Claiming a tax loss on your Celsius assets is not straightforward. As we've detailed in our article “Celsius bankruptcy hands UK crypto investors a tax nightmare”, many issues are at play and there is a lack of clear guidance from HMRC. However, after months of collaboration with our accountant partners, we've released features that enable you to generate a tax write-off aligned with key principles of exchanging contractual rights. Andersen LLP and the CryptoUK working group accountants support this approach.

In this detailed guide we provide some background on the Celsius bankruptcy, asset distribution plan and talk you through our approach for UK Celsius creditors.

This is not tax advice. We strongly recommend using these features in collaboration with a tax professional. You can seamlessly invite your accountant or tax advisor into your Recap portfolio using our agent sharing feature.

Who was Celsius?

Celsius was a global cryptocurrency platform founded in 2017 by Alex Mashinsky, Daniel Leon, and Nuke Goldstein. Users could deposit digital assets like Bitcoin and Ethereum into a Celsius wallet, facilitating lending and borrowing.

What happened to Celsius?

By May 2022, Celsius had lent out $8 billion and had $12billion in assets under management. In Q2 2022, CNBC described Celsius as "one of the largest players in the crypto lending space". In early June there were claims that Celsius had sustained significant losses as a result of the Luna collapse. Around this time, CEO Mashinsky also denied that Celsius was having problems with clients' access to their funds and accused commenters on Twitter, (now X), of spreading FUD about Celsius.

