Welcome to our comprehensive guide for individuals on cryptocurrency tax in the UK, providing you with all the essential information based on HMRC’s crypto tax guidance. From understanding when and how to pay taxes on your crypto assets to filing your tax return, we’ve got you covered.

As a responsible UK crypto investor it’s crucial to report any taxable gains or income from your crypto assets to HMRC. Our guide explores the intricacies of crypto tax, breaking down how different transactions are taxed and the differences between capital gains and income tax.

Given the complex nature of crypto tax this is an in depth guide with a lot of information! Navigate through your desired topics quickly using the menu on the left hand side.

What are cryptoassets?

Cryptoassets are a type of digital asset defined by HMRC as “cryptographically secured digital representations of value or contractual rights” that have the potential to be transferred, stored and traded electronically.

There are thousands of types of cryptocurrencies, the most popular examples are Bitcoin (BTC) and Ethereum (ETH). Non-fungible tokens (NFTs) are another type of digital asset. Whereas fungible assets like BTC, ETH and even the fiat Pound (£) are worth the same amount, every NFT is unique, with its own characteristics and digital identifier.

While crypto assets share certain attributes of both fiat currency and stocks and shares, such as the ability to be used as a form of payment and potential to fluctuate in value, it is important to note that HMRC do not consider crypto assets to be currency or money. HMRC also does not class the buying or selling of crypto assets as gambling, meaning that profits derived from interacting with crypto are taxable.

Do you have to pay tax on crypto in the UK?

Yes, you have to pay tax on crypto in the UK. The type and amount of tax you will pay depends on the types of crypto activity resulting in the profits, capital gains or income from crypto.

Most individuals are buying and selling crypto assets as an investment activity which is taxed under the capital gains tax (CGT) regime. As an investor, you pay CGT when your crypto capital gains exceed the CGT exemption (also known as the capital gains allowance) for the tax year.

You also pay income tax or CGT on any income or capital rewards you generate from crypto activities. Income tax is applicable when income rewards are earned through activities like mining and staking and should be reported on the tax return as miscellaneous income.

Tax compliance is law and declaring your crypto taxes is your legal responsibility, however there are strategies to legally reduce your crypto taxes. To find out how to optimise your crypto tax liability and pay less tax see our article "Can you avoid paying crypto taxes in the UK?"

How much tax do you pay on crypto?

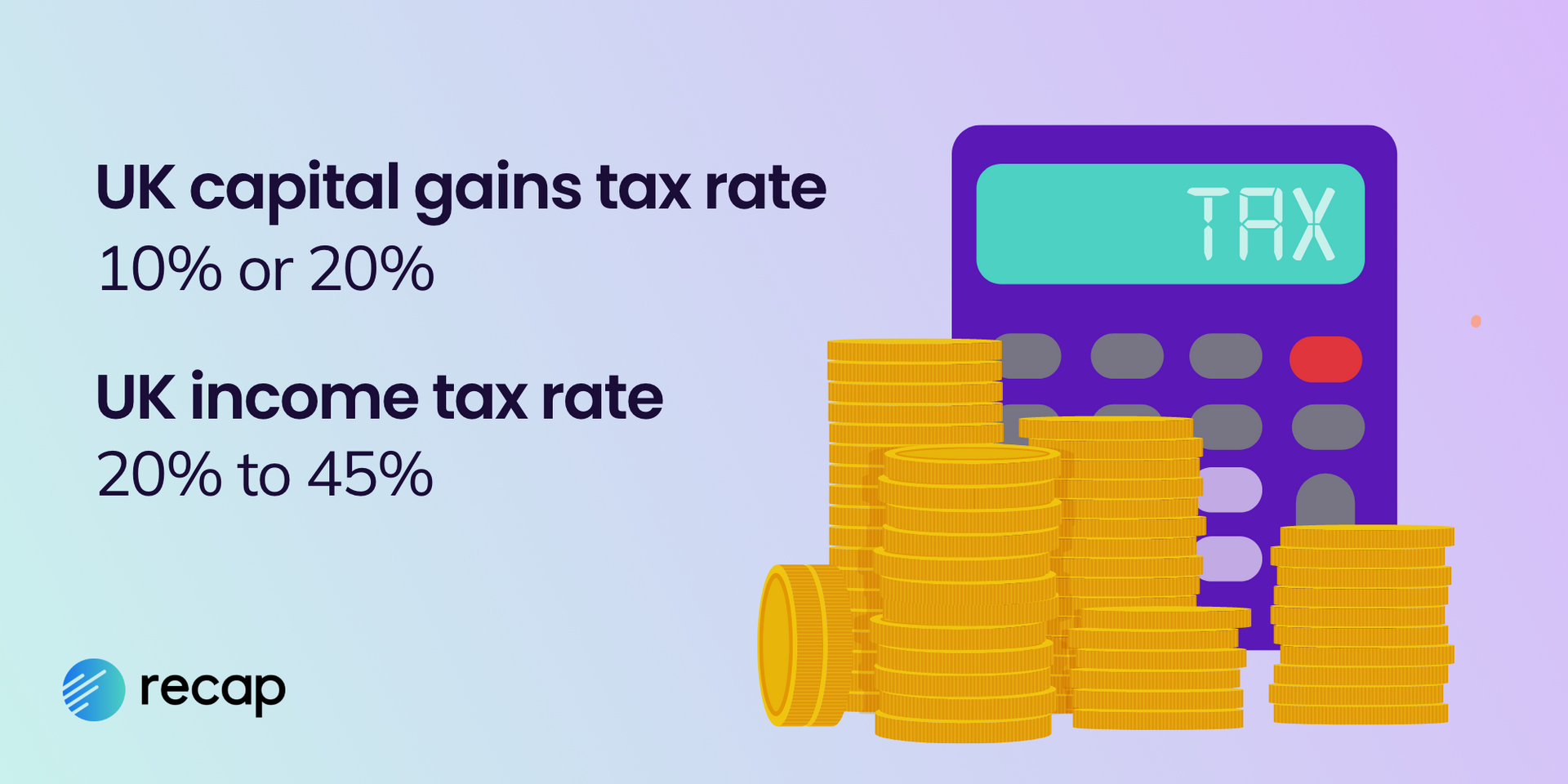

In the UK you’ll pay tax on capital gains that exceed the annual capital gains allowance, at a rate of 10% or 20%, depending on your total income in the tax year.

For crypto income, the rate of tax you pay will be between 20% to 45% depending on your other sources of income and your overall income level in the year.

The specific amount of tax you will pay on your crypto transactions is influenced by several factors, including the transaction type and tax applied. We’ll look into all of these in detail in the below tax guide.

How is crypto taxed in the UK?

In the UK, the way you are taxed on your crypto depends on whether you are classified as a crypto investor or financial trader (business). According to HMRC, most individuals hold cryptoassets as personal investments and therefore are most likely to be subject to capital gains tax and income tax.

Very rarely an individual’s crypto activity may be considered financial trading, in which case they would be required to pay income tax and national insurance on their profits.

It’s important to note that the term ‘trades’ is often used to describe buying and selling crypto assets; however, this use of the term does not mean you are regarded as a financial trader for tax purposes.

HMRC have confirmed in their guidance that "Only in exceptional circumstances would they expect individuals to buy and sell exchange tokens with such frequency, level of organisation and sophistication that the activities amount to a trade in itself.”

For more help determining how your crypto activity would be classed head to our "Investor or trader" article.

Employees or self employed contractors who are paid in crypto are taxable on this employment or self-employment income as usual.

Capital gains tax and income tax are the two main types of taxation that crypto investors need to be aware of. Capital gains tax is levied on the capital gain made from the disposal of crypto assets, whereas income tax is applied to crypto related income such as mining or staking rewards. Understanding the difference between these two types of taxation is crucial for accurately reporting your tax obligations relating to crypto in the UK. Let’s dive in…

Crypto capital gains tax

Every time you dispose of a crypto asset, you’ll incur a capital gain or loss and when your total capital gains in the tax year exceed the annual capital gains allowance you will pay capital gains tax.

HMRC guidance confirms that disposals include:

- Selling crypto assets for fiat money (e.g. selling Bitcoin, BTC for pounds sterling, GBP)

- Exchanging one crypto asset for a different crypto asset (e.g. trading Bitcoin for Ethereum)

- Using crypto to pay for goods or services (e.g. fees on crypto trades, buying a coffee or paying for a software subscription)

- Gifting crypto assets to another person (except a spouse/civil partner or qualifying charity)

Find out how to calculate crypto gains for taxes in our guide.

