Welcome to our guide for individuals on cryptocurrency tax in South Africa - from understanding when and how to pay taxes on your crypto assets to filing your tax return, we’ve got you covered.

As a responsible South African crypto investor it’s crucial to report any taxable gains or income from your crypto assets to the South African Revenue Service (SARS). Our guide explores the intricacies of crypto tax and the differences between capital gains and income tax.

Crypto tax is complex!

Given the complex nature of crypto tax this is an in-depth guide with a lot of information! Navigate through your desired topics quickly using the menu on the left hand side.

Disclaimer

This guide is intended as a generic informative piece. This is not accounting or tax advice that can be relied upon for any UK individual’s specific circumstances. Please speak to a qualified tax advisor about your specific circumstances before acting upon any of the information in this article.

What are crypto assets?

Crypto assets are a digital representation of value that uses technology (cryptography) to secure transactions. People and companies can trade, transfer, and store crypto electronically using it for payments, investments, and more. No banks or governments control crypto assets, they are popular for their growth potential and privacy. There are thousands of crypto assets, the most popular examples are Bitcoin (BTC) and Ethereum (ETH). Non-fungible tokens (NFTs) are another type of digital asset. Unlike fungible assets like BTC and ETH, each NFT is unique with an individual identifier.

SARS crypto classification

SARS officially recognizes cryptocurrencies as 'crypto assets', not as virtual currency, as seen in their ITR12 (Income Tax Return). In January 2021, SARS replaced the word cryptocurrency with crypto asset in line with the proposed adoption of a uniform definition of crypto assets within the South African regulatory framework.

Crypto assets are included under the definition of a ‘financial instrument’ under section 1(1) of the Income Tax Act, No. 58 of 1962 (ITA).

Do you have to pay tax on crypto in South Africa?

Yes, SARS has confirmed that gains or profits arising from crypto transactions may be taxable as capital gains or as income. The onus is on affected taxpayers to declare their crypto assets’ gains or losses in the year of assessment in which they are received or accrued.

This means if you have sold, exchanged, used, or received crypto assets, you may be liable to pay taxes on the concomitant profits. It also means that you should consider all crypto asset transactions made during the year, including crypto-for-crypto and internal platform transactions, not just crypto sold for fiat or withdrawals from an exchange.

What is the deadline to file my crypto taxes in South Africa?

It's vital to understand when each tax year starts and ends as well as when your filing is due, so you know which gains fall into what tax year.

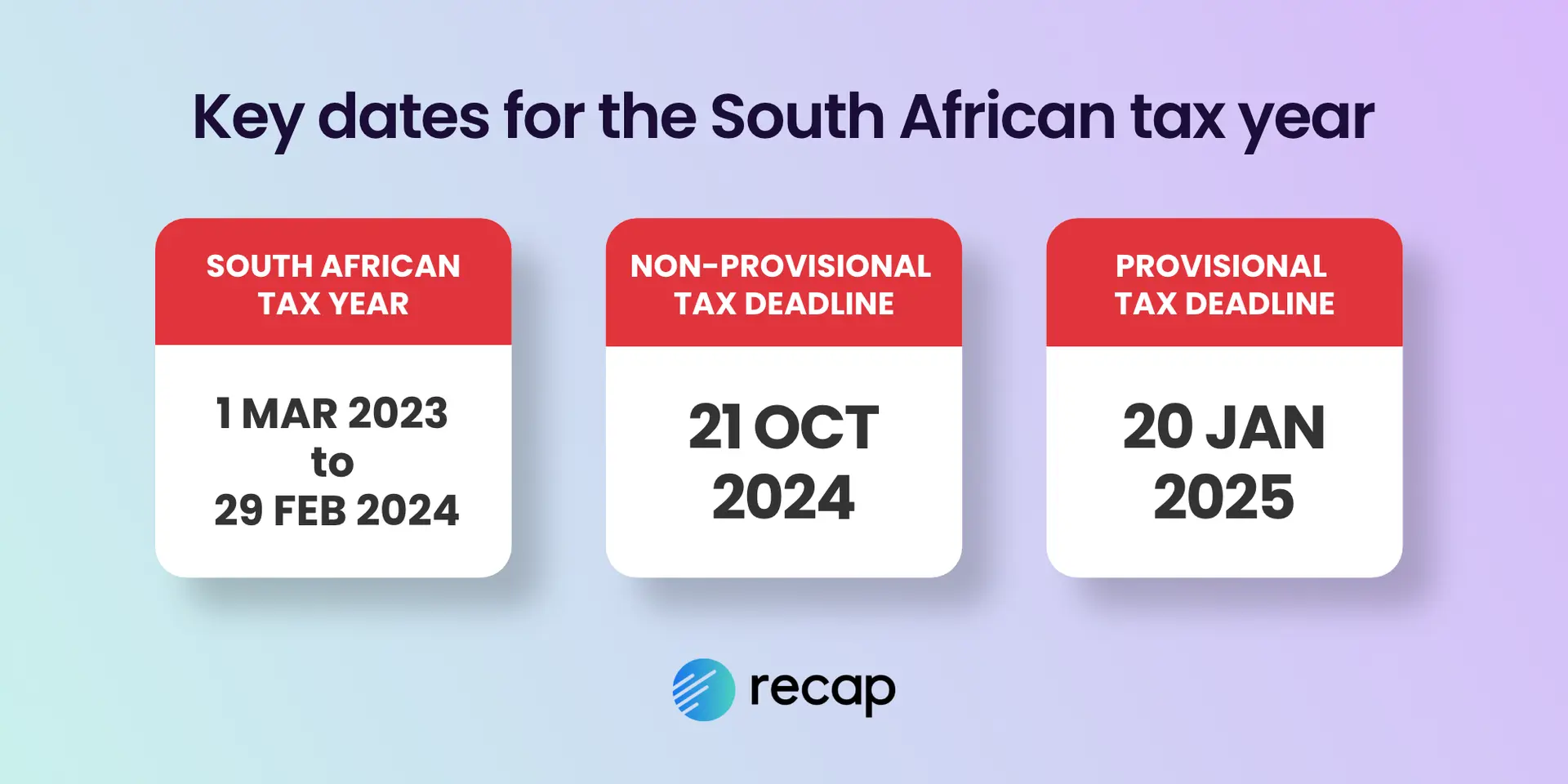

The South African tax year commences on the 1st of March and ends on the last day of February in the following year.