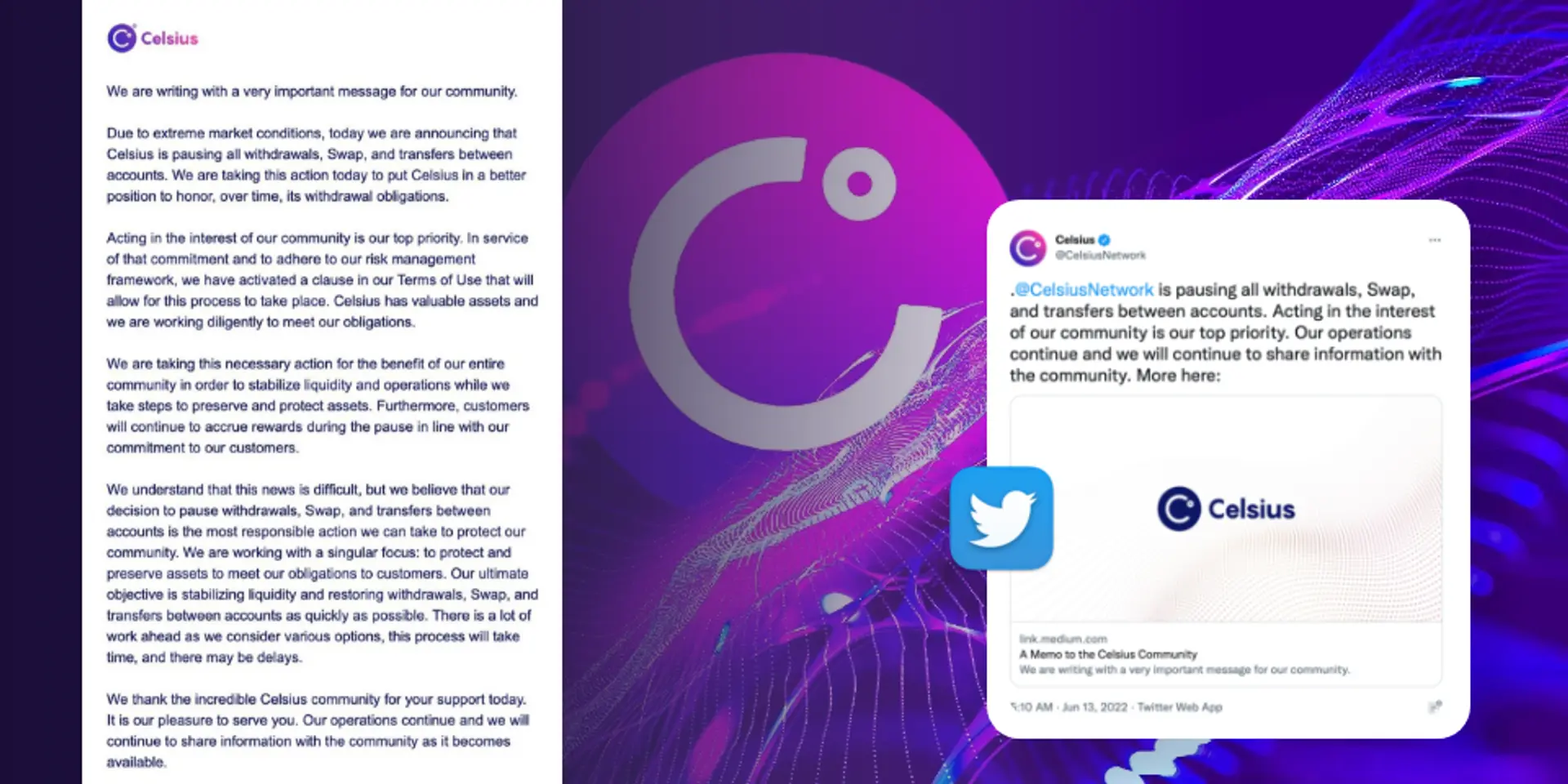

The first big sign that something was wrong was on 13th June 2022, when an email was sent out to Celsius customers. This informed them that all transfers and withdrawals were paused "in order to stabilise liquidity and operations" citing “extreme market conditions”. CEL token fell by a third in price and the announcement also triggered a major downturn across the crypto industry with Bitcoin falling to an 18-month low of $22,725 and Ethereum to $1,176. Celsius CFO, Rod Bolger resigned on 30th June and in early July, Celsius Network laid off a quarter of its workforce.

The Celsius bankruptcy and asset distribution plan

On 13th July 2022, Celsius filed for Chapter 11 bankruptcy in the US, revealing a $1.2 billion shortfall in assets. By 31st January 2024, Celsius announced it was exiting bankruptcy as part of a restructuring plan to distribute assets to creditors. Since February 2024, Bitcoin, Ethereum, and Ionic Digital Shares have been paid to creditors.

Beware of scams

As if losing out once wasn’t enough, scammers are lurking! Celsius claim agent, Stretto, has confirmed that they will only request account or personal information through the Celsius app or email domain @celsius.network, but many Celsians have reported phishing emails, texts, and phone calls relating to recovering Celsius assets, so be vigilant. Notice of withdrawal or solicitation procedures can always be found at https://cases.stretto.com/Celsius.

The UK tax position for Celsius

In the UK, purchases of the same fungible cryptoassets are pooled together for tax purposes in what is known as a s104 pool. When you dispose of some, or all, or a particular cryptoasset, this s104 pool is used to calculate the 'cost' of the asset you are disposing of. When assets become practically worthless, it is possible to submit a 'negligible value claim' through self-assessment, effectively writing off the value of the acquired asset. However, such a claim is only possible where the entire pool becomes worthless. This presents practical difficulties in making a claim where cryptoassets are held across a number of platforms or wallets, and one of these platforms or exchanges goes bankrupt.

For example, if you held Bitcoin on an exchange that went bankrupt, you can't simply write off 1 BTC (worth £50k) for 0. The asset must be nearly worthless, and you can't own that asset on other exchanges or in any other wallets. The claim must dispose of the entire section 104 position - your entire holding of Bitcoin.

Given the fragmented nature of the crypto market, many investors hold assets on multiple exchanges and wallets, making negligible value claims often impractical for fungible assets like Bitcoin.

Understanding negligible value

HMRC state that for tax purposes there is no accepted definition of ‘negligible value’, but generally it applies to assets that have become worth next to nothing while someone has owned them. Assets cannot have been of negligible value when you acquired them, they must have become of negligible value while you have owned them.

Beneficial ownership considerations

An essential factor is beneficial ownership. Version 8 of Celsius’s terms of service, released in April 2022, explicitly stated that Celsius acquired "all right and title" to deposited crypto, including "ownership rights." This suggests that customers might have disposed of beneficial ownership when depositing to Celsius or when the terms of service were updated.

Upon exchanging beneficial ownership of your assets, you receive a ‘contractual right’ to get your asset back. These contractual rights are chargeable like any other capital asset, when Celsius entered Chapter 11 bankruptcy, reclaiming your assets was no longer possible and therefore was likely to cause a genuine disposal of the contractual rights for nil. Or the contractual rights become of negligible value and a claim can be made.

Beneficial ownership

Beneficial ownership is a term used to describe who ultimately controls and therefore enjoys the economic benefits of an asset - even if you had legal title over your assets, control is what matters for tax purposes.