HMRC’s recent DeFi guidance states that some DeFi transactions (even if not via DeFi platforms), might also be subject to capital gains tax. When a change in beneficial ownership takes place upon locking up and unlocking your tokens, the following transactions are subject to capital gains tax at the time of entering and exiting a position (in addition to taxing the rewards receivable from this activity):

- Lending out your crypto assets

- Staking your crypto assets

- Adding/removing your crypto to/from a liquidity pool

- Depositing crypto assets as collateral for a loan you take out.

For more detailed guidance on DeFi taxes take a look at our "DeFi tax guide".

Capital gains tax allowance

In the UK, all taxpayers are entitled to a capital gains tax allowance (aka exemption) each tax year; you are only required to pay tax on net capital gains that exceed this amount. (A UK tax year runs from 6th April to 5th April).

Historically, HMRC has been fairly generous with the CGT exemption, however in the Spring Budget 2023, the government announced cuts to the annual allowance as part of their efforts to reduce the tax gap.

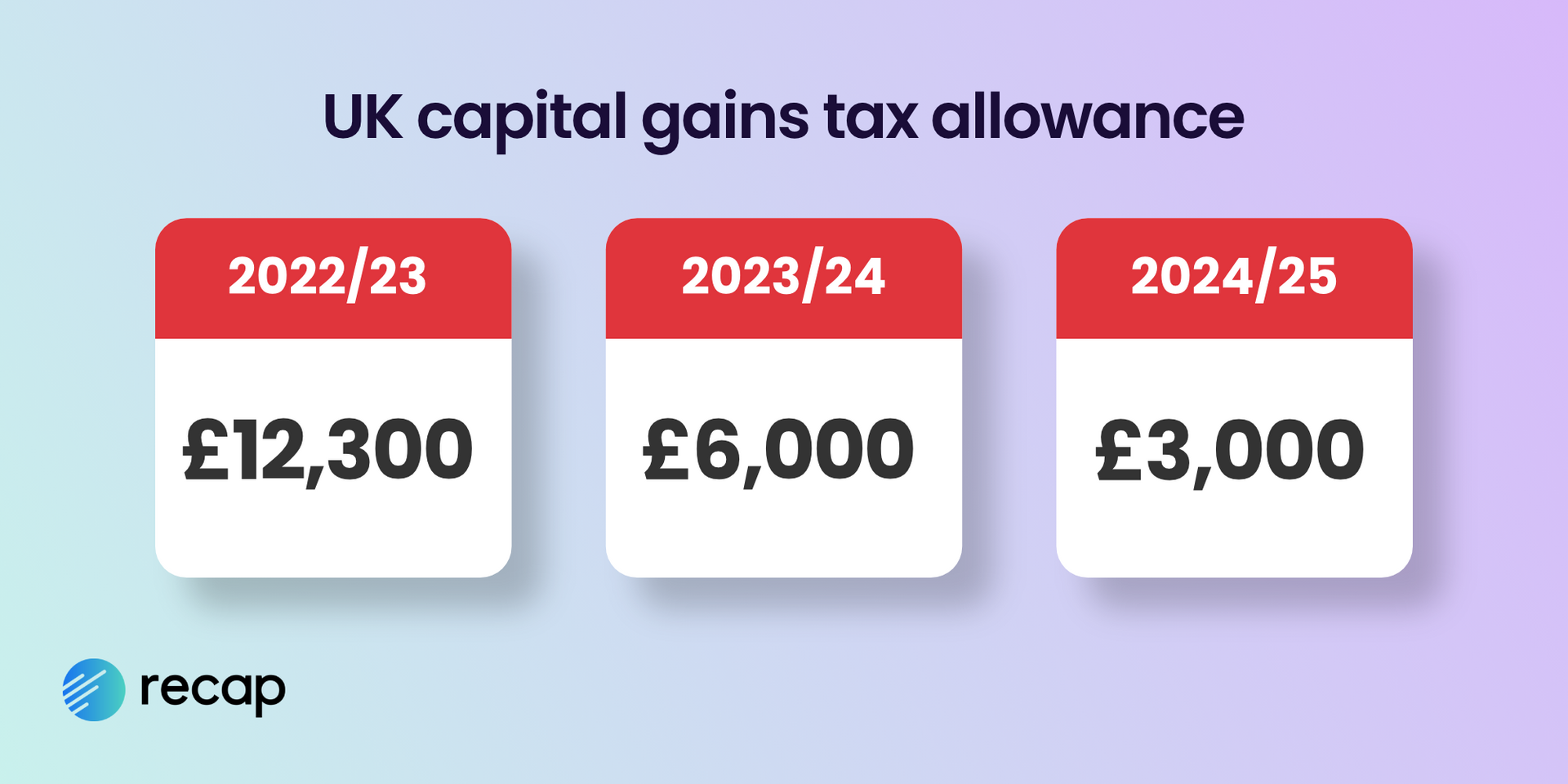

Below, we have clarified the capital gains allowance for the current tax year (2023/24) and the upcoming tax year (2024/25). Make sure to take advantage of the allowances while you still can!

Capital gains tax allowance (exemption)

| 2022/23 Tax Year | 2023/24 Tax Year | 2024/25 Tax Year |

|---|---|---|

| £12,300 | £6,000 | £3,000 |

UK capital gains tax rates

When a UK individual’s net capital gain exceeds the annual capital gains allowance, then capital gains tax is payable.

The tax rate you will pay on your taxable crypto gains is either 10% or 20%, depending on your total income for the tax year (this typically includes your annual salary, self-employment income and investment income).

Capital gains tax rate 2023/24 & 2024/25

| Taxable Income | Tax Bracket | Capital Gains Tax Rate |

|---|---|---|

| £12,570 - £50,270 | Basic Rate | 10% |

| £50,270+ | Higher Rate | 20% |

Where the taxable income is more than £50,270, the CGT rate is 20%. Where the taxable income is less than £50,270, the deficit below £50,270 becomes the amount of capital gains that can be taxed at the lower 10% capital gains tax rate. A maximum of £37,700 capital gains can be taxed at the 10% CGT rate where there is no income in the year.

Example

- Four crypto investors each made a net capital gain of £66,000 in the 2023/24 tax year.

- Less the CGT annual exemption (£6,000), that's a taxable gain of £60,000.

- Each investor has a different total income for the tax year. In the table below we’ve demonstrated how this affects the total capital gains tax:

| Total income in tax year (Taxable capital gain) | Basic rate band that can be used for 10% CGT rate | CGT at 10% (Gain taxed at 10%) | CGT at 20% (Gain taxed at 20%) | Total CGT |

|---|---|---|---|---|

| £30,270 (£60,000) | £20,000 | £2,000 (£20,000) | £8,000 (£40,000) | £10,000 |

| £5,000 (£60,000) | £37,700 | £3,770 (£37,700) | £4,460 (£22,300) | £8,230 |

| £50,270 (£60,000) | £nil | £12,000 (£60,000) | £12,000 | |

| £250,000 (£60,000) | £nil | £12,000 (£60,000) | £12,000 |

Crypto income tax

In the UK, some returns (sometimes called rewards) from crypto asset activity are treated as taxable income and taxed at your regular income tax rate. For some types of income you’ll also be required to make National Insurance contributions too.