The annual tax return is due during filing season, which falls after the end of the tax year and is announced by SARS each year. There are different deadlines for non-provisional and provisional taxpayers.

2025 tax deadlines for South Africa

Non-provisional taxpayers: 20th October 2025

Provisional taxpayers: 19th January 2026

How is crypto taxed in South Africa?

In South Africa, crypto can be subject to income tax or capital gains tax. Generally earning crypto, for example through mining, is typically subject to income tax. Disposals of crypto may be subject to capital gains or normal income tax, depending on the motive behind the investment. SARS may view persons who hold crypto assets as either traders (taxed on revenue income) or investors (taxed on capital gains). Generally, short-term, active dealings often lead to income tax whereas long-term, passive gains usually face capital gains tax.

We’ve highlighted some of the considerations and differences below, however, it is important to note that this classification must be determined on a case-by-case basis and different classifications may apply to different crypto transactions made during the tax year. Given the complexity, it's wise to seek advice from a crypto-savvy tax professional - they can guide you based on your specific situation.

| Income | Capital Gains | |

|---|---|---|

| Are you actively trading with crypto assets? (A higher frequency of transactions suggests that they are trades rather than investments). | Yes | No |

| Did you purchase the cryptocurrency with intentions of long-term investment? (Buying crypto with the motive of selling it again quickly at a higher price may be considered a trade compared to holding it as a long-term investment). | No | Yes |

| Have you held the crypto long term? (The longer you hold crypto, the more likely it will be considered capital gains). | No | Yes |

Taxed as a trader

Traders are viewed as short-term investors, looking to actively trade in the market for a profit. Crypto asset traders will generally, frequently trade tokens and engage in a lot of swing-trading, or dispose of crypto when opportunities arise to make a profit. Most holders of crypto assets in South Africa are seen as traders not investors, as their trading pattern alludes more to a transactional or ‘trading stock’ nature in respect of their crypto assets. SARS will likely view you as a trader and tax you accordingly, especially if you are heavily active in income-generating protocols.

Tax approach for traders

- Taxed on your entire crypto profits, at the normal tax rates applicable depending on your income bracket.

- Can deduct allowable expenses before calculating and paying your taxes.

Taxed as a investor

On the other hand, crypto asset investors are generally seen as longer-term holders of crypto with the expectation of long-term growth. In certain cases, this may include crypto assets that are held for the purpose of making other profits (for example, crypto assets held to earn staking rewards).

Tax approach for investors

- Annual exclusion of R40,000.

- Taxed at the normal tax rates applicable depending on your income bracket, but only on 40% of any gain after the annual exclusion is applied.

The massive difference in the way gains are taxed when you are perceived as an investor and not a trader makes it more favourable for taxpayers. The distinction between being classed as an investor or trader is dependent on whether you can convince SARS of your intentions. If you want to be recognized as an investor and not a trader, many precautions can be put in place, to add weight to this argument, such as:

- Only holding crypto assets for extended periods of time, for example, 3-5 years.

- Not participating in revenue-generating protocols like yield-farming or staking.

- Not constantly trading crypto-to-crypto or crypto-to-fiat, as this will be viewed as disposals.

How much tax do you pay on crypto in South Africa?

The amount of tax you'll pay depends on the transaction, how it is taxed (revenue or capital gains) and your total annual income. For earnings subject to capital gains tax, you'll pay up to 18% tax on gains over the R50,000 annual exclusion. You'll pay between 18% and 45% on crypto profits subject to income tax.

Capital gains tax on crypto assets

Capital gains are the backbone of long-term crypto asset investments, with tax arising when crypto asset disposals are made. Capital gains tax will, however, only be applicable in limited circumstances, based on the nature of the gains made as well as the intention and conduct of the crypto investor.

However, there is good news, as individuals are granted a R50,000 annual capital gains exclusion and are only required to pay income tax on, effectively, 40% of any capital gains made through crypto assets of a capital nature. On top of this, capital losses also occur when a loss is made on a disposal, which can be offset against subsequent crypto gains.

Most crypto profits are taxed as income

SARS generally views crypto assets being held as a speculative asset that is subject to income tax treatment. Capital gains tax treatment is only applied in exceptional circumstances.

How to calculate capital gain

Capital gain or loss is the difference between the cost basis of your cryptocurrency and the value you received in exchange for your cryptocurrency when sold.

As a basic calculation, CAPITAL GAIN/LOSS = PROCEEDS (the amount of money you received from disposing of the crypto asset) – BASE COST (usually the cost to originally acquire the crypto asset)

If the proceeds exceed the base cost, a capital gain on the crypto assets arises. If the base cost exceeds the proceeds, a capital loss is realized on the crypto assets.

Example

- Ben bought 1 Ethereum for R5,000, with a plan to hold it for five years. R5,000 is now his ‘base cost’.

- After three years, Ben sold his Ethereum for R10,000.

- Ben has made a capital gain of R5,000. (R10,000 - 5,000)

Get help from a tax professional

We recommend you speak to a qualified professional tax advisor to discuss your potential capital gains tax liability. The burden would be on the taxpayer to prove that their crypto assets are capital in nature

What is my cost basis?

As many crypto assets are traded on exchanges without fiat conversions, the value of any gain or loss must be converted into South African Rands to declare on your tax returns. The statutory tax rules for foreign currency conversion must be followed in each case.

Where the transaction does not have a fiat value (for example if Bitcoin is exchanged for Ethereum) an appropriate value for the crypto assets at the time of the transaction must be established, in order to convert the transactional value to South African Rands.

