Cryptocurrency is on the rise, but unfortunately challenges like lost and stolen crypto are also common. In 2023, cryptocurrency users lost nearly $2 billion to scams, rug pulls and hacks. That figure gets even greater when we include the $40 billion lost to collapses of stablecoin issuer Terraform Labs, crypto lender Celsius and the FTX exchange. Plus, many investors lose their crypto through mishap - losing private keys, damaging or losing cold storage devices and even sending crypto to an incorrect address.

If you’ve experienced lost or stolen crypto, you’re not alone. But can you recover your crypto assets or claim it as a loss? In this article we explore the UK position for lost and stolen crypto including the tax consequences and how to report on your tax return.

Disclaimer

This guide is intended as a generic informative piece. This is not accounting or tax advice that can be relied upon for any UK individual’s specific circumstances. Please speak to a qualified tax advisor about your specific circumstances before acting upon any of the information in this article.

Crypto losses and thefts

Losing cryptocurrency can happen in several ways. For example, you might forget the password to your digital wallet, misplace your hardware wallet, or accidentally transfer crypto to the wrong address. These situations can be frustrating and disheartening, as lost crypto is typically irretrievable.

Stolen cryptocurrency, on the other hand, involves malicious actions by others. Common examples include hacking, where someone gains unauthorised access to your account, phishing attacks that trick you into revealing your login details, and scams where fraudsters deceive you into sending your crypto to them.

The tax implications of lost or stolen cryptocurrency in the UK

How crypto is taxed in the UK

In the UK, cryptocurrency is subject to capital gains and income taxes. When you sell or dispose of cryptocurrency, you may be liable for Capital Gains Tax (CGT) on the profit made. If you receive cryptocurrency as payment for goods or services, or through mining and staking rewards, it's treated as income and subject to Income Tax.

For more information, take a look at our UK crypto tax guide or start calculating your tax position at recap.io.