HMRC released guidance for DeFi Lending and Staking in March 2021, highlighting an examination of the contract/terms and conditions required to make a judgement of whether there has been a transfer of beneficial ownership. This guidance subsequently turned into a call for evidence and then a consultation. Recap responded to HMRC’s consultation advocating for a no-gain no-loss treatment for DeFi (which would include centralised exchanges like Celsius).

Potential beneficial ownership exchange triggers

- Every deposit to Celsius.

- Change to Celsius’s terms of service (April 2022).

- Freezing of withdrawals (June 2022).

- Chapter 11 bankruptcy filing (July 2022).

Potential loss relief / write-off dates

- Chapter 11 petition date: 13th July 2022.

- Bankruptcy ruling on version 8 of terms of service: January 2023.

- Effective date of the reorganisation plan: January 2024.

Managing the tax position of bankruptcy distributions

We support the position that you dispose of beneficial ownership for contractual rights, as well as acquiring a parallel right - a right to make a claim against the bankruptcy estate - valued at zero. The ‘right to make a claim against the bankruptcy estate’ is for the eventuality that there was a solvency issue. Bankruptcy distributions exchanged for this right and realise a capital gain upon receipt. For creditors settling a clawback from Celsius, these should be deducted from distributions as they are a direct cost of receiving distributions.

By writing off the contractual rights for zero or via a negligible value claim the subsequent capital loss should offset any prior gains, provided they are in the same tax year.

When the bankruptcy distributions are paid to creditors, these distributions are to be exchanged for the bankruptcy claim right, realising a capital gain on receipt.

For any creditor who has also settled a clawback from Celsius, these should be deducted from the distributions as they are a direct cost of being able to receive your distributions.

Example Earn account

Beneficial ownership transferred: 15/04/2022.

Loss relief claimed: 14/07/2022 on the bankruptcy petition date.

- 01/01/2022 - UK Celsius Customer deposited 1 BTC to the Celsius platform

- 15/04/2022 - UK Celsius Customer lost beneficial ownership of their 1 BTC when Celsius released version 8 of their terms of service.

The Version 8 Terms of Service provided that, with respect to assets deposited into Earn accounts, the customer "grant[s] Celsius . . . all right and title to such Eligible Digital Assets, including ownership rights, and the right, without further notice to you, to hold such Digital Assets in Celsius’ own Virtual Wallet or elsewhere, and to pledge, re-pledge, hypothecate, rehypothecate, sell, lend, or otherwise transfer or use any amount of such Digital Assets, separately or together with other property, with all attendant rights of ownership, and for any period of time, and without retaining in Celsius’ possession and/or control a like amount of Digital Assets or any other monies or assets, and to use or invest such Digital Assets in Celsius’ full discretion. You acknowledge that with respect to Digital Assets used by Celsius pursuant to this paragraph:

(1) You will not be able to exercise rights of ownership; [and]

(2) Celsius may receive compensation in connection with lending or otherwise using Digital Assets in its business to which you have no claim or entitlement; [and]

(3) In the event that Celsius becomes bankrupt, enters liquidation or is otherwise unable to repay its obligations, any Eligible Digital Assets used in the Earn Service … may not be recoverable, and you may not have any legal remedies or rights in connection with Celsius’ obligations to you other than your rights as a creditor of Celsius under any applicable laws. Here we expect a 1 BTC market value disposal and an acquisition of a ‘right to reclaim BTC’, with an acquisition cost of the same value. It is the acquisition of a right which allows the loss claim to be made upon bankruptcy. A parallel bankruptcy claim right has also been acquired a ‘right to make a claim against the bankruptcy estate’ in the eventuality that there was a solvency issue. This second right is considered to have GBP Nil value at the time of receipt, since there was no prospect of bankruptcy proceedings at the time of acquiring this right. - 14/7/22 - Celsius enters chapter 11 bankruptcy in the US.

There was a disposal of the ‘right to reclaim BTC’ from Celsius for Nil proceeds, realising a capital loss in 22/23 (equal to the market value of the tokens at the date beneficial ownership of the tokens was passed to Celsius). - 22/01/2024 - Celsius Customer received a disbursement of ETH and BTC from the bankruptcy estate.

These assets are exchanged for the ‘right to make a claim against the bankruptcy’ and are therefore subject to CGT on the full market value of the proceeds at the time of receipt.

Example Loan account

Beneficial ownership transferred on deposit.

Loss relief claimed 14/07/2022 on the bankruptcy petition date.

- 01/01/2021 - UK Celsius Customer posted 1 BTC to the Celsius platform as a collateralised loan.