Reasonable care should be taken to arrive at an appropriate valuation for the transaction using a consistent methodology. Details of the valuation methodology must be readily available, should this be a subject of enquiry.

Costs

Thankfully, SARS allows trading costs and any other costs related to the purchase or disposal of crypto assets to increase your base cost, reducing your taxable gain. However, certain restrictions do apply.

SARS guidance states ''Taxpayers are also entitled to claim expenses associated with crypto assets accruals or receipts, provided such expenditure is incurred in the production of the taxpayer’s income and for purposes of trade''.

How much capital gains tax will I pay on my crypto?

South African taxpayers are granted an R50,000 annual capital gains allowance and are required to pay income tax on, effectively, 40% of any capital gains made through crypto assets of a capital nature. On top of this, any capital losses that occur when a loss is made on a disposal, can be offset against subsequent crypto gains.

To calculate the amount of tax owed you’ll need:

- Total capital gain

- The inclusion rate (40%)

- Your tax rate

Capital losses

Capital losses are inversed capital gains, occurring when a loss is made on a disposal. SARS acknowledges crypto capital losses, allowing them to offset capital gains made if the losses were in respect of the disposal of crypto assets held as capital.

Furthermore, capital losses you make investing in crypto assets can be brought forward multiple years, but you cannot “skip” a year when claiming losses – these must be claimed each year until the loss has been fully offset in the subsequent years.

Under section 20A of the ITA, the set off of assessed losses is ring fenced to the income derived from carrying on a specific trade and applies specifically to the acquisition or disposal of crypto assets. This is, however, subject to certain exceptions.

Before implementing any tax strategies, each crypto investor should understand whether they will be classified as investors or traders by SARS with respect to each transaction type and / or each crypto asset concerned. There is no ‘catch-all’ determination for this.

Bed and breakfast rule

Bed and breakfasting is a common tax avoidance scheme for shares, where an investor sells shares that have fallen in value and buys them back the following day. The aim is to create an artificial loss to offset capital gains and lower your tax. However, SARS has rules for this and specifically where the crypto assets are held as capital.

While SARS bed and breakfast guidance covers shares, it also applies to crypto assets, to prevent investors using artificial losses to offset their gains.

If an investor sells crypto assets at a loss and buys them back within a predefined period, the loss cannot be used to save on tax payable.

Income tax on crypto assets

Where your transactions are seen as trades rather than investment, all profits from disposals will be taxed as income. This may include profits from:

- Selling crypto for fiat ZAR

- Crypto to crypto trades

- Gifting crypto

- Spending crypto

Additionally, transactions where you are essentially earning crypto are subject to income tax. Although SARS does not provide concrete guidance, these are possible transaction types where income tax will be applicable:

- Mining

- Staking

- Airdrops

- Employment income

- Liquidity pools

- DeFi interest/ rewards

Earning income from crypto investments

As soon as you earn 'income' through your crypto investments, SARS may view you as a trader, not as an investor. An amount may be considered as ‘income’ regardless of whether it is in fiat or in crypto.

Employment income

If you are paid in crypto assets, the Rand equivalent at the earlier of receipt or accrual is taxable as “other income”, being subject to normal tax, at the applicable marginal tax rate. In these cases, the costs a taxpayer can apply to reduce their tax liability are limited. See our detailed guidance below on employment income or contact a tax professional for advice.

Income tax rates

2025 tax year (1 March 2024 – 28 February 2025) and 2026 tax year (1 March 2025 – 28 February 2026)

| Taxable income (R) | Rates of tax (R) |

|---|---|

| 1 – 237 100 | 18% of taxable income |

| 237 101 – 370 500 | 42 678 + 26% of taxable income above 237 100 |

| 370 501 – 512 800 | 77 362 + 31% of taxable income above 370 500 |

| 512 801 – 673 000 | 121 475 + 36% of taxable income above 512 800 |

| 673 001 – 857 900 | 179 147 + 39% of taxable income above 673 000 |

| 857 901 – 1 817 000 | 251 258 + 41% of taxable income above 857 900 |

| 1 817 001 and above | 644 489 + 45% of taxable income above 1 817 000 |

How to value crypto assets for tax purposes in South Africa

As many crypto assets are traded on exchanges without fiat conversions, the value of any gain or loss must be converted into South African Rands to declare on your tax returns. The statutory tax rules for foreign currency conversion must be followed in each case.

Where the transaction does not have a fiat value (for example if Bitcoin is exchanged for Ethereum) an appropriate value for the crypto assets at the time of the transaction (fair market value) must be established, in order to convert the transactional value to South African Rands.

Reasonable care should be taken to arrive at an appropriate valuation for the transaction using a consistent methodology. Details of the valuation methodology must be readily available, should this be a subject of enquiry.

Do you pay tax when buying crypto?

When buying crypto in South Africa, whether or not you pay tax depends on the method and currency you use to purchase the asset. Here’s a breakdown of the tax implications for different scenarios.

Buying crypto with ZAR

If you purchase crypto assets with fiat currency like ZAR, you won’t be taxed at the time of purchase but it is important to maintain a record of these transactions so you can calculate your capital gain/loss when later disposing of the asset.

Buying crypto with crypto

Buying one crypto asset with another is subject to tax. Many crypto investors overlook this when filing their taxes because they are not “cashing out”. However, you are disposing of one crypto asset and acquiring another. The disposal realizes a gain or loss which is subject to either capital gains tax or income tax. The sterling market value of the crypto asset disposed of is used as the disposal proceeds in the calculation of the gain or loss and is also recognised as the acquisition cost of the newly acquired crypto asset.

Buying crypto with stablecoins

Buying crypto with stablecoins is taxable just like swapping one crypto for another. Stablecoins are designed to maintain a stable value, so investors often get surprised by gains or losses from stablecoin trades, but this is inevitable due to fluctuation of the price of the pegged currency to sterling between acquisition and disposal of the stablecoin.

Is holding crypto taxable?

