2022 was an absolute roller coaster ride for the crypto market. Many UK crypto investors have faced losses due to the market's high volatility and the collapse of multiple exchanges. Despite this tax is still due on any gains realised. There is a small silver lining to the situation - as a crypto investor, you can use tax loss harvesting to offset your capital gains and reduce your tax bill.

In this blog, we explore tax loss harvesting with Louise Lane, Head of Crypto Tax at Wright Vigar Chartered Accountants and discover how it can help you recover from your crypto losses in 2022. We'll explain what the term means and how you can claim capital losses to reduce your tax bill.

Capital losses cannot be carried back to an earlier tax year, so 5 April 2023 is the last date you can realise a loss to use in 2022/23.

What is tax loss harvesting?

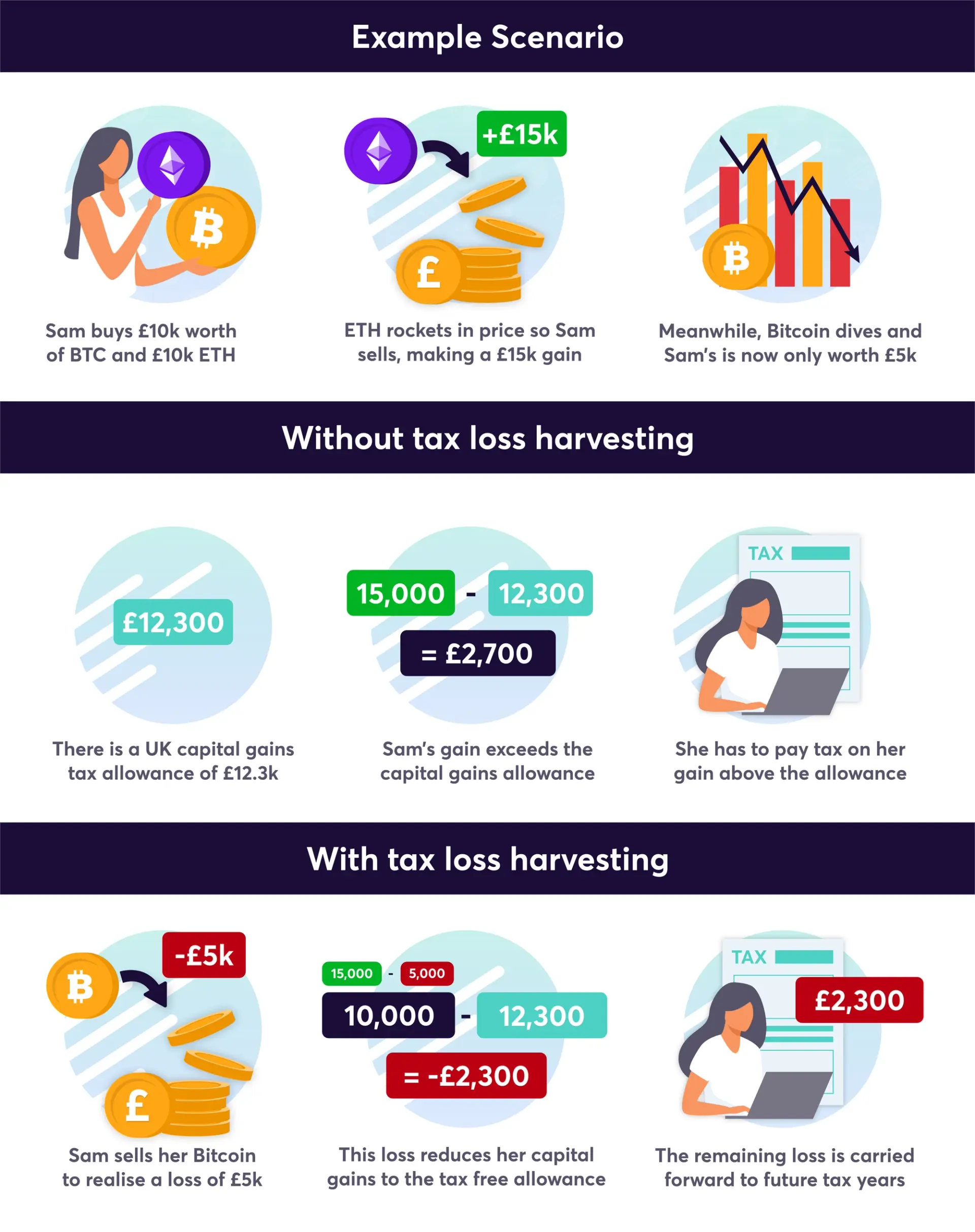

Tax loss harvesting is a term that’s normally heard more in the US and is the process of selling an investment that has experienced a loss to offset the capital gains from other investments, with the goal of minimising your tax liability. Within crypto, tax loss harvesting would involve disposing of assets that have decreased in value to realise losses against taxable gains.

How can tax loss harvesting help UK crypto investors?

If you’re one of the many crypto investors who experienced losses in the crypto market during the 2022 tax year, tax loss harvesting can help you recover. By disposing of cryptoassets that have decreased in value before the end of the tax year, 5th April 2023, you can realise losses to offset capital gains and lower your tax bill due 31st January 2024. In the UK, unused capital losses are rolled forward indefintely so this action could lower your gains for future tax years too, if the loss is not all used in the 2022/23 tax year. With the reduction in 2023/24 to the capital gains allowance, now is a good time to act.

How to claim a capital loss on your crypto?