Tax treatment of lost crypto

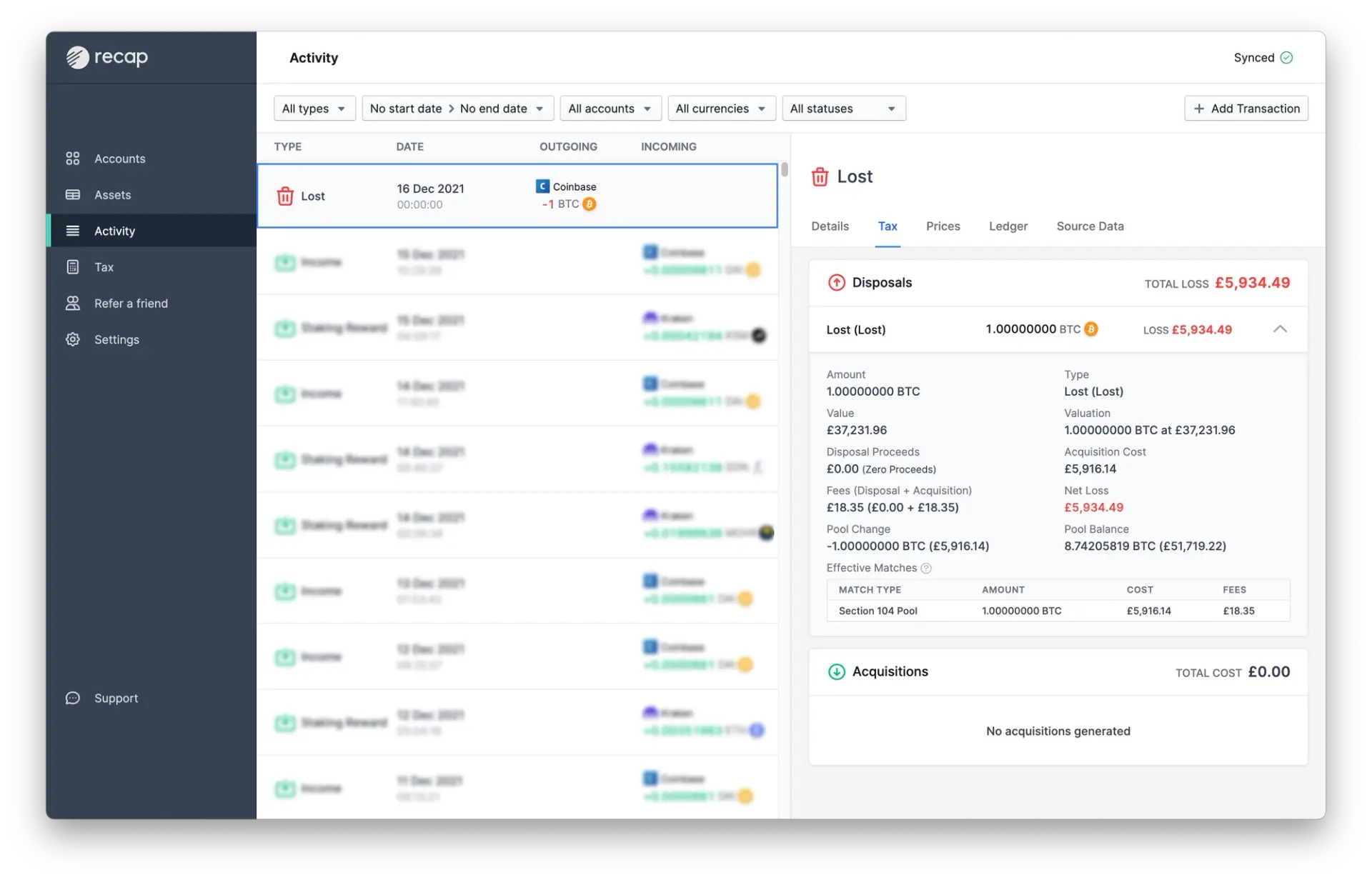

If you lose crypto, for example by losing the private key to your wallet, it doesn’t count as a disposal for capital gains tax purposes. Even though you can’t access your crypto, the private key and the tokens still exist as part of the cryptography and you still own them, they are just not accessible to you anymore.

When can you make a negligible value claim for lost crypto?

HMRC guidance confirms that if you can show there is no prospect of recovering the cryptoassets, you can file a negligible value claim in their Tax Return, to claim a capital loss.

Tax treatment of stolen crypto

Being the victim of crypto theft isn’t considered a disposal for Capital Gains Tax (CGT) purposes by HMRC, as you still technically own the stolen assets and have a right to recover them. Proving crypto theft can be challenging, as it often requires extensive documentation, evidence of the hacking or scam, and cooperation from exchanges and other involved parties.

If you can prove you held the crypto assets at some point but they have since become worthless, you can file a negligible value claim and claim a capital loss on your Tax Return. However, if the tokens were worthless when acquired, a negligible value claim won’t be allowed.

Additionally, if you never received the tokens you paid for, HMRC guidance suggests you may not be able to claim a capital loss.

How to make a negligible value claim for crypto

HMRC guidance allows UK individuals to crystalise capital losses for cryptoasset tokens that they still own if they become worthless or of negligible value while owned. A negligible value claim treats the tokens as being disposed of and immediately re-acquired at an amount stated in the claim.

Don't forget about HMRC pooling rules

As tokens are pooled, the negligible value claim needs to be made in respect of the whole section 104 pool, not the individual tokens. So be aware that a negligible value claim will impact your entire holdings of a token, even if you are holding it in different accounts and wallets.

There isn’t a specific form for making a negligible value claim but it must be made in writing and state:

- The claimant and their unique taxpayer reference

- The asset which is the subject of the claim

- The amount the token should be treated as disposed of (which may be £nil)

- The date that the token should be treated as being disposed of and immediately re-acquired

You’ll also need to provide evidence to HMRC that the asset had value and later became of negligible value while you own it.

When a negligible value claim is approved, you need to notify the capital loss to HMRC - this can be done within the same tax return, letter or document. This loss can be used to reduce capital gains in the same tax year, or be carried forwards to reduce future capital gains.

Can you recover lost crypto?

Losing crypto can happen in several common scenarios, such as forgetting your wallet password, misplacing a hardware wallet, or making mistaken transfers to the wrong address. While these situations can seem dire, there are some tools and techniques that might help you recover your lost funds.

For forgotten passwords, recovery options depend on the wallet provider. Some wallets offer password recovery features, while others might use seed phrases for account recovery. Misplaced hardware wallets can sometimes be traced through purchase records or found using the device's serial number. If you’ve made a mistaken transfer, tracking the transaction on the blockchain can help you identify the recipient. In some cases, contacting the exchange or wallet provider involved can assist in recovering your funds.

Legal and arbitration procedures can also be an option, especially if significant amounts are involved. Engaging with legal professionals who specialise in cryptocurrency can help navigate these processes. Additionally, there are software tools designed to track down lost transactions and potentially recover lost assets.