When you buy crypto assets and hold on to them - known as HODLing, the action is not taxable as you retain the crypto and do not generate any taxable events. Generally long-term holders face capital gains tax when they eventually dispose of their crypto assets and traders who hold short-term, will face income tax. As capital gains are taxed at a lower rate, investing long term has potential to lower your tax bill.

Keep a record

Remember to keep a record to help with calculating the gains or losses for future taxable disposals. It’s also helpful to note when you move crypto between your own wallets and accounts in case this is ever incorrectly tracked as a disposal.

Do you pay tax when selling crypto in South Africa?

Buying crypto assets with fiat currency is not taxable, however disposing of your crypto into fiat is.

Disposing into fiat currency is a direct disposal, where either a gain or loss can be made. This means that a taxable event will occur, regardless of whether or not you have subsequently withdrawn the fiat from the exchange. The important distinction then, as always, is whether the crypto asset was a capital or revenue-generating asset.

Capital gains tax

If the crypto asset was correctly considered to be capital in nature, only 40% of the crypto capital gain can be taxed in South Africa, reducing the effective tax rate down to a maximum of 18% for an individual taxpayer.

If you are looking to save on taxes, it's important that you will need to be seen by SARS as investing in each crypto asset, not trading, which often means potentially holding your crypto assets for extended periods of time.

As SARS has clearly stated, crypto assets are treated as assets and not currencies, meaning a capital gain or revenue profit can occur, if the proceeds exceed the cost of acquisition, of such crypto asset.

By using FIFO, an investor can calculate their cost basis, inclusive of trading expenses, to find their total gain or loss.

Henceforth, two unique scenarios appear:

- Selling your crypto assets for a gain = capital proceeds, or revenue profit

- Selling your crypto assets for a loss = capital loss, or trading loss

Individual investors, and special trusts, do benefit from an annual capital gains exclusion of R50,000. This will apply only if your crypto holdings are capital in nature. This allowance does not apply to profits / gains derived from the trading of crypto assets.

Example

Princess has been actively trading and wants to realize some of her profits. Instead of trading into stablecoins, she wants to trade directly into Rand.

Princess bought a total of R80,000 Bitcoin last year; R40,000 when Bitcoin was valued at R300k and another R40,000 when Bitcoin was valued at R400K.

Always Remember: SARS requires the usage of FIFO to calculate your cost basis and subsequent gains.

After holding for six months, Princess had unrealized gains of R80,000, valuing her Bitcoin at R160k. She decided to sell it all.

Due to FIFO, the remaining gain is calculated in two ways:

- The first R40,000 saw a gain of R50,000

- The second R40,000 saw a gain of R30,000

After her annual allowance is considered, Princess' gain is reduced from R80K to R40K, of which all will be fully taxed as we assume SARS views Princess as a trader.

The gain of R40,000 is taxed at 18%, leaving her R7,200 left to pay in income taxes.

Do you pay tax when spending crypto in South Africa?

More and more opportunities to purchase goods and services with crypto are appearing, with some home builders even offering houses for sale in Bitcoin.

When a service or product is bought with cryptocurrency, the crypto assets are considered to be disposed of, at their current market value.

Cryptocurrency cards, such as Crypto.com's VISA card, use fiat funds and only reward users in cryptocurrency. No disposals occur.

Difficulties occur when considering SARS cost basis method of FIFO (First in First Out), as purchases with crypto assets are often small and frequent.

SARS has stated that FIFO is used for crypto calculations, making purchases with cryptocurrency akin to selling crypto for fiat, or other crypto assets.

Example

Michael recently bought a weekend vacation for himself and his girlfriend. The travel company allowed him to pay through Bitcoin.

Having spare Bitcoin, Michael thought it would be a good idea and went ahead.

Michael bought Bitcoin twice in the last year:

- R10,000 worth in January, when 1 BTC was priced at R400,000

- R25,000 worth in March, when 1 BTC was priced at R500,000.

Remember: SARS uses a First in First out policy for an asset’s cost basis. Here's how:

The weekend trip cost him R15,000 in total. As he bought the trip with crypto, the R15,000 worth of Bitcoin was considered a disposal. (One Bitcoin is currently valued at R600,000)

Using FIFO, Michael must negotiate two cost basis':

- First R10,000 worth was bought when Bitcoins price was R400,000, making a gain of R5,000 (R10,000 * 50%).

- Second R5,000 bought at a Bitcoin price of R500,000, making his gain 20% or R1,000 (R5,000 * 20%)

Michael's total gain was R6 000 and will be taxed at his income rate, assuming that SARS view this a trade and not subject to capital gains tax.

How are crypto to crypto trades taxed in South Africa?

If you decide to trade your crypto, your trade will be liable for tax on any gain made. SARS has not stated whether any crypto assets are free from taxation; therefore, we must accept all crypto-to-crypto trades are taxable as a capital gain including trades into stablecoins. Examples of crypto-to-crypto trades are:

- ETH > USDT

- TRAC > BTC

- DAI > ETH

Gains are made when your proceeds are more than your cost basis. (You can increase your cost basis by including any sales fees or network fees related to the sale of your crypto assets).

Example

As an example, let us look at a crypto-to-crypto trade including Ethereum and a Rand stablecoin.

Although stablecoins are not volatile, we must assume they are considered crypto assets by SARS, therefore fully taxable.

Prince recently bought R60,000 worth of Ethereum with intentions to hold. Quickly realizing Ethereum had doubled in value rapidly, he wanted to sell to secure his gains, believing prices would soon dip.

Moments after, he sold his R120,000 worth of Ethereum into a Rand stablecoin, securing his R60,000 gain.

As Prince quickly bought and sold his Ethereum, will SARS view him as a trader?

Assuming SARS does view Prince as a trader, he will have to pay tax on the full gain.

Prince is in the bottom income tax bracket so he will pay 18% on R60,000,

Therefore, Prince owes R10 800 in income tax (R60 000 * 18%).