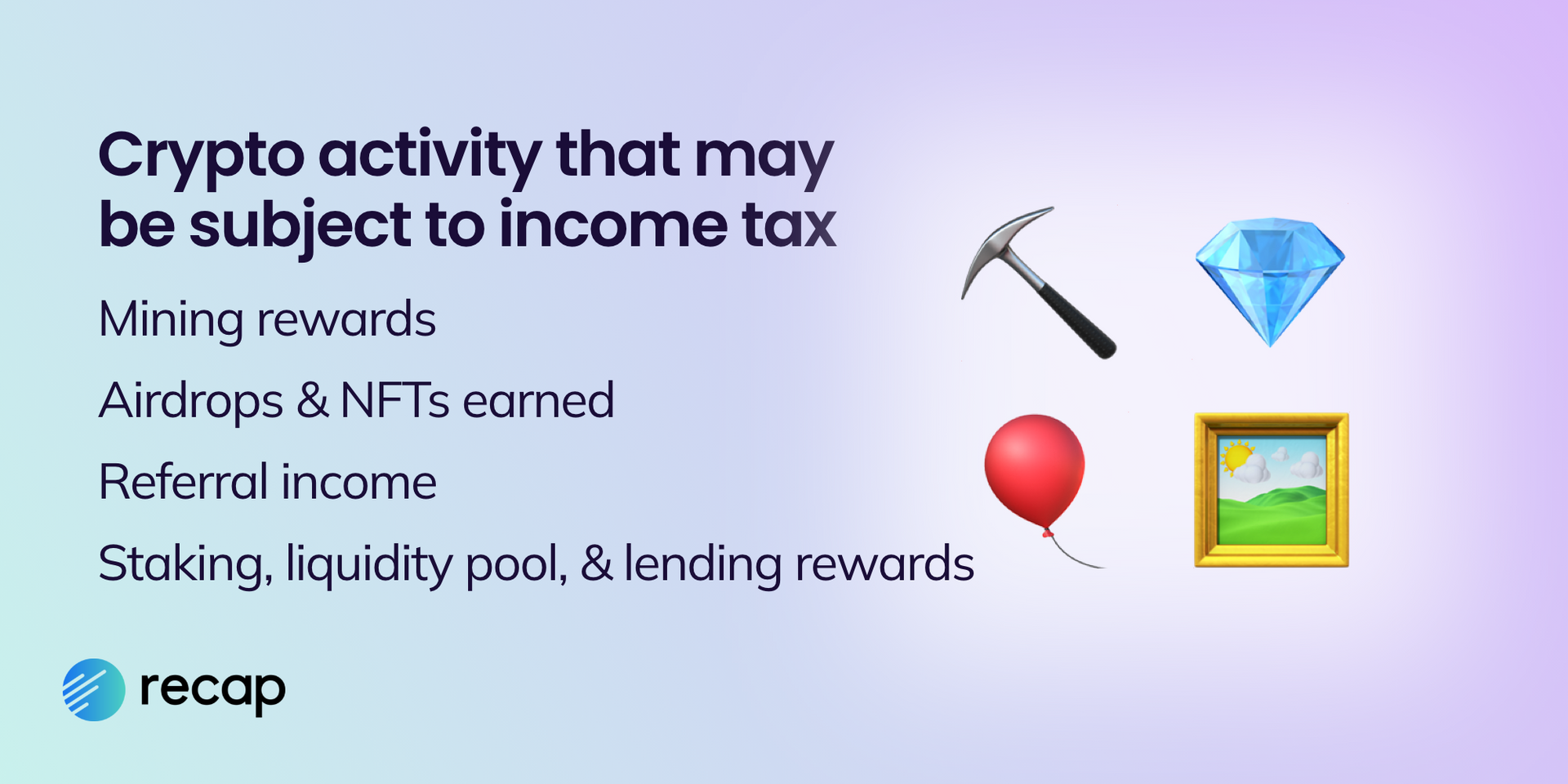

HMRC guidance indicates it is likely that the following crypto activity is taxed as income:

- Mining rewards

- Staking rewards

- Liquidity pool rewards

- Lending rewards

- Taxable airdrops

- Referral income

- NFTs earned

Crypto income is taxed in different ways, depending on the type of income, the individual's status (investor or trader) and the activity undertaken to generate it. Let’s take a closer look…

Miscellaneous income

In the UK, most individuals investing in crypto will be taxed on their crypto income for the activities listed above as miscellaneous income, subject to income tax, with any allowable expenses or the trading allowance, reducing the amount chargeable.

DeFi staking and lending income

On the basis of HMRC's new guidance on DeFi staking and lending, it is expected that most staking and lending rewards will be treated as income rewards. Factors that determine the nature is income by receipt include:

- Return earned by providing a service to the borrower/DeFi lending platform (ie borrower agreeing to pay 5% pa of the principal to a lender over the period of borrowing)

- Return known at time agreement made

- Return is paid by the borrower/DeFi lending platform to the lender/liquidity provider

- Return is paid periodically throughout the period of the lending/staking

- The period of the lending is fixed or short-term

Losses on miscellaneous income

A loss under the miscellaneous income provisions can be carried forwards to reduce future miscellaneous income from the same source.

Subsequent disposals of crypto income

When crypto assets received as income are later disposed of, the capital gain (or capital loss depending on the change in value since acquisition) needs to be included in the individual’s net capital gain.

Financial trading

In exceptional circumstances, individuals may be classed as “financial traders” for some or all of their crypto asset activity. This could be buying and selling crypto, staking, mining or trading in crypto asset derivatives. Where this is the case, their profits are self-employed business profits, subject to income tax and national insurance, rather than capital gains tax on their capital gains and income tax on their miscellaneous income. Being classed as a trader rather than investor usually results in a higher tax bill.

How to file your crypto tax return if you are classified as a financial trader

Individuals classed as financial traders will need to be registered as a sole trader business with HMRC in order to file their for Self Assessment tax returns. You can register online but we recommend seeking the advice of a qualified tax professional first to confirm your status as a financial trader.

Trading allowance and expenses

The allowable trading expenses (under the normal income tax rules for businesses) are deducted from the receipts to calculate a trading profit or loss. The HMRC Business Income Manual provides lots of guidance about the kind of expenses that can be deducted.

Can crypto mining electricity and equipment be claimed as an expense by financial traders?

Under normal business expense principles, the cost of additional electricity used in order to mine and capital allowances on the mining equipment used should be allowable expenses, however HMRC have not explicitly stated this in their crypto tax guidance.

Losses from financial trading in crypto assets

A trading loss can be claimed and used against other income or carried forwards to set against future profits from the same trade, making them more useful than losses under miscellaneous income provisions. HMRC have been known to challenge trading losses to deny loss relief by making a case that the taxpayer is not a trader; or arguing that although they are a trader, they are not trading on a commercial basis with a view to making a profit. The consequence of a successful HMRC challenge is that the trading loss cannot be offset against other income (i.e. employment); it can only be carried forwards against profits of the same trade.

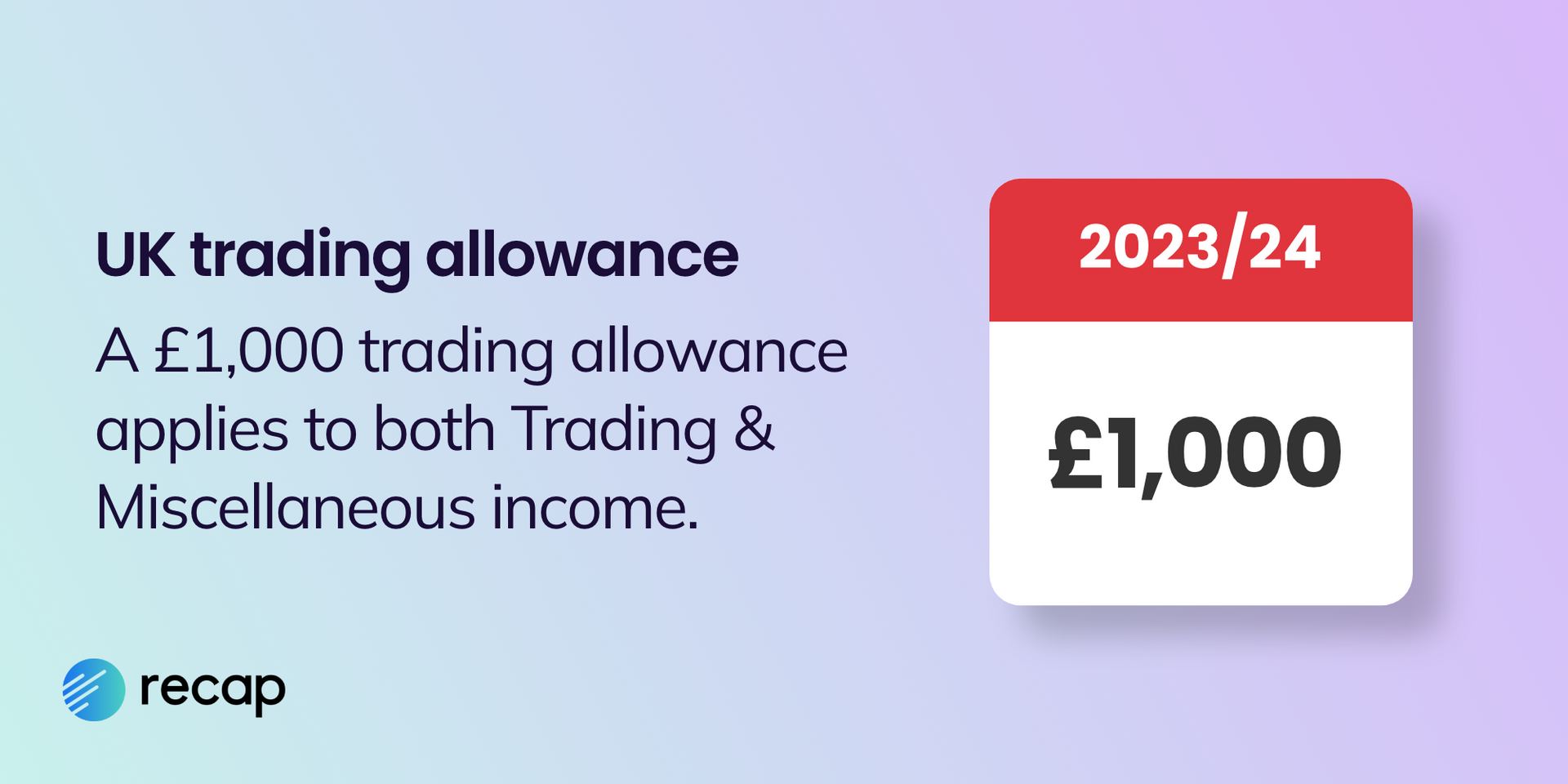

Trading allowance for crypto income

From tax year 2017/2018 there has been a trading allowance of £1,000 that applies to both Trading and Miscellaneous income. If the total trading and miscellaneous income for a tax year is less than £1,000 and the individual has no other self-employment, there is no tax to pay on this income and nothing to declare to HMRC. (Although this is recommended if you already file a tax return).