Based on the commercial agreement of the loan the UK customer may have immediately disposed of beneficial ownership. Here we expect a 1 BTC market value disposal and an acquisition of a ‘right to reclaim BTC’, with an acquisition cost of the same value. It is the acquisition of a right which allows the loss claim to be made upon bankruptcy. A parallel bankruptcy claim right has also been acquired a ‘right to make a claim against the bankruptcy estate’ in the eventuality that there was a solvency issue. This second right is considered to have GBP Nil value at the time of receipt, since there was no prospect of bankruptcy proceedings at the time of acquiring this right. - 14/7/22 - Celsius enters chapter 11 bankruptcy in the US.

There was a disposal of the ‘right to reclaim BTC’ from Celsius for Nil proceeds, realising a capital loss in 22/23 (equal to the market value of the tokens at the date beneficial ownership of the tokens was passed to Celsius). - 22/01/2024 - Celsius Customer received a disbursement of ETH and BTC from the bankruptcy estate, which are exchanged for the ‘right to make a claim against the bankruptcy’ and are therefore subject to CGT on the full market value of the proceeds at the time of receipt.

How to calculate your Celsius tax write-off with Recap

Using the Celsius bankruptcy feature in Recap

- Sign up to Recap and add your Celsius data.

- Invite your accountant or tax advisor.