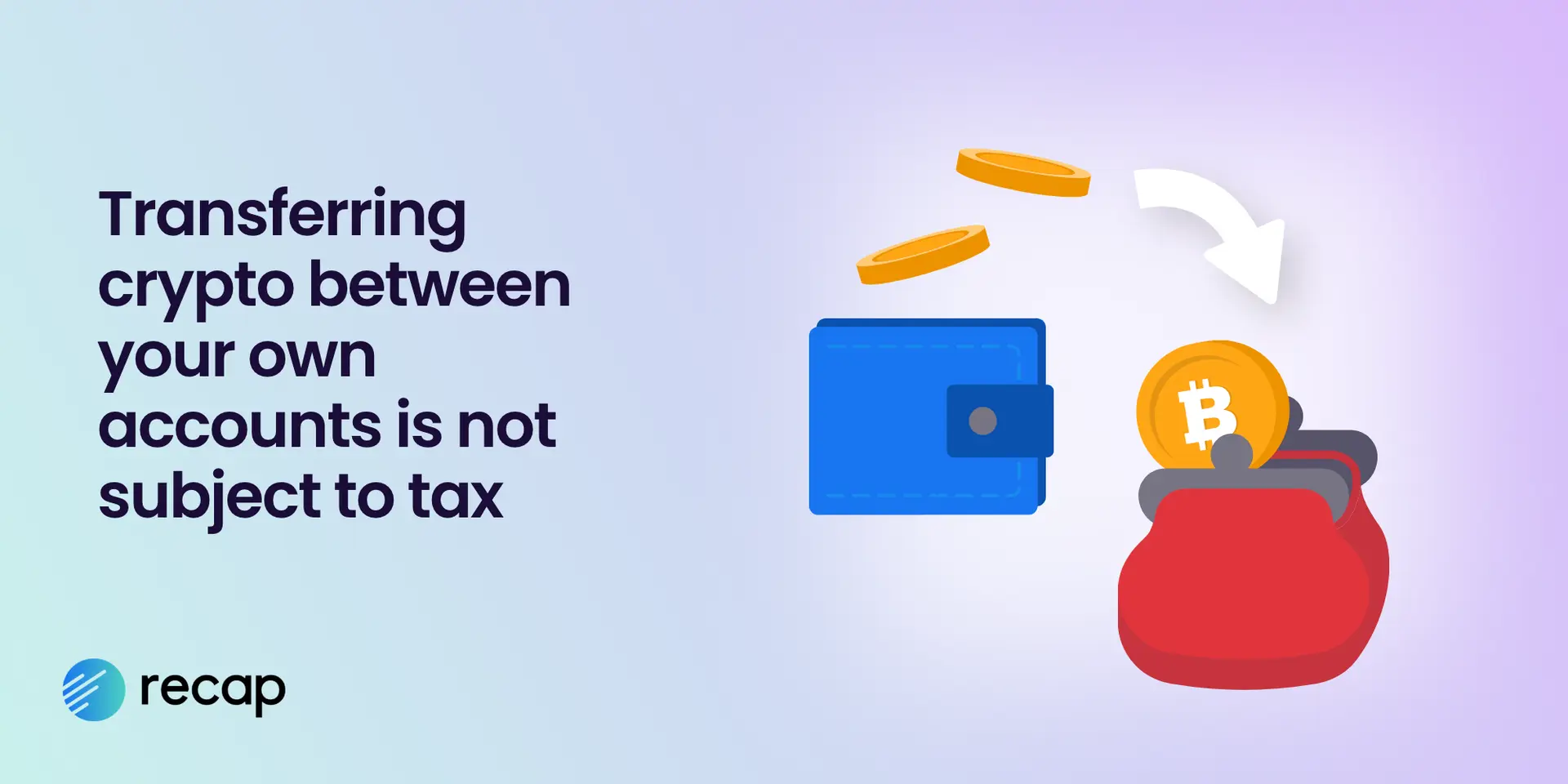

Is transferring crypto between wallets a taxable event?

No, in South Africa, transferring crypto assets between wallets or exchange accounts you own is not subject to tax, because they are not taxable disposals. It is important however, to keep records of all transfers in case they are ever incorrectly assumed to be disposals.

Example

Bandile owns five Bitcoin across multiple wallets and wishes to consolidate all his crypto assets into a singular cold-storage ledger.

Making over ten transactions, Bandile compiled all five Bitcoin into a singular wallet that he then sent to his ledger to keep in cold storage for many years.

Having moved crypto assets that, he already owned into wallets entirely owned by him, Bandile suffers no tax liability from his actions and only will if and when he decides to dispose of any of his Bitcoin.

Gifting crypto

When it comes to gifting crypto assets, the guidelines from the South African Revenue Service (SARS), are not explicitly clear. However, there are several methods to gift crypto assets, including:

- Through centralised exchanges, where assets can be easily tracked and linked to your KYC information.

- Self-custodial wallet gifting, completely anonymously.

- Sharing private keys or ledgers with close friends and family.

Take care when gifting crypto

Remember to always confirm the recipient's wallet address with a small transaction first!

The recipient of the crypto assets will only be taxed once they decide to dispose of the asset.

Recipients cost basis' will be calculated at market value the day they receive their crypto assets.

Like recipients, the disposals value will be the fair market value of the crypto assets as you can see in the example below.

Example

Annie and Mary are both crypto investors, frequently talking to each other about the market.

Mary's birthday is soon, and Annie wants to gift her some TRAC as a present.

Annie sends 100 TRAC over to Mary's wallet on her birthday, worth R7,000 at the time of the gift.

(Consequently, this is now Mary's cost basis and Annie's proceeds)

Having bought her first 100 TRAC for R1,000, Annie must follow SARS First in First Out principles, leaving her with a gain of R6,000 to be taxed.

When Mary decides to sell her TRAC, she will use R7,000 as her cost basis.

Are airdrops taxable in South Africa?

Airdrops are rewards or gifts from cryptocurrency projects for your loyalty, service or simply owning a particular crypto asset. They often come in the form of a new project's token, looking for 'free' publicity and promotion, hoping those who received the airdrop hold onto them for greater rewards in the future. The value of airdropped tokens can vary wildly, so understanding proper tax treatment is essential.