You may be holding crypto that has decreased in value. It’s important to understand that until you actually dispose of the cryptoasset, ie. sell the asset at a lower price than you paid for it, or make a negligible value claim, you haven’t realised this loss for tax purposes.

You can keep holding an asset while its down, but at this stage it’s a hypothetical loss. Your portfolio could recover, so a loss can only be claimed if it is worthless and qualifies for a negligible value claim. Negligible value claims rely on HMRC’s discretion on whether they accept the tokens were worthless at 5 April 2023 and you have to make a claim for all tokens in the same pool.

For this reason, it is less contentious to physically dispose of the asset. To realise a capital loss you’ll need to physically dispose of the asset that has decreased in value, for example by selling it for fiat, trading it for another crypto or using it to make a purchase.

The capital loss is the difference between the disposal price of the asset and the original acquisition cost; subject to the HMRC matching rules dictating if this is an acquisition on the same day, next 30 days or from the average cost S104 pool.

Beware of the bed and breakfasting rules for cryptoassets that prevent you from realising the expected capital loss. If you buy back the same token within 30 days of the disposal, the new acquisition cost in that following 30 days is deducted in calculating the gain, rather than the S104 pool cost.

NFT’s are not subject to the matching rules, so buying an NFT back at a later date does not affect the capital loss. For NFT’s it is simply disposal price less acquisition cost.

Beware of making a capital loss on gifting crypto or NFT’s to a connected person. Such losses cannot reduce your other capital gains in the tax year and can only be used against future capital gains to the same person. See our [Recap UK Tax Guide](https://docs.recap.io/uk-tax-guide-for-individuals/cryptocurrency-tax/capital-gains-tax/disposals-to-connected-parties) for more details on this.