If the trading and miscellaneous income is more than the £1,000 Trading Allowance, the individual can choose to simply deduct £1,000 from their total income, without needing to justify the costs incurred. The trading allowance cannot create a loss (i.e. if income is £600, the remaining £400 of the allowance cannot be claimed as a loss).

Alternatively, if the actual expenses incurred on the activity of generating the income is more than £1,000 you can choose to deduct the actual expenses instead of the £1,000 allowance. You may need to justify these expenses to HMRC at a later date if investigated. Capital costs such as purchase of hardware cannot be deducted.

The trading allowance cannot be claimed against the crypto asset trading or miscellaneous income where any self employed expenses or the trading allowance are being deducted from self employed income.

Employment income

Some individuals receive their employment income/ salary as crypto income. Employment income received in crypto assets is subject to income tax and national insurance contributions at the sterling equivalent at the date of receipt.

The way the tax and NI is collected depends on whether or not the crypto asset tokens are readily convertible assets (RCAs) and whether the employer is based in the UK or overseas.

If your employer has no UK presence, you are required to operate your own PAYE scheme and make tax and NI payments to HMRC every time you are paid in crypto.

In the UK, can your salary be paid in crypto?

As HMRC are clear that crypto assets are not money and that employees need to receive an actual sterling payment for National Minimum Wage purposes, employers should consider paying part of the salary in fiat sterling.

Self-employment income

Some individuals receive payment for their self employment work in crypto. Self-employment income received in crypto assets is subject to income tax and national insurance contributions at the sterling equivalent at the date of receipt.

UK income tax rates

The rate of income tax depends on the overall income level and other types of income in the tax year. As a rough guide, the current income tax rates for miscellaneous income, employment income and self-employment are:

| Taxable Income | Tax Bracket | 2022/23 Tax Rate | 2023/24 Tax Rate |

|---|---|---|---|

| Up to £12,570 | Personal Allowance* | 0% | 0% |

| £12,571 - £50,270 | Basic Rate | 20% | 20% |

| £50,271 - £125,140 | Higher Rate | 40% | 40% |

| £125,141 - £150,000 | Higher Rate | 40% | 45% |

| £150,001+ | Additional Rate | 45% | 45% |

The UK uses a progressive tax system meaning that the more income you make, the higher tax you pay. You do not pay a flat rate on all income based on your tax bracket, as you climb up the tax brackets your tax rate increases; for the 2022/23 tax year income up to £12,750 is tax free, income between £12,571-£50,270 is taxed at 20%, income between £50,271-£150,000 is taxed at 40% then 45% for income over £150,000. As you can see, more of your income is taxed at 45% from 2023/24, with income in excess of £125,140 being taxed at this top rate.

* The Personal Allowance goes down by £1 for every £2 that your adjusted net income is above £100,000.

What is cost basis in crypto?

Before you can calculate your capital gain from crypto you need to understand the original cost of acquisition or ‘cost basis’ of your crypto asset. Because most crypto investors have thousands of transactions and own multiple kinds of the same asset, establishing the cost basis can be difficult.

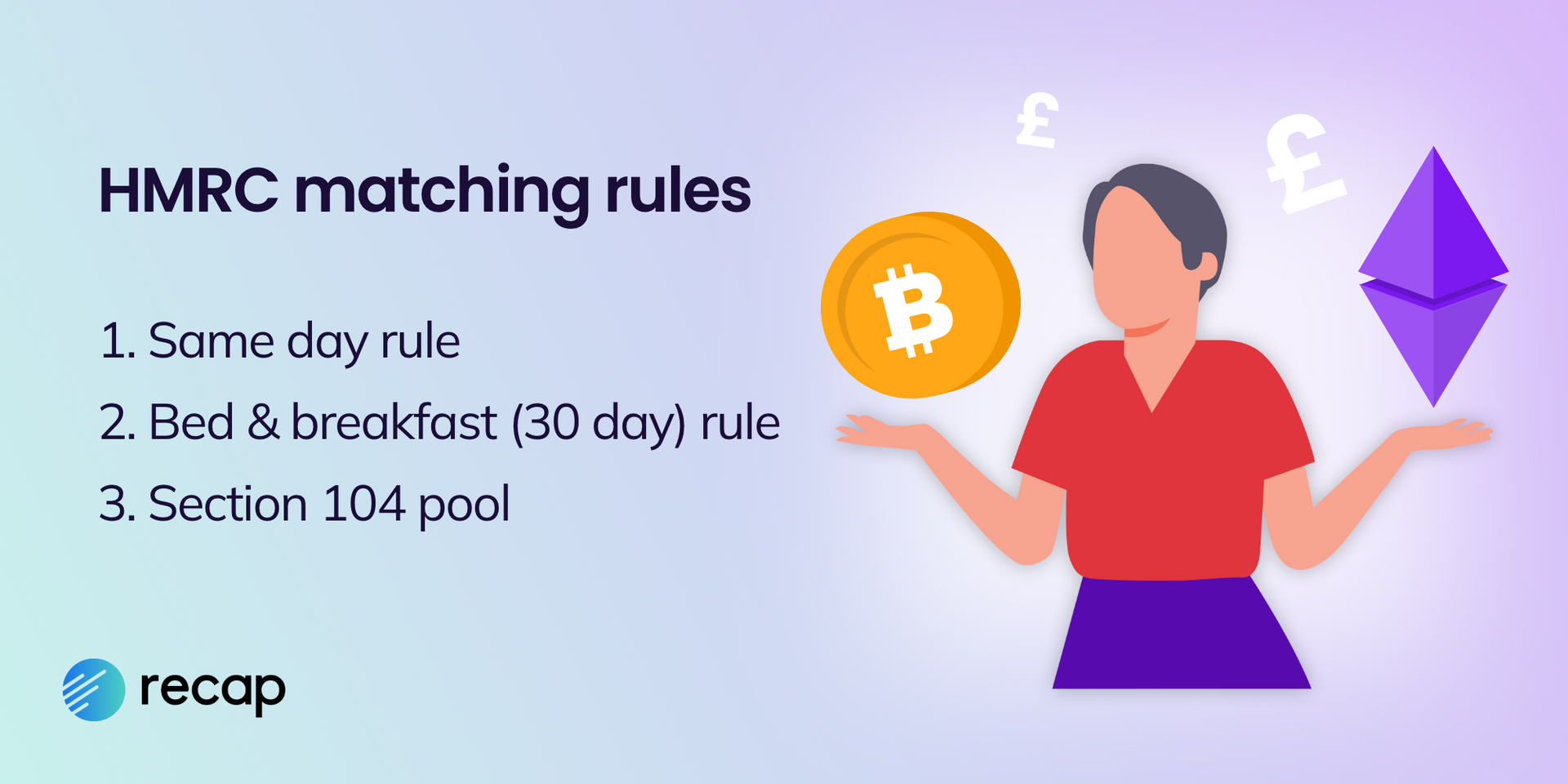

In the UK, the cost basis for your crypto is determined by HMRC’s Section 104 (S104) pooling method, combined with the matching rules. Pooling is also the concept used to calculate the CGT on disposal of traditional shares and the matching rules prevent individuals purchasing and selling assets in a short period of time to manipulate capital gains and losses.

HMRC describes the concept of pooling as: Instead of tracking the gain or loss for each transaction individually, each type of cryptoasset is kept in a ‘pool’. The consideration (in pounds sterling) originally paid for the tokens goes into the pool to create the ‘pooled allowable cost.

The matching rules

To find the cost basis, also known as the allowable cost, the first step is to identify which crypto assets have been sold by following the ‘matching rules’ as set out in the order below.

1. Same day rule

When you dispose of a crypto asset they are first matched with acquisitions made on the same day. So if you buy and sell an asset on the same day, then you need to use the cost basis from this day to calculate the gain or loss.

2. Bed and breakfast rule (30-day rule)

If the same day rule does not apply, then the crypto asset disposed of is matched with acquisitions made in the 30 days after the disposal, on a first-in first-out basis.