While not all lost crypto can be recovered, exploring these avenues increases the chances of retrieving your funds so while it may feel like a long shot it could be worth a try.

What are the tax implications for recovered crypto?

If your stolen crypto assets are recovered, they are treated as if you never lost them from a tax perspective. This means you won't need to report a disposal for Capital Gains Tax (CGT) purposes when the theft occurred. Instead, you would report any gains or losses when you eventually sell or dispose of the recovered assets.

If you only recover part of your stolen assets, the situation is more complex. You would need to calculate the cost basis for the portion you recovered and report any gains or losses based on that. The portion that remains unrecovered could potentially be claimed as a capital loss, provided you can demonstrate the loss and meet HMRC’s requirements for negligible value claims. Understanding these implications ensures you handle your taxes correctly, regardless of the outcome of your recovery efforts.

Crypto rug pulls

A crypto rug pull is a type of scam where developers abandon a project and run off with investors' funds, typically after artificially inflating the project's value. If you are involved in a rug pull then you still own the token but it has plummeted in value leaving you with an unrealised loss. To claim the loss and offset capital gains you need to dispose of the token, but there’s not likely to be much demand. In this situation, many investors send the token to a burn wallet, essentially disposing of the token for £nil to realise a loss.

Lost crypto through collapsed and bankrupt crypto exchanges

We've seen the collapse of multiple crypto exchanges including Celsius, Voyager and FTX and Mt Gox back in 2014. Investors using these platforms had transactions halted and accounts were frozen leaving them unable to access their assets. While some assets have been recovered, we’re finding it's very much a game of wait and see for many customers. Below we have summarised what happened and where we’re at with some of these bankruptcies, but unfortunately, tax guidance is limited at this stage. Our suggestion is to hang tight, gather your data and seek out a specialist tax advisor.

The Celsius bankruptcy

Celsius went into bankruptcy in July 2022 and recently started refunding customers. While Celsius investors have now received some of the asset distribution, because this was led by US courts, UK tax guidance is still unclear. The position from HMRC is that you should be able to make a negligible value claim, however as the assets on these exchanges are likely to have a market value greater than zero, negligible value claims are not an option. Another approach is to treat the bankruptcy as a change of beneficial ownership, creating a disposal of your assets for a right to reclaim, and making a negligible value claim against the rights.

To find out our more and explore our suggested tax approach take a look at our blog Celsius bankruptcy hands UK crypto investors a tax nightmare.

FTX

The collapse of FTX left investors wondering whether they will get their funds back. When the company filed for Chapter 11 Bankruptcy in November 2022, they had a massive shortfall and owed the IRS $24 billion in tax. Since then, some assets (such as an 8% stake in AI startup Anthropic) have been liquidated. A reorganisation plan has been proposed and is currently subject to approval by a Delaware court overseeing the bankruptcy case. Whilst still waiting for a resolution, you could start collating your historical transaction data.

Mt. Gox

Mt Gox was a massive Bitcoin exchange based in Japan that launched in 2010. It handled around 70% of all worldwide bitcoin (BTC) trades by 2014, but abruptly stopped operating after the loss of thousands of bitcoins. Mt. Gox suspended trading, closed its website and filed for bankruptcy in February 2014. Although BTC assets have been tracked down to return to claimants, it’s certainly taking a long time to distribute. The plan was officially approved on 16 November 2021, and the latest promised end date is 31st October 2024.

Voyager

Voyager, once hosted 3.5 million users and $5.9 billion in assets, but suffered after Three Arrows Capital (3AC) defaulted on unsecured loans. Voyager froze customer funds on 1st July and filed for bankruptcy days later. Their repayment plan aims to return around 35% of customers' cryptocurrency deposits, depending on your initial deposit and allocated share. Voyager are currently in ongoing litigation with FTX, if this is successful, the expected recovery could increase up to 64%. Payments are expected to be made over the next few years while assets are sold and recoveries obtained. Although you may still be waiting to receive your allocation you could start collating any historical transaction data to help with future reporting.

How Recap can assist in tracking and reporting crypto for tax purposes

Our crypto tax software helps you collate all of your crypto transactions in one place and automatically calculates your crypto tax liability for you. If you've experienced lost or stolen crypto and want to make a negligible value claim and record a capital loss, Recap allows you to create a transaction type “Lost” to help you identify the transaction on your tax report.