This blog is a quick read for those trying to understand the basics of US crypto tax. Recap does not provide advice and we always recommend that you speak to a CPA about your individual cryptocurrency tax circumstance.

Do I need to pay crypto tax and how much?

Your asking the question, so chances are, yes you do. Basically, if you have sold, converted, paid, donated or earned using crypto you may owe tax. Even if you have just bought and are a Hodlr it’s worth checking as you may need to declare this on your tax return. The amount of tax you need to pay depends on how long you have held the crypto – short term (less than a year) or long term (one year plus) and your ordinary income tax rate.

Whose responsibility is crypto tax?

Exchanges are having to be more transparent because of growing worldwide pressure to regulate cryptocurrency. However, ultimately the IRS holds you responsible for reporting your own crypto income and transactions and you could face penalties or interest on tax owed if caught out.

So, how should crypto be treated for tax?

The IRS uses the term “virtual currency” to describe cryptocurrency and generally treats it in the same way as property for tax purposes. Therefore anytime that you dispose of a cryptocurrency you are subject to capital gains or losses.

Cryptocurrency and Capital Gains Tax

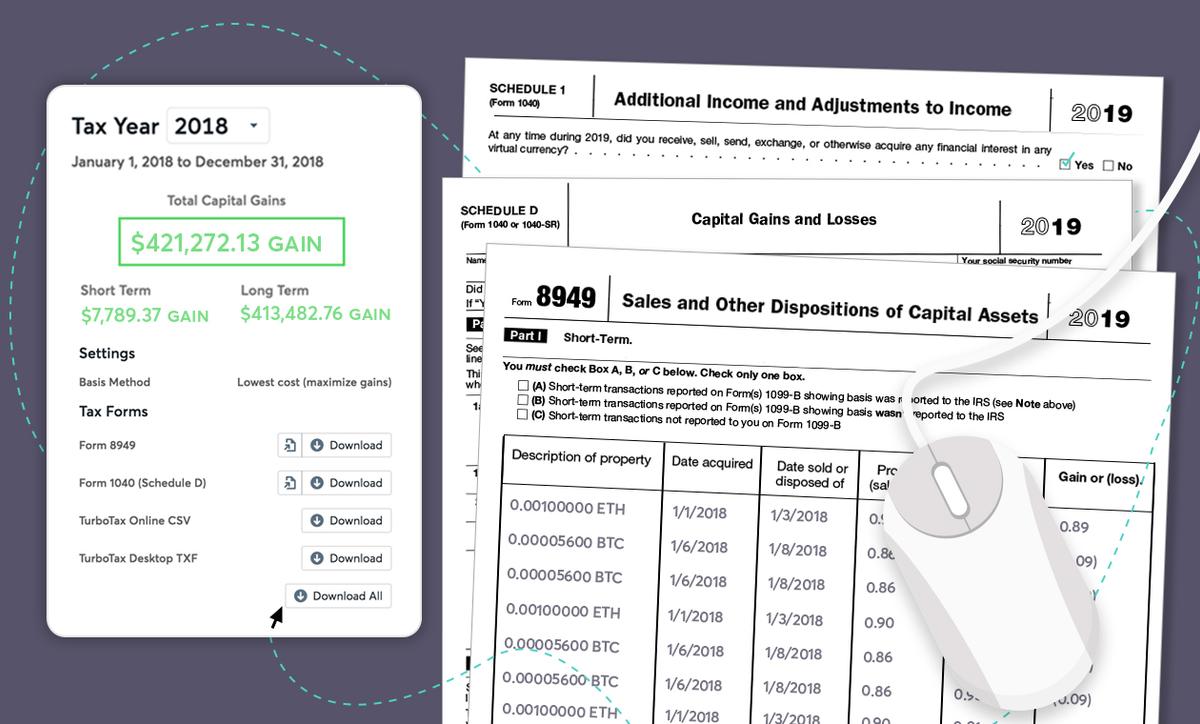

Capital gains tax should be reported on Form 8949 and Form 1040 Schedule D of the tax return. Your gain or loss is the difference between your selling price and purchase price (aka cost basis). As you would expect, if there is an increase in value at the time of disposal then it is treated as a gain and if there is a decrease then you have a loss. Any losses can be deducted against capital gains.