Although there’s no clear guidance from SARS, airdrops can be interpreted to have two distinct tax events:

- Income tax: paid on the market value of the airdropped tokens on the date received.

- Gains when the airdropped tokens are disposed of, taxed as income or capital depending on circumstances.

Example

David has held token X for six months, making him eligible for the recently announced token Y airdrop, worth R16,000.

David receives R16,000 worth of 'value' without disposing of token X, which is likely to be classed by SARS as taxable income.

David is in the lowest income tax bracket, so he will pay 18% tax on the initial airdropped income of R16,000.

16,000 * 18% = R2,880

When he eventually disposes of the asset, he will need to calculate the tax on the gain or loss.

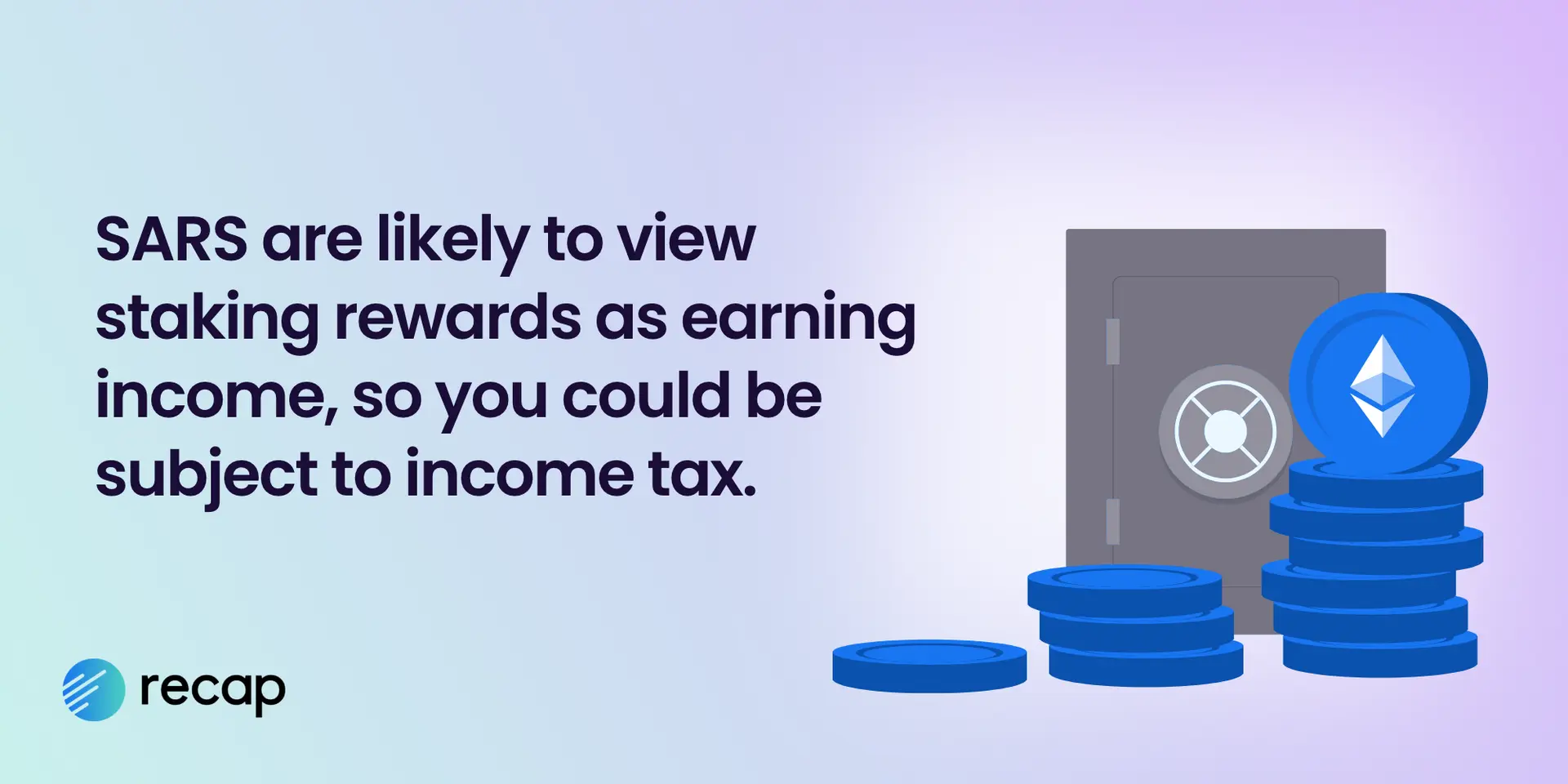

How is crypto staking taxed?

Staking has become the most prominent consensus mechanism used by cryptocurrency projects to validate their blockchain, keeping it permissionless, trustless and irrefutable. Staking, or Proof-of-Stake, requires no physical hardware, unlike Proof-of-Work and is exponentially more environmentally friendly. It uses validators and delegators, where a reward is received proportionately to the number of coins you provided to the stake. If you contributed 1% of the pool's coins, you would receive 1% of the pool's rewards. Rewards come in the form of the network fees, which are passed on to the validator.

Cryptocurrency projects utilising PoS can instantly 'mint' their tokens instead of having to pre-mine them like you would with PoW.

Even by providing liquidity as a delegator, you are providing a service and therefore earning 'income' when you receive your reward. As you are providing a service in return for crypto assets, it is likely SARS views staking rewards as income.

Furthermore, if you eventually dispose of your rewarded cryptocurrency, any appreciation greater than your cost basis is taxable.

Your cost basis when receiving crypto assets is the market value on the date you received them.

Let us look at an example for clarification.

Example

Nia delegated 30,000 CRO (R150,000) on the decentralized Cronos chain, helping validate the network for a guaranteed APR of 12%. She is in the lowest income tax bracket.

Her yearly reward of 3600 CRO was valued at R18,000 (R5 each),

She pays income tax at 18% (18,000 * 18%) = R3,240 payable

How is crypto mining taxed in South Africa?

