Filing your Self Assessment tax return just got a bit more crypto-specific. HMRC is introducing a new Self Assessment form for the 2024/25 tax year, with a dedicated section for cryptoassets. If you’re a UK crypto investor, it’s important to understand what’s changing and how to report your gains correctly. Here’s everything you need to know.

This guide is intended as a generic informative piece. This is not accounting or tax advice that can be relied upon for any individual’s specific circumstances. Please speak to a qualified tax advisor about your specific circumstances before acting upon any of the information in this article.

What’s changing on the Self Assessment Tax Return?

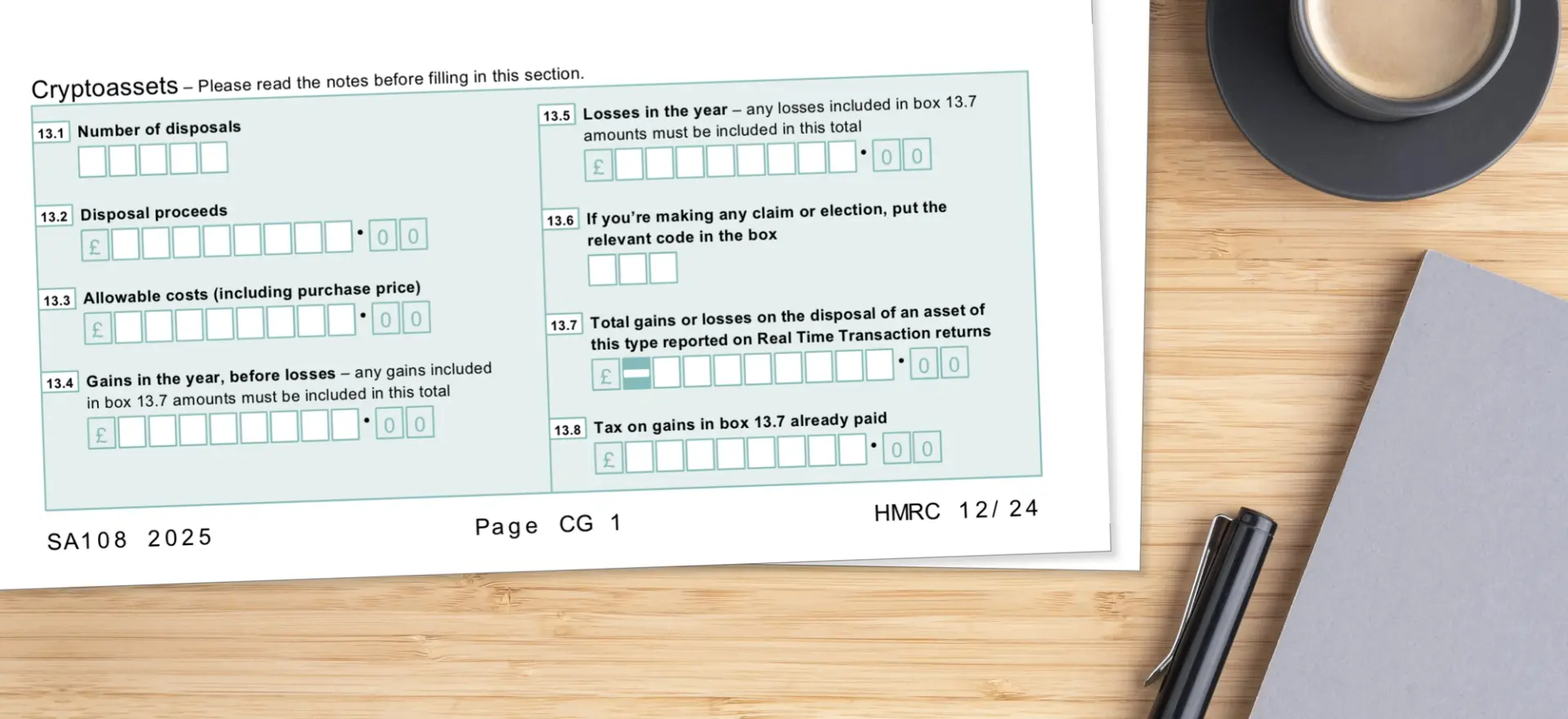

Previously, if you sold, swapped, or spent crypto, you reported any gains in the general Capital Gains section of the Self Assessment form with other gains like stocks and shares. Now, from the 2024/25 tax year onward, there’s a separate section specifically for cryptoasset disposals.