It sounds a fairly straight forward process but gets complicated for crypto traders who have lots of transactions because:

- Gain/loss has to be calculated for every individual disposal throughout the tax year – a tedious and time demanding process that requires good record keeping

- Determining the correct cost basis is difficult – if you have bought the same cryptocurrency at different times and prices how should you determine which one you are actually selling?

Cost Basis Methods

There are different approaches to cost basis; the most well known are FIFO, LIFO, SpecID, HIFO and LOFO. You should choose one method and use it consistently to calculate your capital gains.

FIFO – First In First Out is the most common method and is preferred by the IRS. It assumes that the first assets you purchased are the ones you are disposing of and therefore you use the price paid for the oldest assets in your portfolio to calculate your gain/loss.

Find out more about Capital Gains Tax and Cost Basis Methods in our US Crypto Tax Guide.

Income Tax and Cryptocurrency

Cryptocurrency that you have not “bought” may be classed as income, which should be reported as “other income” on Form 1040 Schedule 1. Hard forks, airdrops and interest generated from lending crypto are all examples of income from cryptocurrency and should be reported in this way.

Mining, staking and masternodes activity also generate cryptocurrency income but you must first determine your level of activity. If you classify as a hobbyist miner, you can report income on Form 1040 Schedule 1, business miners should use Schedule C Profit or Loss from Business instead.

Deductibles

Cryptocurrency Trading Fees

Incidental costs of purchase and disposal can be deducted from capital gains. There isn’t much guidance from the IRS yet but we would assume related costs such as Trading Fees are acceptable but transfer fees are not.

Expenses

Cryptocurrency miners can deduct their expenses however the amount allowed and what is acceptable varies depending on if they are classed as a hobbyist or business miner.

Donating to charity

If you donate to a qualified charity then you can claim a charitable deduction of the fair market value at the time of donation. The amount deducted depends on how long you held the crypto for.

Offset your losses

You can deduct any capital losses against capital gains, including non-crypto gains. If your losses are higher than your gains then you can also use any remaining losses against your income, up to $3,000 per year. Losses also carry over to the following year.

Tax Loss Harvesting

If you have purchased cryptocurrency that has since nose-dived in value then you can strategically sell it to realise your losses and then buy back straight away to offset your gains. Doesn't sound legitimate and there is a rule called the Wash Sale Rule to prevent this for Stocks and Shares but as the IRS classes Cryptocurrency as property this does not apply. Technically it is legal but we would highly recommend speaking to a tax professional before acting.

Reporting Cryptocurrency Income and Capital Gains and the IRS Tax Deadline

You should report your cryptocurrency tax on Form 8949 and Form 1040 Schedule D for capital gains and Form 1040 Schedule 1 for income. The IRS deadline for filing 2023 taxes is the April 15, 2024. Should you miss the deadline there are two penalties - one for filing late and one for paying late. Penalties can escalate fast as interest accrues, so it is worth getting on top of things as soon as possible.

Keeping Records of Activity

One of the most important messages to come from the sudden worldwide regulation on cryptocurrency is the importance of keeping records of all activity. You should be responsible for your own data and be proactive in exporting a copy from exchanges and wallets that you use on a regular basis.

Additionally keeping this data even after submitting tax returns for the relevant year is vital to aid any IRS compliance checks or to find cost basis’ for future tax returns.

How Recap can help

Recap securely manages cryptocurrency data and calculates your gain/loss based on your chosen cost basis method. You can download a ready to file Form 8949 and file yourself or share your account with your CPA and they will be able to complete the Tax Return and advise on your tax position, based on your specific circumstances.

Recap is a tool that you can use year round to keep track of your whole portfolio - as cryptocurrency regulation increases this will help you to optimize your taxes and crypto investments.