to pay the remaining tax before the final due date.

- You paid 90% of the total estimated tax for the current year

- You paid 100% of the total tax on the prior year's tax return.

As keeping track of crypto gains can be tricky, this is where crypto tax calculators like Recap, which help you to understand your liability in real-time are particularly useful. We also recommend checking whether you need to make estimated tax payments with a tax professional.

What if you forgot to report your crypto taxes?

The IRS has made it clear that crypto is taxable and tax evasion is fraud so inaccurate tax reporting has consequences. The IRS has sent out educational letters, warning letters and audit letters to investors they believe are underreporting.

For late filed tax returns, there are two penalties that commonly apply - one for filing late and one for paying late. They can add up fast and interest accrues in addition to penalties.

Record keeping for crypto taxes

One of the most important messages to come from growing worldwide regulation on cryptocurrency is the importance of keeping records of all transaction activity. You are responsible for your own data and should be proactive in exporting copies of data from any exchanges and wallets that you use on a regular basis.

What records to maintain?

The Internal Revenue Code and regulations require taxpayers to maintain records that are sufficient to establish the positions taken on tax returns. You should therefore maintain, for example, records documenting receipts, sales, exchanges, or other dispositions of virtual currency and the fair market value of the virtual currency.

Additionally, keeping this data even after submitting tax returns for the relevant year is vital in aiding any potential IRS audits, finding cost bases for future tax returns, and allowing you to adapt to any changes in IRS guidance.

How to calculate your crypto taxes

When it comes to calculating your crypto taxes, a structured approach is key:

- Record all transactions: document every crypto transaction and consider which tax (capital gains or income) applies

- Assign cost basis: attach a cost basis to each transaction, indicating the original value of the cryptocurrency

- Calculate gains or losses: determine capital gains or losses on your disposals by subtracting the cost basis from the proceeds

- Consider holding periods: differentiate between short-term and long-term gains based on the duration of holding

- Account for income: calculate taxable income from activities like staking and mining

Because of the nature of crypto there are typically thousands of transactions to account for and calculating your crypto taxes manually can become extremely tedious. This is the reason why many crypto investors and their accountants consider crypto tax software to be an essential tool.

Accurately calculate your crypto taxes using crypto tax software

Crypto tax software is the fastest and most reliable way to calculate your crypto taxes and generate your crypto tax reports automatically.

You can use Recap to calculate your US crypto tax income and capital gains tax reports by following these steps:

- Sign up for free

Head to recap.io and sign up using your email address or google account. Make sure to backup your recovery key and select your country and tax jurisdiction settings. - Connect to your exchanges and wallets

Automatically sync your transaction data by connecting your exchanges via API or entering your public wallet addresses. Upload additional data via CSV (for example extinct exchanges, old accounts). - Check your data is correct

Ensure all of your historical data is uploaded (our calculator needs your acquisition costs for capital gains calculations). Verify that all transactions are accurately accounted for. - Recap automatically calculates your crypto capital gains, capital losses and income

Our calculator calculates your gain and loss for each disposal made and your income for every receipt. - Generate and download your crypto tax reports

Purchase a Recap subscription and head to the tax page to download your crypto tax reports to attach to your tax return or invite your accountant to finish filing on your behalf.

By using crypto tax software like Recap, you can streamline the process and accurately calculate your crypto taxes while saving time and effort. To find out more visit recap.io.