Do I need to pay tax on my crypto?

If you have sold, converted, paid or earned using crypto you may owe tax. Even if you are a “Hodlr,” or someone who buys but does not sell their crypto, it’s worth checking. The amount you need to pay depends on how long you have held the crypto and your ordinary income tax rate.

Which Taxes Apply?

In the US, most cryptocurrency taxes fall into two categories: capital gains and ordinary income.

| Disposal/Activity Type | Capital Gains Tax | Ordinary Income Tax |

|---|---|---|

| Selling crypto for fiat | ✅ | ❌ |

| Exchanging one crypto for a different crypto | ✅ | ❌ |

| Purchases using crypto | ✅ | ❌ |

| Mining | ❌ | ✅ |

| Airdrops | ❌ | ✅ |

| Staking | ❌ | ✅ |

| NFTs | ✅ | ✅ (for creators) |

| NFTs earned playing games | ❌ | ✅ |

Capital Gains Tax (CGT)

Capital gains tax may seem straightforward, but you must calculate the gain/loss on each individual cryptocurrency disposal or exchange throughout the whole tax year so need an accurate record of all your transactions. This is where a solution like Recap, which keeps track of transactions and calculates gains/losses is useful.

The IRS separates capital gains into two categories: short term and long term. The amount of capital gains tax that you pay depends on how long you have held assets for.

- gains from the sale or exchange of a capital asset not held for more than 1 year

- taxed at the same rate as your ordinary income

- gains from the sale or exchange of a capital asset held for more than a year

- typically taxed at a lower rate than ordinary income (0%, 15%, or 20% depending on your tax bracket)

Taxable events

Individuals investing in cryptoassets must calculate the capital gain or capital loss they have made whenever they “dispose” of cryptoassets. Examples of disposals are:

- Selling cryptoassets for fiat money (e.g. GBP, USD, EUR).

- Exchanging cryptoassets for a different cryptoasset (e.g. exchanging Bitcoin to Ripple).

- Using cryptoassets to pay for goods or services

Calculating CGT

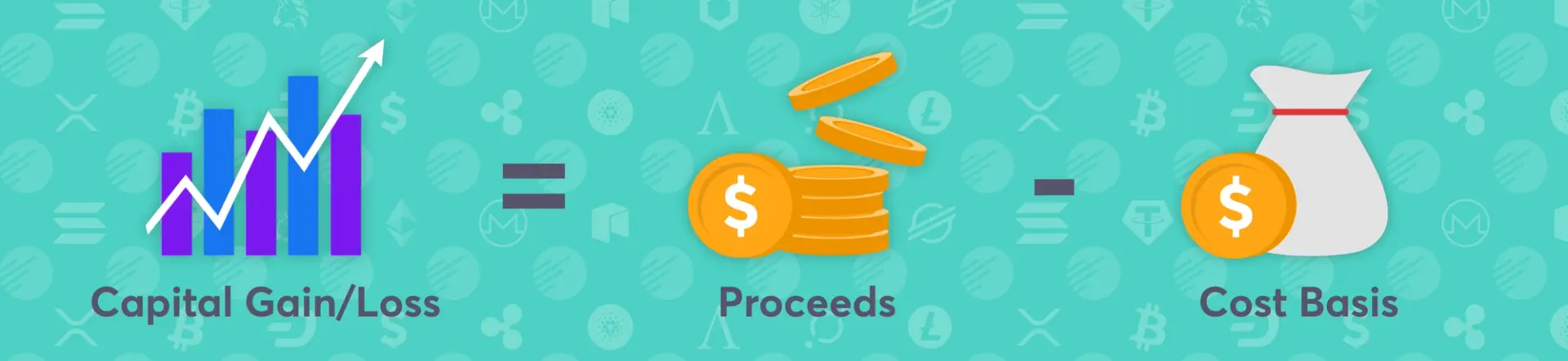

Capital gain or loss is the difference between the cost basis of your cryptocurrency and the value you received in exchange for your cryptocurrency when sold.

CAPITAL GAIN/LOSS = PROCEEDS (the amount of money you received from disposing the cryptocurrency) - COST BASIS (usually the cost to originally acquire the cryptocurrency)

If the proceeds exceed the cost basis, you experienced a capital gain on the cryptocurrency. If the cost basis exceeds the proceeds, you experienced a capital loss on the cryptocurrency.

How to find the cost basis of your crypto

Determining the cost basis can be difficult if you have purchased cryptocurrency at different times at different prices. For example, if you bought 3 BTC but on different dates at different prices and have sold 1 BTC how do you decide which Bitcoin you sold?