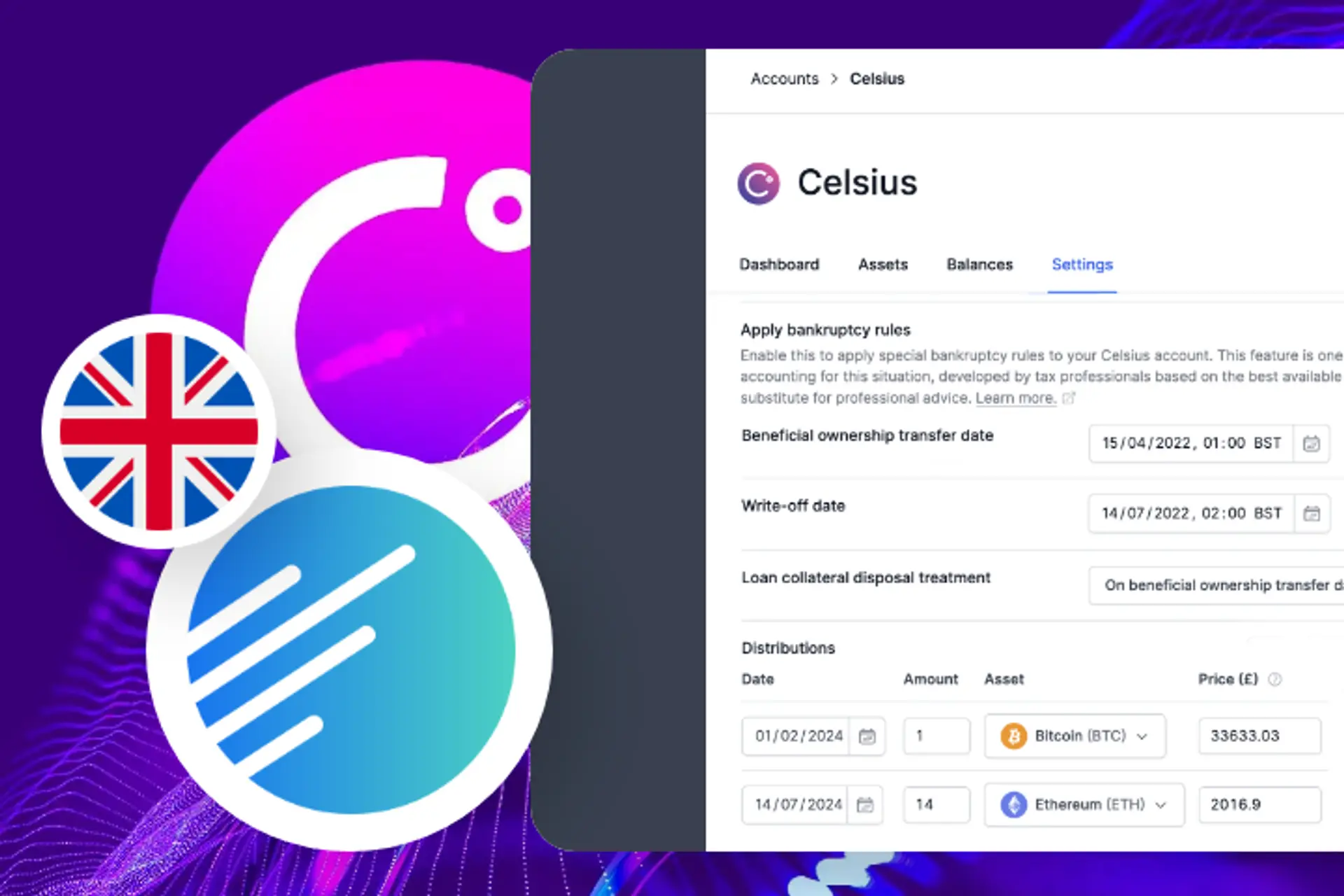

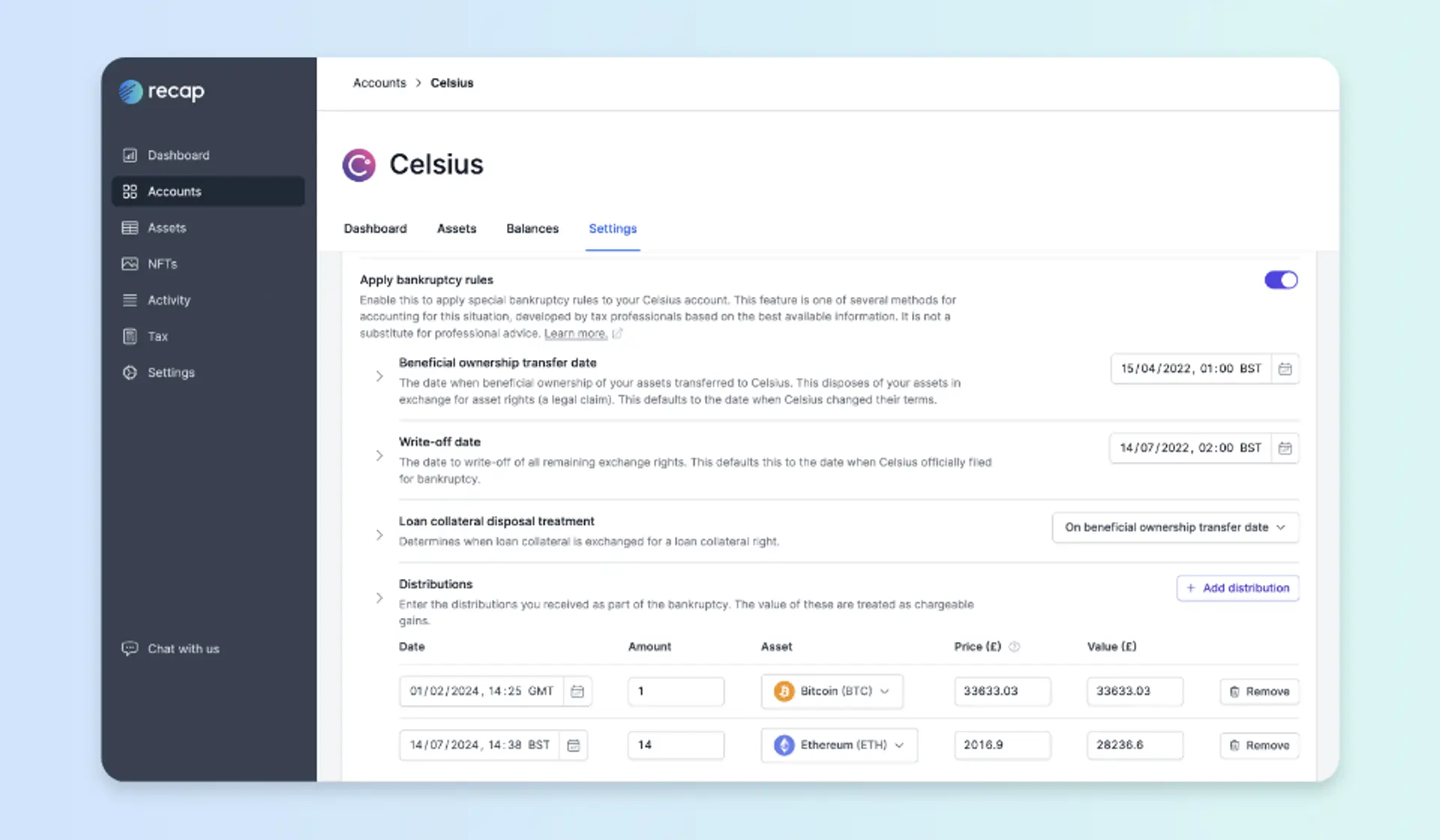

- Toggle on the Celsius bankruptcy feature and collaborate with your tax professional to input the appropriate information for each field.