Recap can help you identify which assets are ideal for tax loss harvesting

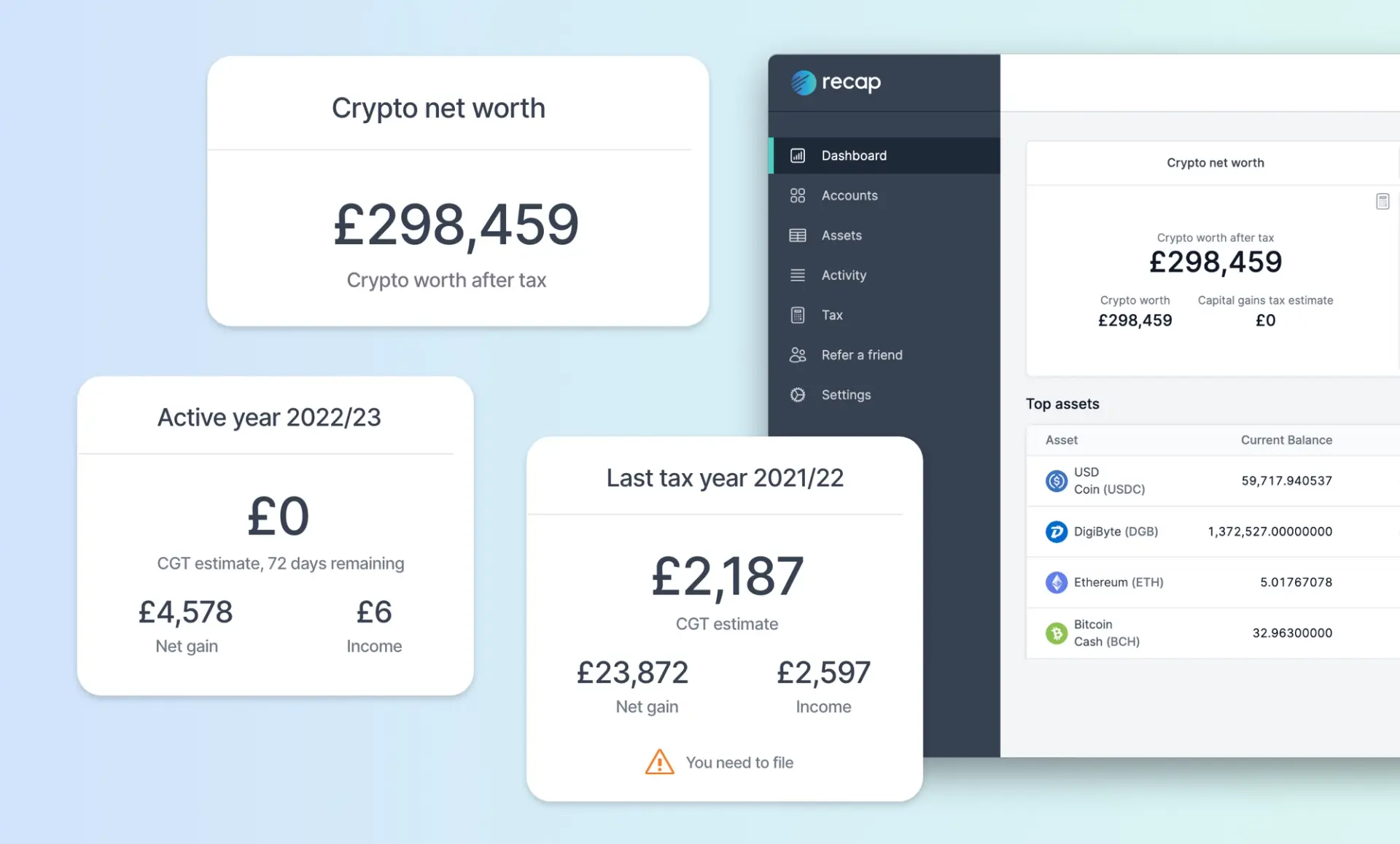

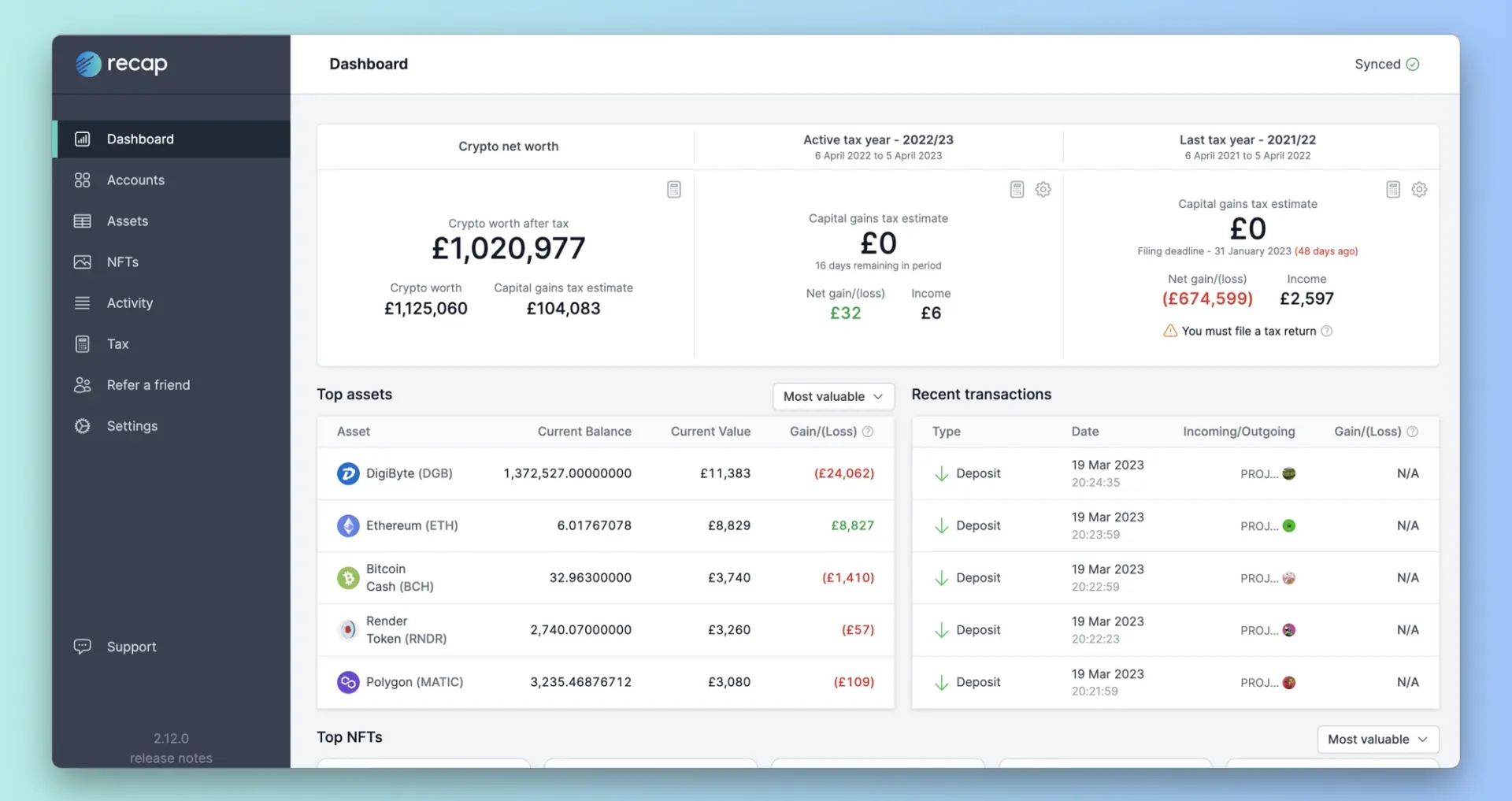

The Recap dashboard gives a live estimate of your capital gains for the open tax year making it easy to understand how much of your annual allowance has been used and how much tax you might need to pay.

The top assets table shows your highest and lowest performing assets, helping you to quickly identify which assets have significantly dropped in value and are therefore optimal for tax loss harvesting.

Seek help from a tax professional and ensure you fully understand the rules

Writing off your losses can dramatically reduce your tax bill, but it’s a strategy that should only be used by those who understand the UK tax rules and are comfortable with the risk of buying and selling cryptocurrency and the volatility of the crypto market. It’s important to consult a tax professional before making any decisions,; they can help you navigate the complex tax rules with more detail, and put together a tax strategy that aligns with your individual situation.

Conclusion

Tax loss harvesting is a smart strategy with massive potential to help UK crypto investors recover from any losses made during the 2022/23 tax year. By realising a capital loss by 5 April 2023, you can offset your capital gains in 2022/23 and reduce your tax bill, and possibly even have losses left to carry forward to future tax years. Capital losses cannot be carried back to an earlier tax year, so 5 April 2023 is the last date you can realise a loss to use in 2022/23. Remember that this strategy is best approached with care by experienced investors or with help from tax professionals like Louise’s team at Wright Vigar.

Disclaimer

This guide is intended as a generic informative piece. This is not accounting or tax advice that can be relied upon for any UK individual’s specific circumstances. Please speak to a qualified tax advisor about your specific circumstances before acting upon any of the information in this article.