The IRS FAQ on Virtual Currency Transactions states that the units are sold or disposed of in a chronological order beginning with the earlier or first unit acquired; that is on a first-in-first-out (FIFO) basis.

If you can specifically identify the unit or units involved in the trade, then you can select which units are deemed to be sold. There are several cost basis methods that might be used for specific identification, such as LIFO or HIFO but you should consult a tax professional before using any of these methods.

Income Tax

As discussed, Capital Gains tax comes from gains realized on the sales of cryptocurrency held and then disposed of via sale or exchange. Cryptocurrency received in other scenarios are often included in the IRS’ definition of income. (26 U.S. Code § 61).

Mining

Crypto received as a result of mining activities is treated as income. If you are mining as a hobby, you need to declare the proceeds as income on schedule C of your tax return.

If you've incorporated a business set up as a sole proprietorship you should report your income on form 1040, schedule C and may be able to claim certain deductions.

Please consult a tax professional to help assess your mining activity.

Airdrops & Hard Forks

In 2019, the IRS issued guidance that crypto received as a result of an airdrop or a hard fork, is treated as ordinary income. (Any forks or airdrops that occurred before this confirmation are still treated this way).

Staking

There has been no official guidance on Staking from the IRS and as such we recommend that you speak with your tax attorney about the best way to file your return.

In general, the IRS considers any increase in value that you receive as income. So, if you receive rewards, it is generally taxed as income at the fair market value at the time received.

NFT’s

NFTs tent to follow the same tax treatment as other crypto assets and coins but this can vary depending on if you created, re-sold or earned an NFT and whether you are the creator or a seller/investor.

The IRS recently issued guidance that some NFTs may be collectibles meaning that the tax rate increases from 20% to 28% for long-term gains. However, they are currently determining this on a case-by-case basis and we await further guidance.

Tax considerations for NFT creators/investors

- Creating or minting an NFT is not a taxable event but when you sell the asset, as the creator you would be subject to income tax.

- An investor or collector selling or swapping an NFT would incur a capital gain or loss in the same way as a disposal of any other cryptocurrency.

- Purchasing an NFT is not taxable however, its likely you are also disposing of a crypto asset (like ETH) in order to buy it which is subject to capital gains tax.

- If you stake an asset and earn an NFT in return this could be viewed as income. If you deposit and asset and receive an NFT in return, this could be assumed to be a swap subject to capital gains tax.

Tax considerations for play-to-earn gamers

There is no IRS guidance on NFT’s or crypto rewards earned whilst gaming, so you would need to examine the circumstances with a tax professional. Although activity varies in different games most involve crypto-to-crypto trades so its likely they are taxable. As NFTs are classed as digital assets, this is how we would expect them to be treated in the following circumstances.

- Selling or trading NFTs or assets within a game would generate a capital gains disposal

- Earning an NFT or asset within a game would be taxable as ordinary income.

Record Keeping

One of the most important messages to come from the sudden worldwide regulation on cryptocurrency is the importance of keeping records of all activity. The Internal Revenue Code and regulations require taxpayers to maintain records that are sufficient to establish the positions taken on tax returns.

Recap makes keeping track of your crypto simple and streamlines the process of tax compliance. You can connect to over 16 exchanges automatically via API and import data by CSV for other accounts. Our platform applies a fiat conversion to every transaction and calculates your tax position for you. Unlike other solutions, our end-to-end encryption gives you complete privacy meaning the only person that can see your transaction history is you.

Reporting Income and Gains to the IRS and Paying the Tax

Capital Gains

You should calculate your capital gains using your chosen accounting method and report the gains on Form 8949 and Form 1040 (Schedule D) of your tax return. Capital losses should be reported on Schedule D of your tax return so that they can be claimed against future gains.

Income

Crypto received as income should be reported as “Other income” on Line 8 of Schedule 1 of your income tax return.

Tax Deadline

The US tax year runs from January 1st to Dec 31st and the deadline for filing your taxes to the IRS is normally April 15. (The deadline for filing 2022 taxes is April 18, 2023). Penalties can be applied for filing and paying late, to avoid a late filing fee you can apply for a 6 month extension by submitting Form 4868 before the deadline.

For more detailed, but totally digestible guidance check out our US Cryptocurrency Tax Guide.

Disclaimer

The content of this blog is for general informational purposes only. It is not legal or tax advice. The information in this guide represents the opinions of experienced crypto tax professionals; however, some of the topics are still subject to debate amongst professionals, and the IRS could ultimately release guidance that conflicts with the information in this guide.Therefore, use this information at your own risk and for information purposes only. Consult a professional regarding your individual tax or legal situation.