What is mining? (PoW)

Mining or Proof-of-Work is the original consensus mechanism for blockchains, being used to validate transactions on a blockchain through the use of miners computing power. Miners are then rewarded through the blockchains native token of which transactions they are validating.

For Example: Bitcoin miners receive bitcoin as a reward for each block they validate.

Miners can be seen as providing a service, validating a blockchain, in return for cryptocurrency, which SARS will likely view as income. Unlike other income-generating protocols in the crypto-sphere, miners have business expenses relating to mining which they can use to offset any gains made. Mining profitability is about balancing energy fees with block rewards.

Tax treatment of mining

Although there is little advice from SARS, the tax treatment of mining cryptocurrency falls into two brackets:

- Income tax when receiving the rewarded cryptocurrency

- Tax on any gains made on disposals

Example

Lewis has been mining Bitcoin for the entire tax year, making a total of R50,000 in rewards. He incurred business expensesthrough mining which amounted to R5,000. After five years the Bitcoin has appreciatedto R75,000.

- Firstly, Lewis will likelyowe tax on the full R50,000 he received as his mining reward, seen as a trader by SARS. Lewis owes R8,100 in income tax: (R50,000-R5,000 * 18%)

- Secondly, when Lewis eventually disposes of the crypto asset, he will pay tax on 40% of the entire R25,000 capital gain. He has none of his R40,000 personal allowance left to offset the gain. So, Lewis later owes R1,800 for his capital gain: (R25,000 * 40% * 18%)

Tax on crypto employment income

Getting paid in crypto assets

With increasing inflation and general negative sentiment toward fiat currencies, many employees are losing faith in fiat, choosing to be paid at least partly in cryptocurrency.

Most will choose to be paid in stablecoins, such as USDT, to avoid volatility and exchange their assets into 'blue-chip' cryptocurrencies such as Bitcoin or Ethereum, believing them to be their path to financial freedom.

You may ask - 'If an employee receives half of their wages in cryptocurrency, will SARS know about their earnings?' For this reason, the tax treatment of employment income being paid in crypto assets can begin to get tricky.

How is crypto income from employment taxed?

All income through employment must be taxed. Therefore, we can assume SARS expects you to declare that any crypto received from your employer will be taxed accordingly.

How to file cryptocurrency employment income to SARS

Declare your cryptocurrency earnings through form ITR12, along with your fiat earnings.

Employees have earned their crypto assets by working (mental or physical labour), so they will be taxed based on their income tax bracket.

Example

Junior gets paid R400,000 yearly at his employment and was offered to receive 10% of his employment income in cryptocurrency.

Now receiving R40,000 worth of stablecoins every year, Junior must declare his cryptocurrency 'earnings' or income through form ITR12 when he declares.

He would continue to pay the same income tax rate on his crypto income.

How is lost or stolen crypto taxed in South Africa?

How are crypto assets lost or stolen?

With anonymity preferred and self-custodial wallets the norm, the crypto-sphere, particularly DeFi, provides a landscape littered with opportunists and costly mistakes.

A few of the ways Crypto assets can be lost or stolen include:

- Self-errors: Sending crypto to an incorrect wallet address, or to the wrong type of wallet, can see crypto instantly disappear.

- Rug-pulls: When a developer or project team 'rug' all the liquidity out of their project, leaving investors with nothing.

- Smart-contract exploits: A user exploiting a bug within a smart contract's code to steal funds for themselves.

Furthermore, pushing complete ownership over one's crypto assets through self-custodial wallets is a concept new to most investors. Mistakes made are mistakes owned; within the DeFi sphere, there is no customer service!

Complete anonymity has its costs. Both investors and developers acting anonymously can create a lack of trust within a project.

Tax treatment

Losing crypto assets is never fun; however, not all hope is lost. SARS haven’t given specific guidance for crypto but have declared that involuntary disposals of capital assets relating to destruction or theft can be written off as capital losses, so we can assume that some crypto assets that are lost or stolen can too, providing you can prove that you cannot recover the assets. Where you still have access to crypto assets that are now worthless you can dispose of the crypto to realise a capital loss. Capital losses can be used to offset capital gains within the same tax year.

Example

Daniel was recently storing an entire Bitcoin on his secure ledger wallet; before destroying the hardware wallet when he moved house. Foolishly, Daniel does not have a copy of his backup phrase, and as such, he has now lost those crypto assets forever.

However, provided he can prove ownership over the lost ledger, the value inside and that he can never recover the funds, Daniel could claim a capital loss.

Although it is uncertain whether SARS would allow the loss, they would most likely ask for a few critical pieces of information:

- Proven ownership over the ledger or wallet. Can you link a transaction, which is verified to your identity, back to your ledger wallet?

- Value of crypto assets lost

- Date ledger or wallet was received and date lost

David will not get his crypto back but may still be able to offset up to 1 Bitcoin of future gains if his capital loss is allowed.

DeFi interest and rewards

Within the DeFi ecosystem are different protocols and platforms offering interest gathering services, such as staking and yield-farming through liquidity pools. Users receive rewards for providing liquidity. SARS have not issued guidance on DeFi rewards or interest, however using existing guidance for crypto transactions we can assume that it will be treated as taxable income, relative to your tax bracket.

It is currently unclear whether SARS tracks a crypto assets cost basis at the time earned or at the time claimed.

Example

Julius recently ventured into the world of DeFi earning a reward worth R7 500 from a protocol. It’s likely this will be taxed at Julius' income tax rate band R7,500 * 18% = R1350 payable. When he later disposes of the crypto asset he will also be taxed as income or capital gains.

How is tax applied for South African taxpayers participating in liquidity pools?

Liquidity pools, predominantly used in DeFi (Decentralized Finance), are a pool or pair of cryptocurrencies locked in a smart contract to allow users to lend or borrow crypto assets to other users.

With no guidance from SARS, we must base our tax approach on previous rules and assume that interest received from liquidity pools is seen as crypto income, similar to interest from a bank. As liquidity pools are simply decentralized lending platforms, the treatment should be the same as DeFi interest or rewards.