3. Section 104 pool

When the same day rule and bed and breakfast rule do not apply, the disposal is matched against the relevant number of tokens and their pro-rata cost in the S104 pool. Each crypto asset held has its own S104 pool, which is an aggregate of all the acquisitions (which are not matched under the same day/30 day rules). The S104 pool provides an average cost basis for the crypto assets.

Find out more in our article "Crypto cost basis".

Do you pay tax when buying crypto in the UK?

When buying crypto in the UK, whether or not you pay tax depends on the method and currency you use to purchase the asset. Here’s a breakdown of the tax implications for different scenarios:

Buying crypto with GBP

If you purchase cryptocurrency with fiat currency like GBP, you won’t be taxed at the time of purchase. However it is crucial to maintain a record of these transactions so you can calculate your capital gain/loss when eventually disposing of the asset.

Buying and HODLing crypto

When you buy cryptocurrency and hold on to it - known as HODLing, this action is not taxable as you continue to retain the crypto. Nevertheless, you should keep a record of your acquisition cost for calculating the gains or losses for future taxable disposals.

Buying crypto with crypto

Trading or swapping one crypto asset for another is subject to capital gains tax. Many crypto investors overlook this when filing their taxes because they are not “cashing out”. However, HMRC recognises buying crypto with crypto as two transactions: the disposal of one crypto asset and the acquisition of another. The disposal realises a capital gain or loss and therefore is potentially subject to capital gains tax, depending on the availability of your capital gain tax exemption and any capital losses brought forwards. The sterling market value of the crypto asset disposed of is used as the disposal proceeds in the calculation of the capital gain or loss and is also recognised as the acquisition cost of the crypto asset acquired in the exchange.

Buying crypto with stablecoins

Buying crypto with stablecoins is treated similarly to buying crypto with crypto and is subject to capital gains tax. Stablecoins are designed to maintain a relatively stable value, because they are typically pegged to a currency or commodity. While it’s unlikely you will recognise a gain or loss substantial enough to impact the tax payable, it is still essential to record these transactions for tax purposes. Investors are often surprised that they realise gains or losses on trading in and out of stablecoins; but this is inevitable due to fluctuation of the price of the pegged currency to sterling between acquisition and disposal of the stablecoin.

Do you pay tax when selling crypto in the UK?

Yes, you have to pay tax when selling crypto in the UK, any capital gains over the capital gains allowance will be taxed at 10% or 20% depending on your income in the same tax year.

Selling crypto for fiat currency

Crypto sold for fiat money is treated as a taxable disposal, subject to capital gains tax. To calculate the capital gain or loss, subtract the cost basis of the asset from the fair market value of the asset on the day you disposed of it.

Selling crypto for another crypto

Selling one crypto asset for another is subject to capital gains tax. HMRC recognises this transaction as two transactions: the disposal of one crypto asset and the acquisition of another. The disposal realises a gain or loss and therefore must be subjected to capital gains tax. The sterling market value of the crypto asset disposed of is used as the disposal proceeds in the calculation of the capital gain or loss and is also recognised as the acquisition cost of the crypto asset acquired in the exchange.

Do you pay tax when spending crypto in the UK?

Spending crypto assets to purchase goods or services is a taxable disposal in the UK, subject to capital gains tax. HMRC views spending crypto as a barter transaction and it is treated as though you had sold the crypto assets to the person providing the goods or services and then used the fiat money they gave you to purchase their goods or services.

- If you paid full market value - the disposal proceeds are the sterling market value of the crypto assets disposed of (or more simply valued as the cost of the goods or services purchased).

- If you paid below market value - the disposal proceeds are the sterling market value of the crypto assets disposed of, rather than the cost of the goods or services purchased.

There are special rules where you are buying goods/services from a connected person, your spouse/civil partner or a charity/CASC/National Purpose.

Keep reading to find out more taxes on crypto gifts and donations.

Do you pay tax when transferring crypto in the UK?

No, in the UK, transferring crypto between your own accounts and wallets is not subject to tax. Such transfers are considered tax-free as they are not classified as taxable disposals. That being said, it is important to keep records of all your transfers for HMRC in case they are incorrectly assumed to be disposals.

Are transfer fees taxable?

When transferring crypto between accounts, it’s possible to incur transfer fees from your exchange or wallet. This transfer fee is only tax free when paid in fiat currency. When the transfer fee is paid in crypto, HMRC considers it as spending crypto, which is regarded as a disposal subject to capital gains tax.

Read more in our article “Do you pay tax when transferring crypto?”

Taxes on crypto gifts and donations

When it comes to gifting and donating cryptocurrency in the UK, it’s important to understand the tax implications. In most cases, gifting cryptocurrency is considered a taxable disposal subject to capital gains tax, however there are some exceptions and specific rules that determine where gifting can be tax free. Let’s explore in more detail below.

Gifting crypto to a friend

When you gift cryptocurrency to anyone other than your spouse or civil partner, it is treated as a taxable disposal. This means that you will be liable for capital gains tax based on the full market value of the crypto asset, regardless of whether you receive anything in return for the gift.

Receiving crypto assets as a gift is not taxable. However, when the recipient later disposes of the gifted crypto, they will be subject to capital gains tax. The acquisition cost of the crypto asset will be considered as the market value on the date of receipt.

For more detailed information on how crypto gifts are taxed, please read our comprehensive article on "How are crypto gifts taxed?"

Gifting crypto to your spouse or civil partner

In the UK, gifting cryptocurrency to your spouse or civil partner is considered tax-free and there are no limits on the amount you can transfer. Spousal gifting can be a great tax optimisation strategy allowing both individuals to utilise their full capital gains allowance.

When you gift a crypto asset to your spouse or civil partner it is viewed as a disposal for the giver and acquisition for the receiver, however the disposal is deemed to take place at “no-gain” and “no loss” making it tax free. To qualify, the couple must be:

- Married or in a civil partnership, and

- Living together during the tax year.

When the recipient later disposes of the gifted crypto, they inherit the acquisition cost from their spouse or civil partner for capital gains tax calculations.

For more detailed information on spouse gifts, including exceptions, separation and divorce implications, and how to report them to HMRC, please refer to our article on spouse gifts.

Donating crypto to charity

In the UK, if an individual donates crypto to one of the below bodies they would be eligible for relief from capital gains tax:

- a UK, EU or EEA charity (subject to strict definitions and conditions)

- a community amateur sports club (CASC), or

- a body for a National Purpose (ie British Museum)

The disposal is treated as being made for no-gain and no-loss. Because of this, the recipient of the donation can pay up to the acquisition cost of the crypto asset and the donor will not realise a capital gain on the disposal. Therefore it does not need to be an outright gift to the charity. However, if the recipient pays greater than the acquisition cost, the donor will be liable for capital gains tax on the disposal, based on the amount received. Capital gains relief is also not available when someone makes a tainted donation.

Donations of crypto assets do not qualify for gift aid income tax relief or any income tax relief. These are only applicable to donations of fiat currency or certain assets like shares, listed securities and property.

For a comprehensive understanding of crypto donations, including the definition of a charity, conditions of a tainted donation, and more, please read our detailed article "Are crypto donations tax deductible?".

Crypto mining taxes

In the UK, cryptocurrency received from mining is generally considered income, however the classification of mining income varies depending on whether it is considered a hobby or business activity.

HMRC’s broad expectation is that most individuals generating an income from mining will be classed as hobbyists, who need to report it as miscellaneous income. Only in exceptional circumstances will mining income amount to a financial trading activity which is subject to income tax and national insurance contributions. Let's explore in more detail below.

Mining cryptocurrency as a hobby

For most individuals in the UK, cryptocurrency mining is considered a hobby. In this case, the income generated from mining should be reported as miscellaneous income on the self-assessment tax return. The income is the sterling value of the tokens received from mining, at the time of receipt, with any allowable expenses deducted. Capital expenses such as hardware cannot be deducted. As a hobbyist, when you dispose of your mining rewards, they become subject to capital gains tax, based on the change in value between receipt and disposal.

Mining cryptocurrency as a business

In exceptional circumstances, cryptocurrency mining can be classed as a business activity. In this instance, mining income is added to your trading activity, with allowable expenses, such as hardware, deducted and is subject to income tax. As a financial trader you will also need to pay national insurance contributions. These crypto assets received as income from mining, will be subject to the capital gains tax regime when they are later disposed of. There will be a capital gain if the tokens have increased in value between receipt and disposal, or there will be a loss if their value has decreased.

By classifying your mining activity correctly and understanding the tax obligations you can ensure compliance with HMRC regulations.

For more detail head to "Do you pay tax on crypto mining?"