- Generate your tax write off.

Below we explore the information you need to input with the help of your tax advisor during step 3...

Beneficial ownership transfer date

When do you think Celsius became the beneficial owner of your crypto? This will create a disposal of each of your assets held on the exchange for their equivalent contractual right to reclaim. This could generate huge taxable gains or losses dependent on the acquisition costs.

Write-off date

When you think it became clear Celsius could no longer meet its obligations to return your assets? This will write down the contractual rights to zero, realising a tax loss. Note: it is up to you to assess if this should be claimed through a neg value claim.

Loan collateral disposal treatment

If you took out a loan, was this an immediate disposal of beneficial ownership or was beneficial ownership the same as 1. This will create a disposal of the collateral for a contractual right to reclaim. This could generate huge taxable gains or losses dependent on the acquisition costs.

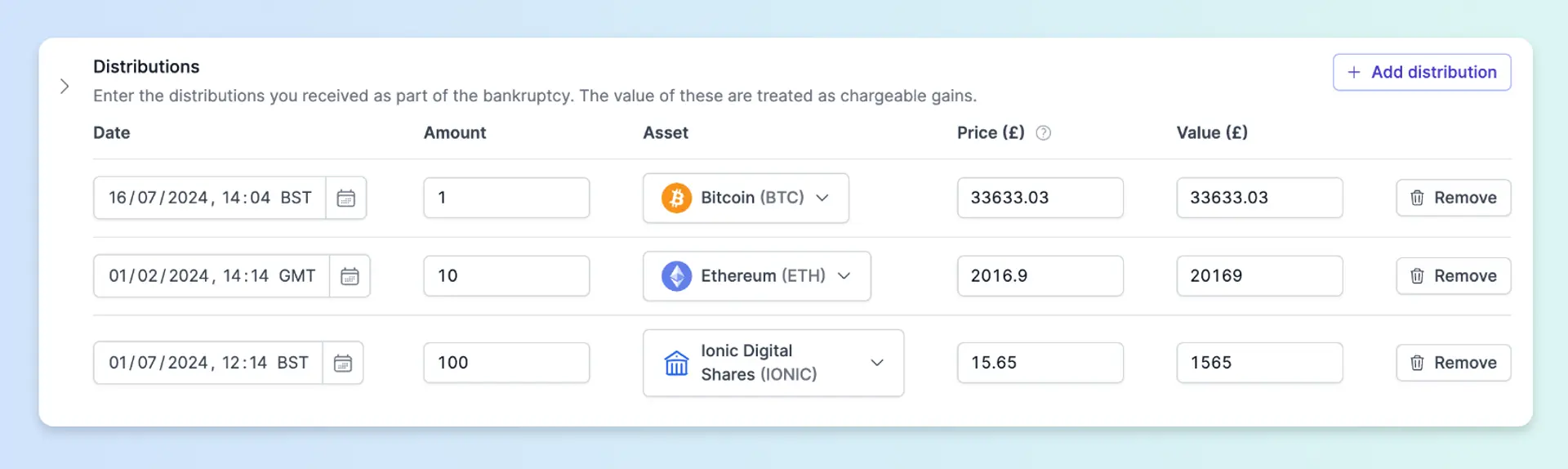

Distributions

Enter in each of your distributions, including the asset, amount, valuation in GBP. We are defaulting the valuations to those agreed in the bankruptcy reorganisation plan effective 31st Jan 2024. Each of these will be treated as having made a disposal of CGT, realising a taxable gain.

Clawbacks

Enter in any clawback settlement. The clawbacks will offset any distribution proceeds.

How to claim your Celsius tax write-off

- After entering the above information, open the activity screen and filter your Celsius account to see your newly created bankruptcy transactions. Assess Recap’s calculations with your tax advisor.

- In the tax screen you’ll be able to see how your tax position is impacted - you may need to refile prior tax years with a loss.

- Ensure your Celsius distributions are accurately represented within the 2023/24 tax year and prepare to file your tax return.

Disclaimer

This guide is intended as a generic informative piece. This is not accounting or tax advice that can be relied upon for any UK individual’s specific circumstances. Please speak to a qualified tax advisor about your specific circumstances before acting upon any of the information in this article.