Example

Deciding to take her Bitcoin off a centralised exchange, Nataly sent it to a DeFi liquidity pool hoping to earn some rewards from her stake.

- She locked in a 3-month stake at a value of R95,000 for 13% APR guaranteed

- Her total reward from providing liquidity was R3,088 (R95,000 * 13% / 4)

- Nataly will be fully taxed on her R3,088 income at R555 (R3,088 * 18%).

How are NFTs taxed in South Africa?

SARS has published minimal advice regarding the taxation of Non-Fungible Tokens (NFTs). However, it’s likely that NFTs follow the same rules as other crypto assets and therefore the tax treatment depends on the transaction and the motive behind the investment as we explored earlier in the guide.

- Where capital gains applies, we can assume disposals of NFTs are taxed on gains that exceed their 'base cost'.

- Where revenue income applies, it is assumed the profits from disposals would be subject to income tax.

Record keeping for crypto assets

An important requirement in South African tax law is that taxpayers must retain their records for at least 5 years after filing their return.

The type of records to be kept are books of account and documents that demonstrate the liability or non-liability of the taxpayer. This may include CSV files or downloads of the wallet activity from each crypto asset exchange wallet, as well as calculations prepared for the taxpayer such as a Recap report.

Crypto asset record keeping

Records must include:

• the type of crypto asset

• date of the transaction

• if they were bought or sold

• number of units involved

• value of the transaction in South African rands (as at the date of the transaction)

• cumulative total of the investment units held and gain or loss for the year

• bank statements and wallet addresses, in case these are needed for a verification or audit.

Crypto assets are obtained, administered, exchanged, used and linked to fiat currency electronically or digitally. It is reasonable to request electronic records with full details of transactions and any supporting valuation records for the acquisition and disposal tax points.

Exporting a copy of your data from the exchanges and wallets, on a regular basis, is good practice.

SARS provides further guidance on record-keeping requirements here.

What if I have missing crypto records?

There could be many reasons for missing data – not taking records before leaving an exchange, historical data being unavailable, exchanges closing, etc. In South Africa, the responsibility for record-keeping lies with the user, so you should prioritise this moving forward.

Unfortunately, sometimes missing data is simply untraceable and can only be identified as such. If this is the case, we recommend that you consult with a professional tax advisor to address this with SARS upon inquiry.

SARS verification and audit

After filing your return, you may be selected for verification or audit. A verification is where SARS requests relevant documents and information to compare against your disclosures. This often happens in cases where you declare amounts that SARS does not already have from third parties (such as employers and financial institutions).

If you are selected for verification, you will be notified by SARS through an official letter. This letter will indicate the due date / time frames within which you must submit the documents and information. The time frame provided is generally 21 business days (not counting weekends and public holidays).

After submitting the requested material, if SARS still requires more information, they will notify you of this and the specific information needed.

An audit, however, is an investigation into your compliance. This is a much more aggressive and intrusive SARS process and should always be treated sensitively. SARS will start by notifying you that your return is subject to audit. If you are notified by SARS of an impending audit, be sure to urgently contact a professional tax advisor to assist.

Accounting for missing data with Recap

Finding missing records is problematic and there are limited ways of finding your transaction history. A couple of suggestions:

- Check bank statements for any fiat deposits or withdrawals you may have made into or out of the account

- Check through any historical data that you do have to see if you can track any movement of assets across accounts/exchanges

- Get in touch with exchanges you no longer use to request data they may still have.

You can create a custom account within the Recap app and try to collate the missing transactions using the ideas above and from memory. You may get warnings for missing acquisitions which you would need to add.

Filing your tax return in South Africa

When you have calculated your crypto taxes and are ready to file, the easiest and most common way to file your tax return is online, through SARS' e-Filing.

All returns are filed through the ITR12 form, where all income and allowable expenses are documented.

Other filing options are available, both virtually and physically:

- Using the SARS MobiApp.

- Filing electronically at a SARS branch to get direct assistance. SARS requires that a booking is made before showing up.

- Completing a tax return via the e-Filing platform.

The tax year runs between March 1st and Feb 28th/29th every year.

How to register for SARS e-Filing

The easiest way to complete your personal tax return is through e-Filing, which you must register for here with valid identification (South African ID or foreign passport). If you have not registered as a taxpayer before, your e-Filing registration will automatically allocate you with a tax reference number.

Unsure about registration?

If you are unsure whether you are registered as a tax-payer, use the SARS query function.

How to file your tax return

Begin by logging into SARS e-Filing with your registered details. After logging in, proceed to ‘Returns Issued’ and then ‘Personal Income Tax (ITR12)’ and go to the tax year you wish to file for – if need be, select the year in the drop-down menu and click ‘Request Return’. Click the 'My tax return ITR12' link to begin filing.

Customise your tax return by answering questions required by SARS. Check that you have all supporting documents and information, input the relevant fields (remember to distinguish between capital and revenue amounts) and submit the return.

SARS have created a simple yet valuable video guide on submitting a ITR12 return here.

How to calculate your crypto taxes with Recap

Recap makes filling simple. Our privacy focused software calculates crypto tax liability for South African crypto investors, using the SARS requested FIFO cost basis method.

1. Connect your wallets and exchanges

Add all of your transaction data by connecting your crypto accounts. We have a range of integrations - single click sign-in, API keys, wallet address and CSV import.

2. Check your data

It’s important to supply all historical transactions so Recap can calculate your taxes correctly. You’ll need to check your synced data is accurate and add or edit anything that is incorrect or missing. Our software applies automated asset valuations and the applicable tax treatments to your transactions and uses FIFO to calculate your taxes.

3. File your return

When you are happy your data is correct, subscribe to download your crypto tax reports, ready to file with SARS.

Contact our team for help

If you need a hand, contact our team through in-app chat. We can help you with data reconciliation and introduce you to our partner for South Africa, Crypto Tax Consulting who can provide advice on a personal level.