Crypto staking taxes

In the UK staking rewards can be subjected to either income tax or capital gains tax, depending on the specific mechanisms of the DeFi protocols you are participating in. To determine how your staking activity should be treated it is necessary to consider if the nature of the rewards is capital or income. Below we explore the different tax treatments applicable to staking rewards.

Staking reward: income tax treatment

If staking rewards are deemed as income in nature, they will be taxable as miscellaneous income, subject to income tax at the date they are deemed to be ‘receivable’. They could therefore be taxable at a point before they are actually received into your wallet. This applies where the rewards have been credited to your account and it is within your power to claim them, but you are choosing not to. This can be a common scenario where you periodically claim accrued rewards or where they are auto-compounding. The value of the reward tokens in GBP on the date they are ‘receivable’ is considered the taxable miscellaneous income. It is worth noting that allowable expenses or the trading allowance (if applicable) can be deducted, reducing the amount of income chargeable to income tax.

If the taxpayer is classified a ‘financial trader’ in cryptoassets, these rewards may be treated as trading income rather than miscellaneous income.

Staking rewards: capital gains tax treatment

Alternatively, if the staking reward is determined capital in nature, it will be subject to capital gains tax. A capital gain is realised on this reward at the time of entering the staking position. The amount of capital gain is the estimated present value of the future capital reward. Determining this is complex and you may need to pay the capital gains tax on it before you even receive the reward. Upon receipt of the capital reward (usually upon exit), the gain is reassessed based on the value of the reward at that time.

Discover whether your staking rewards are classified as income or capital in nature and read our detailed guidance in our comprehensive article How is crypto staking taxed in the UK?

Crypto tax on margin trading, futures and CFD’s

The tax position for individuals trading and investing in derivatives over crypto assets (ie CFD’s, Futures and Margin trading) is different to the tax position of an investor buying and selling crypto assets.

In the United Kingdom, the tax position regarding margin and futures trading of crypto assets currently lacks clear guidance, however, HMRC directs individuals to their guidance for non-crypto specific derivatives.

Depending on the level of activity some individuals may be treated as a financial trader and taxed as trading profits, where this is not the case, profits from trading derivatives may constitute either miscellaneous income or capital gains.

Discover what you need to consider when deciding whether or not your activity is to be treated as miscellaneous income or capital gains by reading our comprehensive article "How are derivatives taxed in the UK?" Below we’ll explore the different types of derivative trading in more detail.

Spot margin trading

Using borrowed funds, traders buy cryptocurrencies to potentially amplify gains or losses through leverage. When participating in spot margin trading, on exchanges like Kraken and Binance, crypto investors will realise a profit or loss upon closing their position. This will either be taxed as miscellaneous income/loss or a capital gain/loss.

Contracts for difference (CFD’s)

Contracts For Difference (CFD’s) are commonly found on platforms like Plus500 and eToro; traders essentially speculate on the price movements of a crypto asset without owning it. Profits or losses realised from this activity will either be taxed as miscellaneous income/loss or a capital gain/loss.

Futures trading

Futures contracts are agreements to buy or sell a crypto asset, at a predetermined price on a specific future date. Traders can use futures contracts to hedge against price volatility or to speculate on price movements. There is potential for both substantial gains and losses. Profits or losses realised from futures trading will either be taxed as miscellaneous income/loss or a capital gain/loss and traders will pay capital gains tax on their profits as noted above.

Options trading

Options trading involves the buying or selling of contracts that grant the right, but not obligation, to buy or sell a cryptocurrency at a predetermined price within a specified timeframe. Traders use options to hedge risk, speculate on price movements, or generate income, while the potential loss is limited to the initial premium paid for the option. Profits or losses realised from this activity will either be taxed as miscellaneous income/loss or a capital gain/loss.

Spread betting

Spread betting involves predicting whether the price of a cryptocurrency will rise or fall, traders speculate on the price movement by betting a certain amount per point change in the asset's price. The profit or loss is determined by the accuracy of the prediction and the extent of the price movement. In the UK, spread betting is generally regarded as a speculative activity resulting in no tax obligations. As always there are detailed conditions to navigate and you need to seek professional advice to confirm the tax position.

Taxes on airdrops and forks

HMRC have released clear guidance on how crypto airdrops and hard forks should be treated for tax.

Tax on airdrops

Crypto assets received as airdrops are sometimes taxable as income when received and subject to capital gains tax when later disposed of.

Taxable airdrops: miscellaneous income

Airdrops are taxable income if they are received in return for, or in expectation of, the individual performing a service or doing something in return in order to qualify. Although not in HMRC guidance, it seems to be generally accepted that if the recipient of the airdrop provides a service to the issuer, for example providing some coding work, or an influencer shilling the crypto; that would make it taxable as income.

In such cases, you should record the sterling market value of the received crypto assets as either self-employment business income if appropriate, subject to income tax and national insurance, or as miscellaneous income on your Tax Return, subject to income tax.

Trading income from airdrops

If airdrops are received as part of a trade or business involving crypto assets or mining; you should record the sterling market value of the received crypto assets as self-employment business income on your Tax Return, subject to income tax and national insurance.

Non-taxable airdrops

HMRC have confirmed that if the airdropped tokens are received without an expectation of, or performing an action in return, and are not received as part of a trade or business involving crypto assets or mining; there is no income to declare and no income tax to pay.

Capital gains tax on airdrops

Regardless of whether the airdrop was treated as taxable or non-taxable upon receipt, the crypto asset will be subject to capital gains tax when disposed of. For income taxable airdrops, the acquisition cost for capital gains tax purposes is the sterling market value at the date of receipt. There is no guidance from HMRC for non-income taxable airdrops, however it is likely the acquisition cost is Nil, although it could be argued that it is the market value of the token at the date of receipt, depending on the circumstances.

To learn more about crypto airdrops and their tax implications, read our comprehensive article ‘A guide to crypto airdrops’.