This means:

- More visibility for HMRC into crypto activity

- A clearer structure for reporting crypto gains and losses

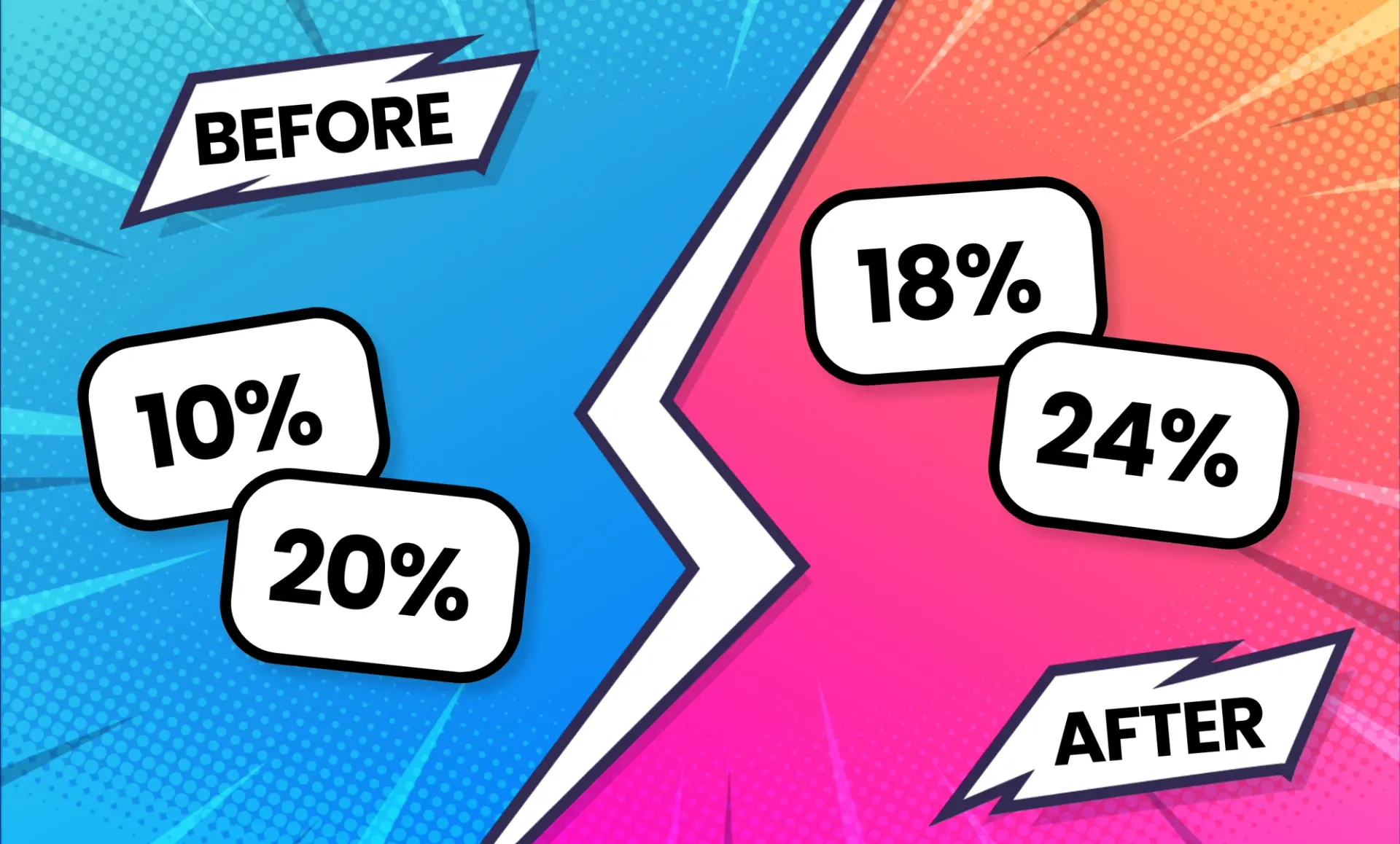

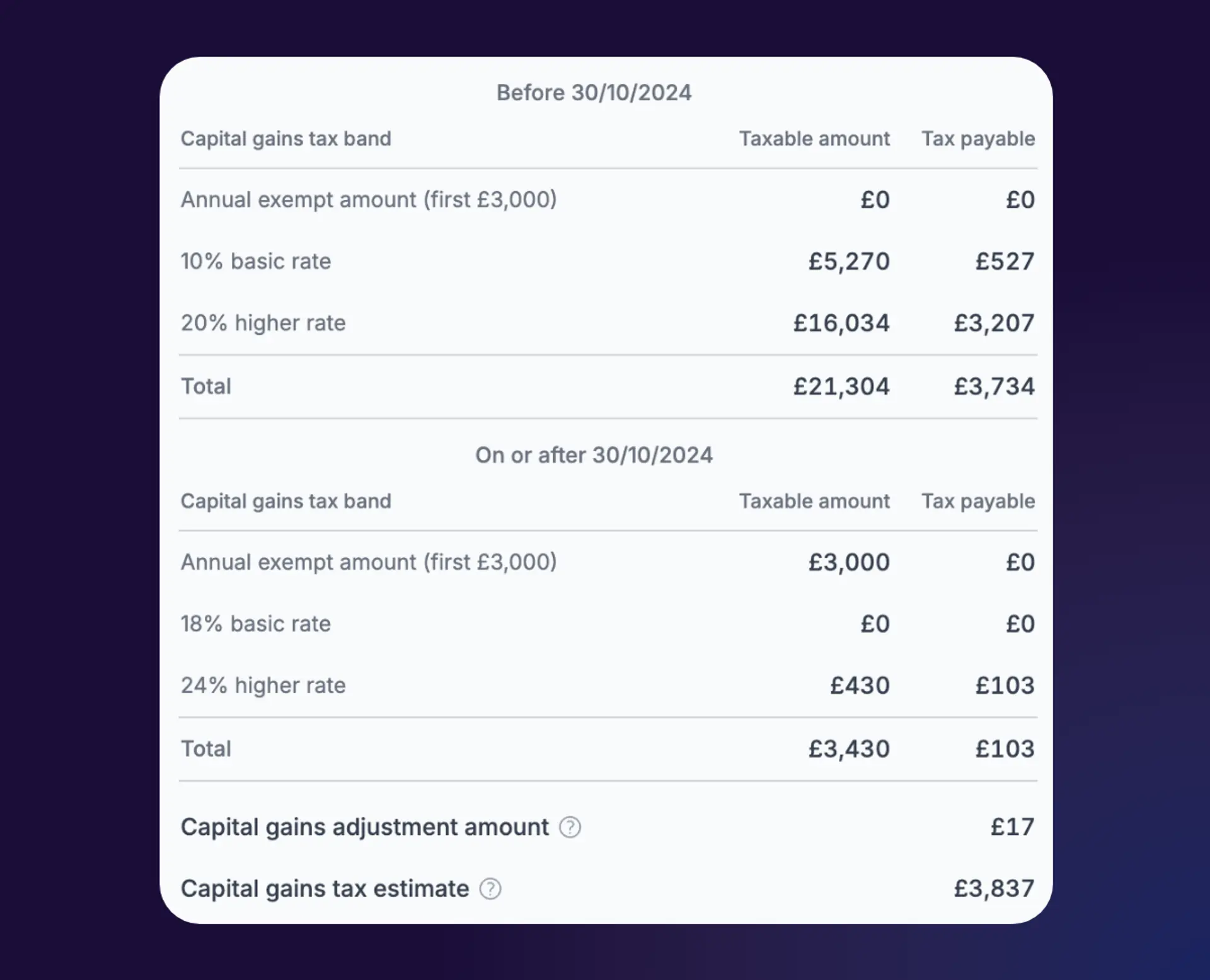

Following the changes to tax rates announced in the Autumn budget, for the 2024/25 tax year, there’s also slightly different reporting if you’ve made gains before and after the split (more on that below).