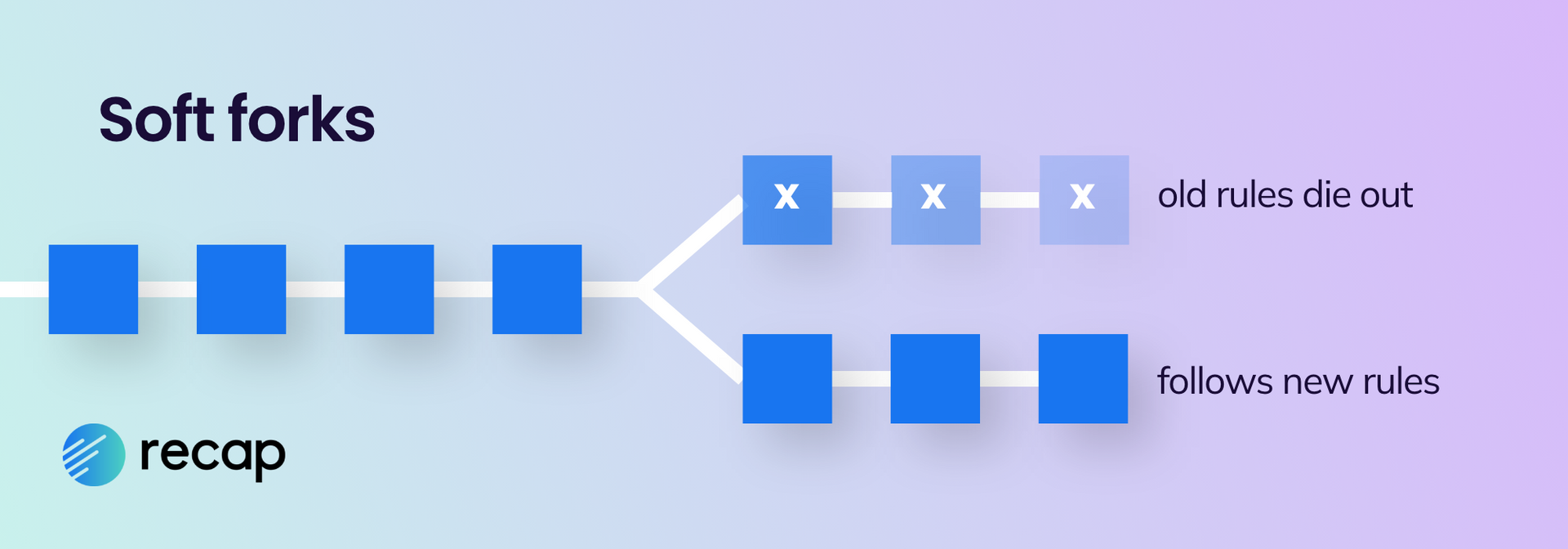

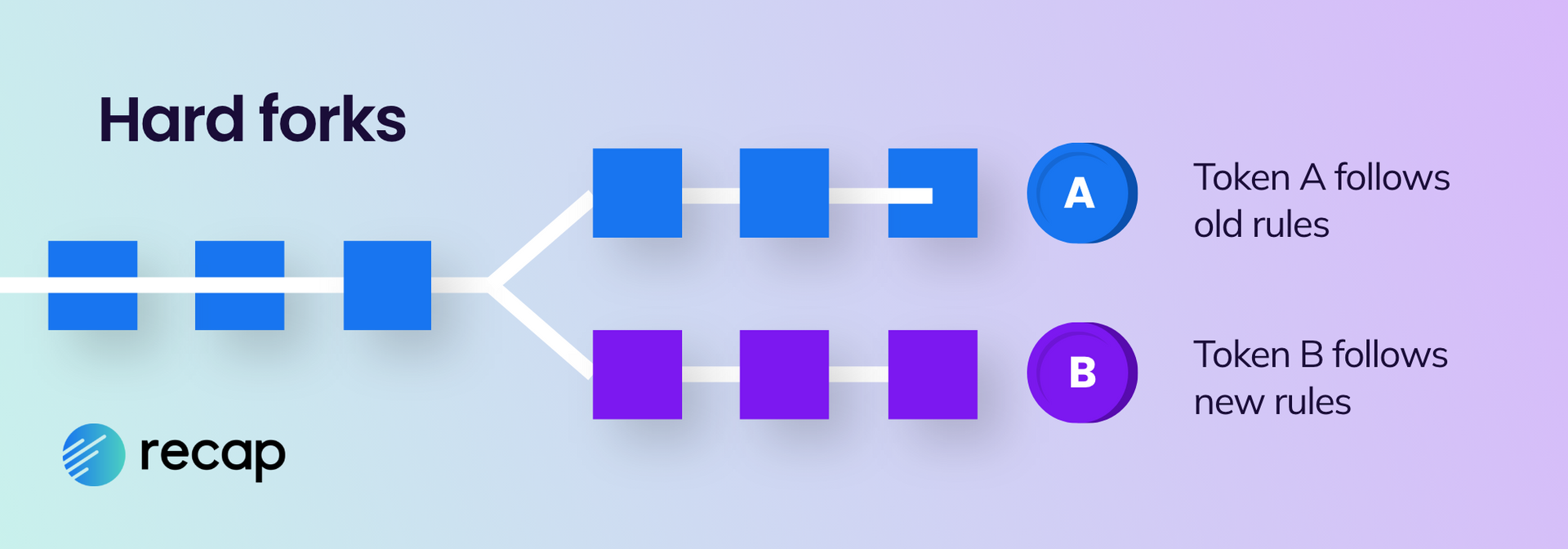

Tax on forks

Some crypto assets operate by consensus amongst their community; when a significant part of the community want to do something different they may create a ‘fork’ in the blockchain. There are two types of forks, a soft fork and a hard fork with different tax treatments.

Soft forks

A Soft Fork updates the protocol and is intended to be adopted by all. As no new tokens or distributed ledger are expected to be created there is no impact on the tax position.

Hard forks

In a hard fork, individuals typically receive new tokens, which is not a taxable event. However, it is crucial to determine the value of these tokens at the time of receipt, for calculating capital gains when you eventually sell or dispose of the assets. The value is derived from the original tokens already held. After the fork, an individual will usually hold an equal number of tokens on both distributed ledgers; with the new tokens being added into their own S104 pool. Part of the acquisition costs of the pre-fork tokens is reallocated to the S104 pool of the new tokens.

For detailed insight, refer to our article "Crypto forks: what are the tax implications?"

UK, DeFi crypto taxes

In February 2022, HMRC released new guidance in their Cryptoasset Manual, specifically addressing the taxation of decentralised finance (DeFi) type activities such as lending and staking. This guidance applies to both decentralised and centralised platforms and aims to provide clarity on the tax treatment of various DeFi scenarios.

Taxation of DeFi in the UK is complex and varies depending on the mechanics and the terms and conditions of the specific DeFi protocol and activity involved.

In addition to calculating the tax position on the rewards received and the eventual disposal of those rewarded tokens, HMRC's guidance highlights the importance of considering the tax position of the principal tokens locked away when entering and exiting various DeFi activities, including lending, staking, adding to liquidity pools, and using crypto assets as collateral for loans.

The tax treatment of the principal tokens locked away in these activities depends on whether beneficial ownership of the locked tokens has been transferred to another party. To determine the correct tax treatment for your lending and staking activities, the following factors should be considered:

1. Tax treatment of the generated rewards:

- Are the rewards considered income or capital gains?

- Are they taxed at the time of entering the activity, upon receipt of the rewards, or both?

- When are the rewards treated as received? This can be earlier than they are received into your wallet. They are taxed as though received at the date they were credited to your account, if you were able to claim them, but chose not to.

2. Tax treatment of the principal tokens locked away during staking/loaning/liquidity providing/collateralisation:

- Is there a capital gains tax disposal upon entering the DeFi position?

- Is there a capital gains tax disposal upon exiting the DeFi position?

We recommend following a three step approach…

- Determine if the rewards are capital or income in nature.

- Examine the terms and conditions of the specific lending/staking activity to determine if beneficial ownership of the tokens locked up has been transferred.

- Consider the tax treatment of the principal tokens locked away upon entering and exiting the DeFi position, as well as the tax treatment of the reward tokens receivable.

For more detailed information and guidance on DeFi taxation, you can refer to our comprehensive DeFi Tax Guide.

HMRC launched a consultation seeking input and suggestions from industry leaders after their DeFi guidance faced criticism from the crypto community. We do not expect to see the conclusions of this consultation and any potential changes in the tax position until after the 2022/23 tax return deadline has passed.

Lost or stolen crypto

HMRC has clear guidance about lost and stolen crypto. While they do not automatically consider lost and stolen crypto a capital loss, there may be opportunities to make a negligible value capital loss claim where assets are still owned, but have become worthless. Read on to learn more.

Losing private keys

If you lose the private key to a wallet containing your crypto assets, it cannot be treated as a disposal for capital gains tax purposes because the private key still exists as part of the cryptography, and the tokens still exist in the distributed ledger.

However, if you can demonstrate that there is no chance of recovering the crypto assets, you can file a negligible value claim. This claim allows you to report a capital loss for the worthless crypto assets.

Being defrauded

Being the victim of theft resulting in the loss of crypto assets is not considered a disposal for CGT purposes, as you still maintain ownership of the stolen asset and have rights to recover it.

Depending on the specifics, in certain cases it may be possible to file a negligible value claim and subsequently claim a capital loss if you can prove:

- that you held the crypto asset at some point yet the tokens have become worthless or

- that you did not receive the crypto asset that you paid for.

Losing crypto in a rug pull

In the event of a rug pull you still own the crypto asset, so this would not be considered a capital loss. You should be able to make a negligible value capital loss claim where the tokens had value at the time they were acquired; but subsequently became worthless at a later point because of the rug pull. Also, you could realise a capital loss by disposing of the tokens for a lower value than the matched acquisition cost..

How to make a negligible value claim for crypto

Individuals can crystallise capital losses for crypto assets that they still own, if they become worthless or of ‘negligible value’. A negligible value claim treats the tokens as being disposed of and immediately re-acquired. As crypto assets are pooled per token, the negligible value claim needs to be made in respect of the whole section 104 pool, not the individual token.

A negligible value claim must state:

- Which crypto asset is the subject of the claim

- amount to be treated as disposed of (may be £nil)

- date that the token should be treated as being disposed of and immediately re-acquired

You have to demonstrate that the asset had value and has later become of negligible value while you own it. This negligible value claim and the capital loss resulting from the claim is to be reported in a Tax Return. You are deemed to dispose of the crypto asset for its current market value, therefore resulting in a capital loss which can be used to reduce capital gains in the same tax year, or be carried forwards.

How are NFTs taxed in the UK?

In the UK, Non-Fungible Tokens (NFTs) are subject to income tax when earned and capital gains tax when disposed of, like other cryptocurrency transactions, however normal capital gains tax pooling and matching rules do not apply to NFTs.

Capital gains tax on NFTs

While there is no specific guidance about the taxation of NFTs from HMRC, it is widely accepted that unless there is an NFT creation business, the disposal of NFTs by investors is taxable under the capital gains tax regime. HMRC has clarified that NFTs are not pooled because each NFT is unique and separately identifiable. Therefore, the normal matching and pooling rules are not relevant.

When disposing of an NFT (i.e. selling or swapping it), the capital gain or capital loss is calculated by deducting the actual acquisition cost of the NFT being disposed of from the disposal proceeds (i.e. the market value of the NFT at the time of disposal).