How to report crypto capital gains in HMRC’s new self assessment form

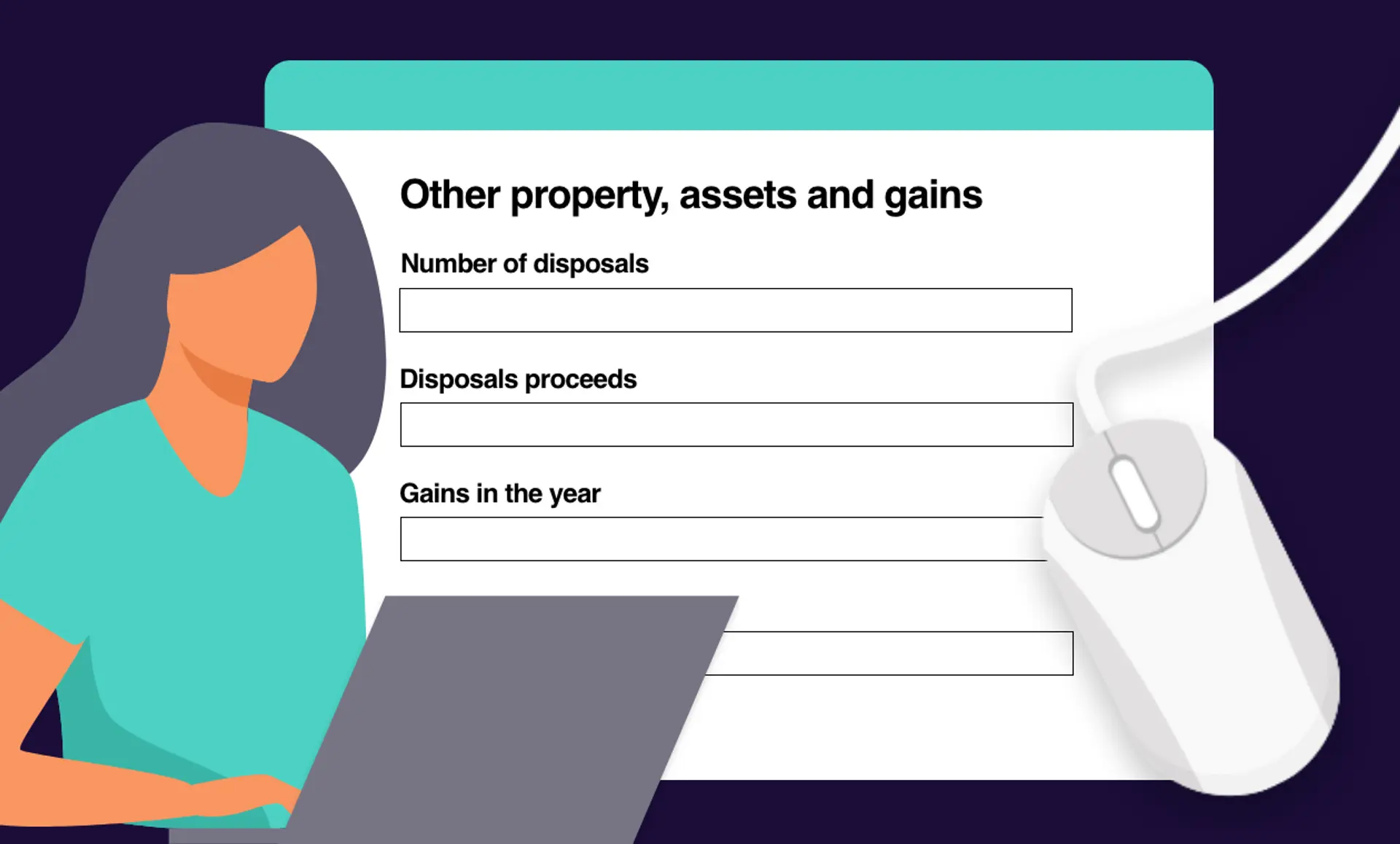

The new format for crypto capital gains on the 2024/25 Self Assessment Tax Return is pictured above. Here’s what HMRC are asking you to declare:

- Total number of disposals

- Disposals proceeds

- Allowable costs

- Gains in the year (before losses)

- Losses in the year

You’ll also need to include calculations and supporting evidence to show that you have followed HMRC’s pooling rules and demonstrate your proceeds and allowable costs. The Recap report which includes disposals and acquisitions does this sufficiently.

There is no change to reporting taxable income from crypto. You can check out our detailed article on how to file your crypto taxes for more information.

What about filing crypto gains for the split tax year?

Additionally, the 2024/25 tax year is a "split" year - HMRC introduced new income tax bands partway through October. This means your capital gains may be taxed at different rates depending on when they were realised.

The new Self Assessment form is expected to include prompts to help guide you through this, but it’s crucial that your records distinguish between disposals before and after the rate change.

Recap makes this easy - your dashboard shows realised gains split across the two periods, with tax estimated accordingly. HMRC's Adjustment Calculator can also help you work out the adjustment for your Self Assessment tax return for disposals of assets on or after 30 October 2024 where the rates changed.

When do I need to file my 2024/25 tax return?

You don’t need to file your return until 31 January 2026, but the window opens from 6 April 2025 – so you can get it done early. That said, waiting until May is advised in case you trigger the bed and breakfast rule.

TL;DR

- New Self Assessment form from 2024/25 includes a dedicated crypto section

- You'll report your crypto gains, losses, and income more explicitly

- Split tax year means some gains may be taxed at different rates

- Recap helps you stay compliant by calculating everything automatically

Can Recap help?

Recap helps you track and calculate your crypto taxes throughout the year, so you’re not scrambling for data when the deadline hits. Log in to Recap and get your data ready early for a stress-free tax season.