If NFTs are acquired in bundles, but disposed of individually, a part disposal calculation is necessary to allocate the acquisition cost of the part of the bundle being sold against the disposal proceeds.

Income tax on NFTs

When NFTs are earned, for example as a taxable airdrop (received in return for doing something), as a staking reward or via play-to-earn games, these earnings are most likely taxable as miscellaneous income. The value of the NFT in GBP sterling at the date of receipt will be considered the value of the taxable miscellaneous income.

How are NFT creators taxed?

NFT creators are most likely to be taxed as a trading business for the activity of the creation and sale of their own NFT collection. The self-employed business profits will be subject to income tax and national insurance. Any crypto assets received as business income will be subject to the capital gains tax regime when they are later disposed of, with a capital gain or loss depending on the change in value between receipt and disposal of the tokens.

Other NFT investment activity (not connected to their own collection) will be subject to the capital gains tax regime, unless the activity of buying and selling others’ NFTs is itself a business activity.

NFTs received as DeFi position redemption mechanism

Sometimes NFTs are received as a placeholder redemption mechanism in order for you to remove your position from a liquidity pool or other DeFi type activity.

The tax treatment of the NFT received is determined by whether or not beneficial ownership is retained upon entering the DeFi type activity.

- Where beneficial ownership is retained, the receipt of and disposal of this placeholder NFT is ignored for tax purposes.

- Where beneficial ownership is lost, the receipt of the NFT is an acquisition for tax purposes, with an acquisition cost equal to the value of the tokens added to the DeFi type position in exchange for the NFT placeholder. The NFT placeholder is disposed of when you exit the DeFi position and there will be a capital gain or capital loss, based on the value of the tokens removed from the DeFi position, less the value of the tokens added to the DeFi position.

For a more comprehensive understanding of NFT Taxes in the UK, please refer to our comprehensive guide NFT taxes UK: a complete guide.

How and when to pay crypto taxes in the UK

In the UK, crypto taxes are reported and paid as part of HMRC’s Self Assessment Tax Return. Crypto miscellaneous income, employment income, self-employment income and capital gains or losses must be declared on the Tax Return (form SA100 and supplementary pages).

Reporting capital gains from crypto to HMRC

Capital gains must be reported to HMRC on the Tax Return if the net capital gains for the tax year exceed the capital gains allowance (before the offset of any capital losses brought forwards).

Capital gains and losses from crypto should be combined with capital gains and losses from other sources, such as property and shares; and be reported on the Tax Return using the Capital Gains Summary SA108 supplementary pages. Starting from the 2024/25 tax year, cryptocurrency will have its own dedicated boxes within the capital gains section of the self assessment tax return.

Where you already need to file a Tax Return for other reasons, and your net capital gains are below the capital gains tax annual exemption but your total disposal proceeds for the tax year exceed four times the annual exempt amount there is an additional filing burden to declare your capital gains to HMRC.

Reporting capital losses from crypto

It is essential to report all capital losses, as it is the only way they can be ‘claimed’ to use against future gains. Capital losses can be reported to HMRC on the tax return (if one is already required) or by letter. For more help reporting and using capital losses from crypto take a look at our article “Claiming capital losses from crypto in the UK”.

Reporting miscellaneous income from crypto to HMRC

Miscellaneous Income from crypto should be reported as ‘Other taxable income’ in Box 17 of the SA100 Tax Return form. Any allowable expenses (including the trading allowance if eligible) can be reported in Box 18.

If the total miscellaneous income is less than the Trading Allowance of £1,000 (and you are eligible to claim it), there is no need to report this income to HMRC. However if you already file a Tax Return, it is recommended to declare the income and the use of the trading allowance in Boxes 17 and 18. We recommend the Recap Income Report for the tax year is attached to your tax return to support the income received in crypto assets.

Reporting employment income from crypto to HMRC

If crypto assets are received as employment income, they may or may not need to be reported on the employment pages of the Tax Return, depending on the circumstances.

If the employment income is taxed via PAYE and you do not meet the criteria for filing a Tax Return, there is no need to include the employment income on a Tax Return.

If you receive employment income in the form of ‘readily convertible assets’, the employment income should have been subjected to income tax and national insurance at the time of receipt via PAYE. If your employer has no presence in the UK, it is your responsibility to operate the PAYE scheme and pay the PAYE/NI to HMRC every time you are paid. You will be issued with a form P60 from your employer, summarising the gross employment income and tax deducted.

Where a Tax Return is required for other reasons (i.e. capital gains, rental income, self-employment), you will need to report the gross employment income received in crypto and tax deducted via PAYE (from your P60) on the employment pages of your Tax Return.

If the crypto assets received as employment income are not ‘readily convertible assets’ then they should be reported on the employment pages of the Tax Return and you will need to register for Self Assessment to declare this, if you are not already filing Tax Returns.

Deadline for reporting and paying crypto taxes in the UK?

The UK tax year runs from the 6th April to the 5th April the following year. The deadline for filing and paying taxes is 31st January following the end of the tax year.

There are penalties when you file your tax return late and interest to pay and late payment surcharges when your tax is paid late.

How to register to file a self assessment tax return in the UK

If you don’t already file a Tax Return, you must notify HMRC that you have income or capital gains to report by 5th October. You can register here.

Financial trading in crypto assets

In rare cases where an individual’s crypto activity is classed as financial trading, it should be reported on the Self Employment pages of the tax return. If you are engaged in financial trading in crypto assets, you can register your crypto assets trading business with HMRC here, but we recommend seeking the advice of a qualified tax professional first.

How to calculate your crypto taxes

Calculating your crypto taxes can be a complex and time consuming task, especially if you have a high volume of transactions and engage in complex crypto activities. Using a crypto tax calculator can automate and simplify the process.

To calculate your crypto taxes manually you would need to:

- Keep a record of all your crypto transactions (even if they are not taxable) and:

- apply a GBP sterling value to every transaction (valued at date of transaction)

- identify the acquisition cost / cost basis, following the pooling and matching rules for each token type, as discussed previously

- decide if they are subject to income tax and/or capital gains tax

- Calculate the total GBP income and the income tax (and possibly national insurance) due on your income from crypto within the tax year

- Calculate the capital gains tax due on your net capital gains from crypto within the tax year.

- Provide HMRC with a capital gains tax calculation for every disposal of crypto assets in the tax year; to include number and type of the crypto asset disposed of, disposal proceeds, matched acquisition costs, incidental costs of disposal and the capital gain or loss.

How to calculate your crypto income

To calculate your crypto income:

- Identify the sterling value of your crypto income at the time of receipt for each transaction. Include income which is not yet received, but has been credited to your account and is available to be claimed.

- Add up the total income from crypto.

- Deduct any allowable expenses or the trading allowance (if eligible and you choose to deduct this instead of actual expenses).

How to calculate your capital gains from crypto

To calculate your net capital gains position, the capital gain or capital loss needs to be calculated for each individual disposal within the tax year (disposals of the same crypto asset on the same day can be aggregated). To work out the capital gain/ capital loss on your disposals, subtract the matched allowable costs from the disposals proceeds.

Total capital losses in the tax year are deducted from total capital gains in the tax year; to arrive at the net capital gains for the tax year. Any capital losses brought forwards from earlier years are deducted, but you don’t have to deduct losses once your gains are below the annual exemption. You will be subject to capital gains tax on the net capital gains after losses (from crypto and other assets, like stocks and shares) that exceed the capital gains allowance.

Take a look at our Crypto tax calculator for a quick overview of the capital gains calculation.

Because of the nature of crypto there are typically thousands of transactions to account for and calculating your crypto taxes manually can become extremely tedious. This is the reason why many crypto investors and their accountants consider crypto tax software to be an essential tool.

Calculate your crypto taxes instantly using crypto tax software

You can use Recap to calculate your UK crypto tax income and capital gains tax reports by following these steps:

- Sign up for free

Head to recap.io and sign up using your email address or google account. Make sure to backup your recovery key and select your country and tax jurisdiction settings. - Connect to your exchanges and wallets

Automatically sync your transaction data by connecting your exchanges via API or entering your public wallet addresses. Upload additional data via CSV (for example extinct exchanges, old accounts). - Check your data is correct

Ensure all of your historical data is uploaded (our calculator needs your acquisition costs for capital gains calculations). Verify that all transactions are accurately accounted for. - Recap automatically calculates your crypto capital gains, capital losses and income

Our calculator calculates your gain and loss for each disposal made and your income for every receipt. - Generate and download your crypto tax reports

Subscribe to Recap and head to the tax page to download your crypto tax reports to attach to your Tax Return and/or to provide to your Accountant.

By using crypto tax software like Recap, you can streamline the process and accurately calculate your crypto taxes while saving time and effort. To find out more visit recap.io.